- Quick take

- 8 May 2024

- FX Sweden

Sweden’s Riksbank cuts rates amid mounting economic woes

The Riksbank has cut rates for the first time but is treading carefully amid ongoing concerns about the risk of a weaker currency. However, with Sweden’s interest rate-sensitive economy coming under greater pressure, further rate cuts look inevitable later this year

Domestic economic issues beginning to outweigh currency concerns

Sweden’s Riksbank has cut rates for the first time, taking the main policy rate to 3.75%, a decision that may contain some read-across for what other central banks do over coming months. It’s worth saying that the Riksbank has been telling us for several months now that it intended to start cutting rates in the first half of this year – and economists were divided on whether this meant May or June.

The fact that the Riksbank has chosen to move today – and crucially ahead of the ECB – is telling. The Riksbank has been very sensitive to the value of the currency and this was one of the principal reasons for hiking aggressively over the past couple of years. Policymakers went as far as saying that they needed to stay out in front of the ECB during the hiking cycle.

These fears about the krona have clearly not evaporated entirely. Governor Thedeen has repeatedly signalled that a weaker currency is the major risk to inflation, a line repeated in the latest policy statement. Presumably for this reason, the committee is pushing back on the idea that it could cut rates at back-to-back meetings, continuing to signal its intention to cut rates just twice more this year.

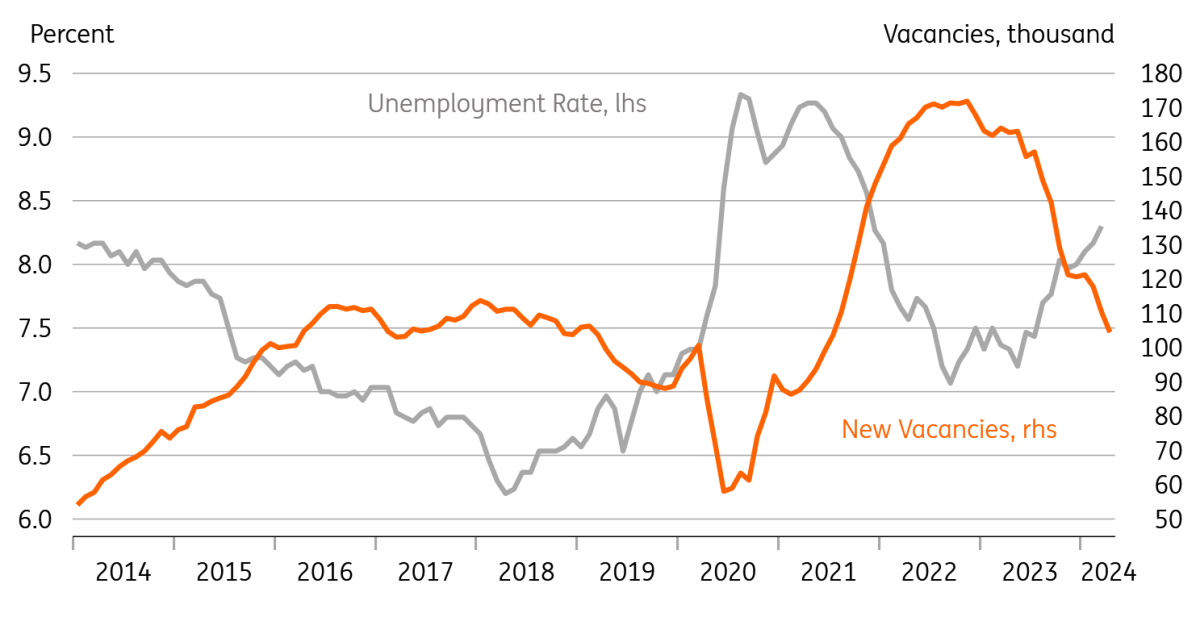

Yet to some extent we think actions speak louder than words, and the fact the Riksbank has cut rates today tells us that domestic economic concerns are starting to dominate the debate within the policy committee. Sweden’s economy has contracted for four quarters in a row now, while the jobs market is cooling more appreciably than elsewhere. By one measure, corporate bankruptcies are the highest since 1996. Core inflation, while still high in some domestically-focused areas, is now much closer to target.

Sweden's jobs market is visibly deteriorating

For markets more widely, the question is whether this decision tells us anything about what other central banks are likely to do over the coming months. We should naturally be cautious in making such comparisons. But having chased the Federal Reserve in taking interest rates higher, Sweden’s considerably more rate-sensitive economy is coming under a strain where the US so far has not. The Riksbank’s dilemma may currently be more acute than elsewhere, but it’s unlikely to be the only central bank to find itself with this trade-off over coming months.

For now, we agree with the Riksbank’s guidance that it will cut twice more this year. That’s in line with our ECB call for three rate cuts in total this year.

SEK woes aren’t over

At the time of writing, EUR/SEK is approaching the 30 April 11.77 highs, trading around 0.5% higher since the Riksbank announcement. If the pair does not trade materially higher by the end of today, we think the central bank will be happy with the market outcome of their rate decision. Still, downside risks for the krona remain quite tangible.

The relatively hawkish guidance by the Riksbank today may well be put in doubt if inflation continues to fall in Sweden. As mentioned above, the Riksbank has shown that it can cut rates despite a weaker SEK, and with two more cuts now highly likely as per forward guidance, the bias will likely be to the dovish side in the SEK curve.

Indeed, a sustainable re-appreciation of the krona depends more on external developments (US data above all) than Riksbank policy, but today’s rate cut puts SEK in a more vulnerable position. Our view remains benign on the krona beyond the short-term as we see three cuts by the Fed this year, but EUR/SEK might re-test the 11.84 October highs soon. A break higher, would make the all-time highs at 12.00 as the next key resistance. We think that the chances of the Riksbank revamping FX sales via the FX reserve hedging programme would increase exponentially above 11.85.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more