- Quick take

Korea’s fourth quarter GDP shrinks on weak exports, private spending

- 26 January 2023

- South Korea

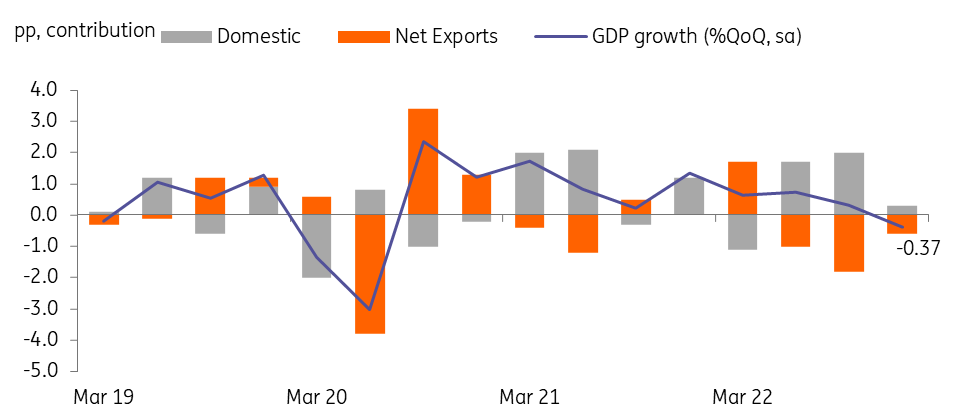

Real GDP dropped sharply as expected, recording a -0.4% decline in the fourth quarter vs 0.3% in the third. Sluggish exports and private consumption were the main reasons for the contraction We don't expect domestic and external growth conditions to improve meaningfully this quarter, thus the Bank of Korea should hold policy steady over the coming months

| -0.4% |

Real GDP% QoQ seasonally-adjusted |

| As expected | |

Korea's weak growth is likely to continue into this quarter

Korea's fourth quarter GDP contracted for the first time since the second quarter of 2020. We think that the impact of the cumulative interest rate hikes along with fading reopening effects have begun to slow down private consumption while weak global demand conditions are hurting Korea's exports.

Private consumption fell 0.4% with declines in both goods and service consumption. The debt service burden on households will not be relieved any time soon since Korea's households are highly leveraged and more than 70% of the outstanding household loans are based on floating rates. As such, the rate hike by the Bank of Korea in January will weigh on consumption this quarter. Also, we expect the unemployment rate to rise quite meaningfully in the first half of the year, thus household incomes are likely to worsen.

Meanwhile, construction and facility investment rose 0.7% and 2.3%, respectively, mainly due to the completion of pre-ordered projects. Forward-looking construction orders and machinery orders data have declined over the last few months, and we expect investment to decline this quarter. The credit crunch has eased a bit since late December, but many investment plans have already been cancelled or trimmed down due to the high level of funding costs and uncertain global conditions.

For external components, exports and imports both fell significantly by 5.8% and 4.6% each. Weak global and Chinese demand drove not only the decline of semiconductor and petrochemical exports but also the sluggish imports, as more than 40% of imports are for re-exports. We do not expect these weak global demand conditions to turn around sharply during the first half of the year. China’s reopening is key for Korea’s exports, but the positive impact will likely materialise in the second half of the year.

Korea GDP contracted in 4Q22

GDP forecast

With a fairly sharp contraction last quarter, we revised up the first quarter GDP forecast slightly, mainly on the back of a technical rebound. But we still think that GDP for this quarter will contract or at best stagnate. The contribution to net exports is expected to improve mainly due to a sharper decline in imports, but domestic demand is expected to worsen. Private consumption is likely to shrink, while investment is also expected to decline. Thus, we maintain our annual GDP growth forecast of 0.6% year-on-year in 2023.

BoK watch

The Bank of Korea will likely stand still on monetary policy from now on due to the weak growth but may also keep its hawkish stance for a while. Inflation still remains around the 5% level and upside risks are high. But we think that if GDP continues to contract this quarter then the BoK could consider a rate cut later this year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more