- Quick take

South Korea: 1Q23 GDP rebounds due to private consumption and exports

- 25 April 2023

- South Korea

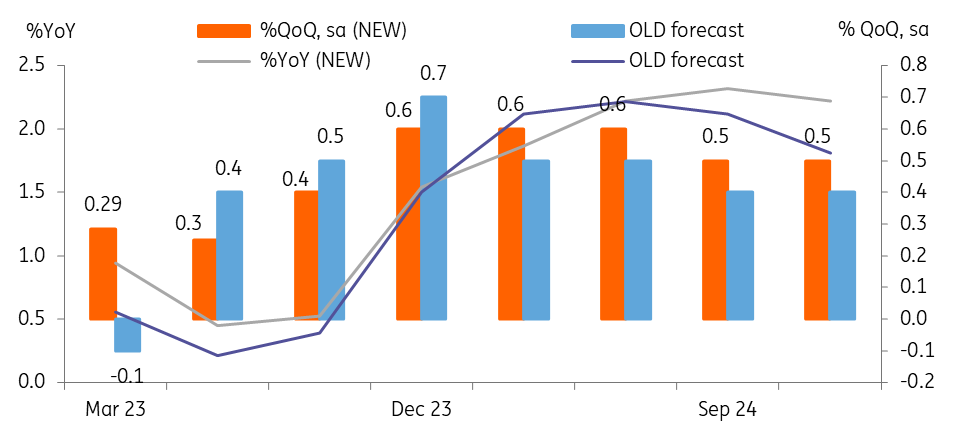

South Korea has avoided a technical recession as GDP expanded 0.3% QoQ in 1Q23. Upside surprises came from private consumption and exports. We have revised our annual GDP forecasts for 2023 from 0.7%YoY to 0.9%.

| 0.3% |

1Q23 GDP%QoQ, sa |

| Higher than expected | |

Private consumption and exports rebounded solidly in 1Q23

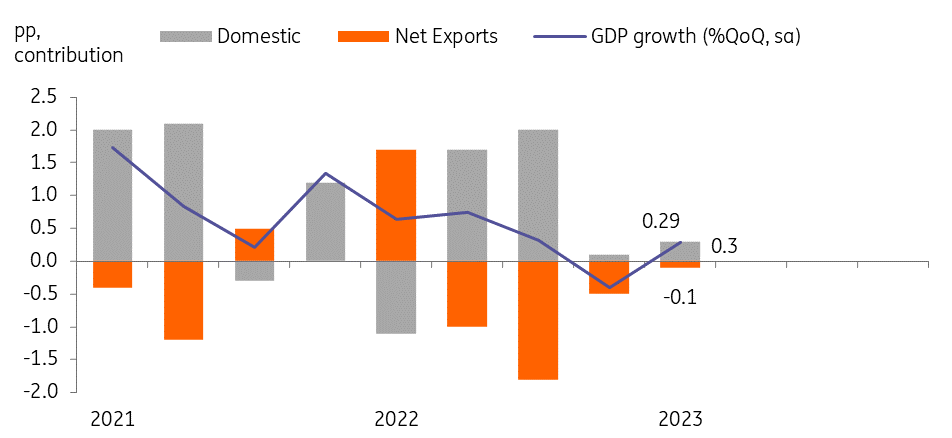

Private consumption was the main driver for the rebound, which rose a solid 0.5% QoQ sa (vs -0.6% in 4Q22). Given consumption for leisure and tourism services was particularly strong, we think the reopening boost has continued. Inflation came down rapidly from last year's peak and market interest rates also stabilised as the BoK has paused its rate increases since January. These factors probably boosted consumption last quarter.

In contrast, investment was a bit mixed. Facility investment was down -0.4% due to declines in machinery investment. Credit tightening and the semiconductor downcycle appeared to be the main reasons for sluggish facility investment. Forward-looking capex indicators such as capital goods imports and machinery orders are still declining, so we expect weak facility investment to continue this quarter. Meanwhile, construction gained 0.2% as pre-ordered residential projects were completed. Given the sharp cooldown in the real estate market and ongoing project finance issues, we believe construction growth is likely to turn negative from this quarter.

There was an upside surprise from exports, which rose 3.8% (vs -4.6% in 4Q22). This was in contrast to customs export data, which showed exports remaining in contraction during the first quarter. As customs exports measure value-term exports, the sharp decline in chip prices must have been the main reason for their weakness, while value-added terms of chip exports seemed to have held up better. The BoK also confirmed that strong exports of vehicles helped offset sluggish chip exports.

1Q23 GDP expanded mainly due to private consumption

GDP forecasts

As a result of the higher-than-expected 1Q23 GDP data, we have revised up our 2023 annual GDP forecast from 0.7% YoY to 0.9%. We expect growth to remain below potential for the rest of the year, mainly for two reasons.

Revising up 2023 annual GDP to 0.9% YoY

1) As mentioned earlier, construction activity is highly likely to turn negative, considering the sharp decline in forward-looking construction data – such as construction orders, permits, and unsold units. In particular, the number of construction permits and construction starts has declined significantly since 2H22, which should make residential construction weak over the next few years.

Construction growth is expected to turn negative from this quarter

2) Manufacturing activity is also expected to weaken in the near term. Inventories contributed a 0.2% gain in 1Q23, signalling a cloudy outlook for near-term production. Chip makers will likely cut production more drastically to adjust inventories from this quarter as announced by major chip makers early this year. Automobile production has been solid due to improvements in supply-chain constraints and catch-up demand but will be hit by both the U.S. demand slowdown and the U.S. IRA Act from 2H23.

On a brighter note, China’s reopening should have a positive impact on Korea’s growth from 2H23 when China’s construction cycle is expected to improve more meaningfully and as more Chinese tourists return to Korea.

BoK watch

Today's data will provide some relief for the Bank of Korea (BoK) as they can keep their focus on taming inflation. Thus we expect the BoK will strengthen its hawkish stance over the next few meetings. That said, given the slowdown in inflation, we don't expect the BoK to deliver another rate hike. Also, as we see growing downside risks for the economy on the back of weak local housing markets and intensifying tensions between the US and China, thus a potential BoK cut is still possible by the end of this year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more