- Quick take

- 26 September 2019

- Singapore

Singapore production still falling

What was supposed to be just a small decline turned into a 7.5% fall from the previous month, throwing our stabilization theory into doubt. Electronics continues to do most of the damage.

| -7.5% MoM |

Aug Production-8.0%YoY |

| Worse than expected | |

A bad figure, but narrowly based

After several months of roughly stable production which had begun to drag trend rates of growth back into positive territory, the 7.5% seasonally adjusted monthly decline in the August production figures come as a blow to our hopes that the worst of the global tech slump has passed.

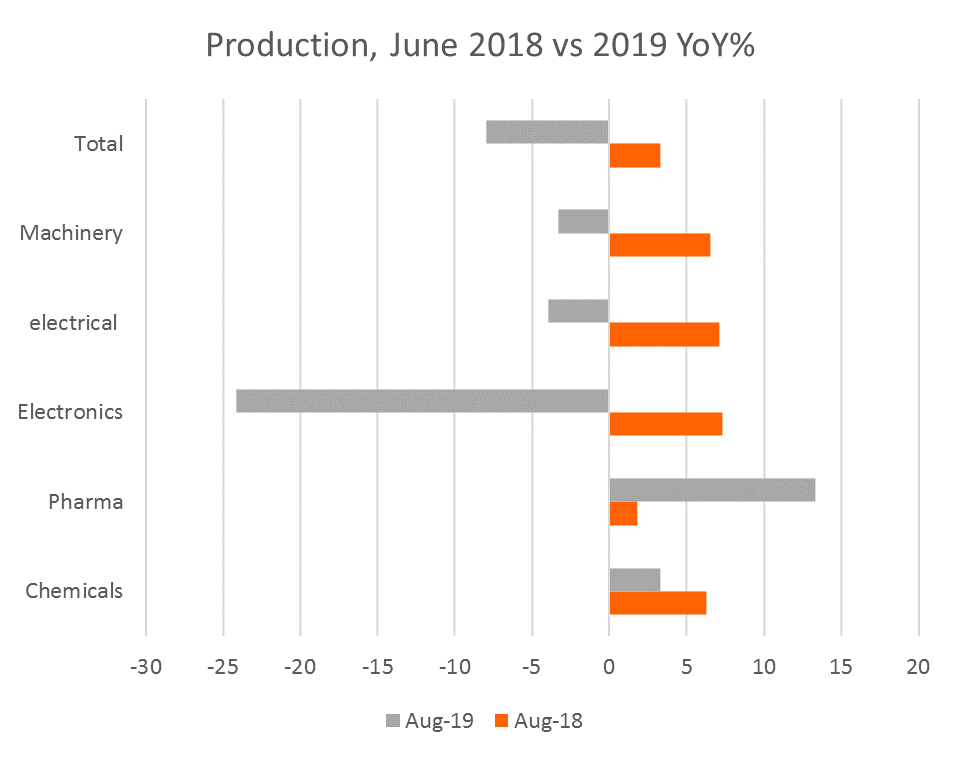

Please note that we are not blaming the trade war for this weakness. If that were the case, we might expect to see declines in all production sectors - we don't. The weakness is, as was the case earlier this year, highly concentrated in the electronics sector, and within this, semiconductors, which fell by 29.6%YoY. In July, semiconductor production had recovered to +1.4%YoY.

If we are to blame the trade war for any of this, it may be that the latest round of US tariffs on Chinese consumer electronics goods had messed with seasonality in semiconductor production as producers try to run ahead of tariffs on these goods. If this was the case, then we might expect some sort of return to trend, albeit at a lower level in the months ahead. But this is just speculation at this point and does not tally with what we are seeing in the export sector, which has also been a little more positive.

Where the weakness lies

GDP probably in technical recession

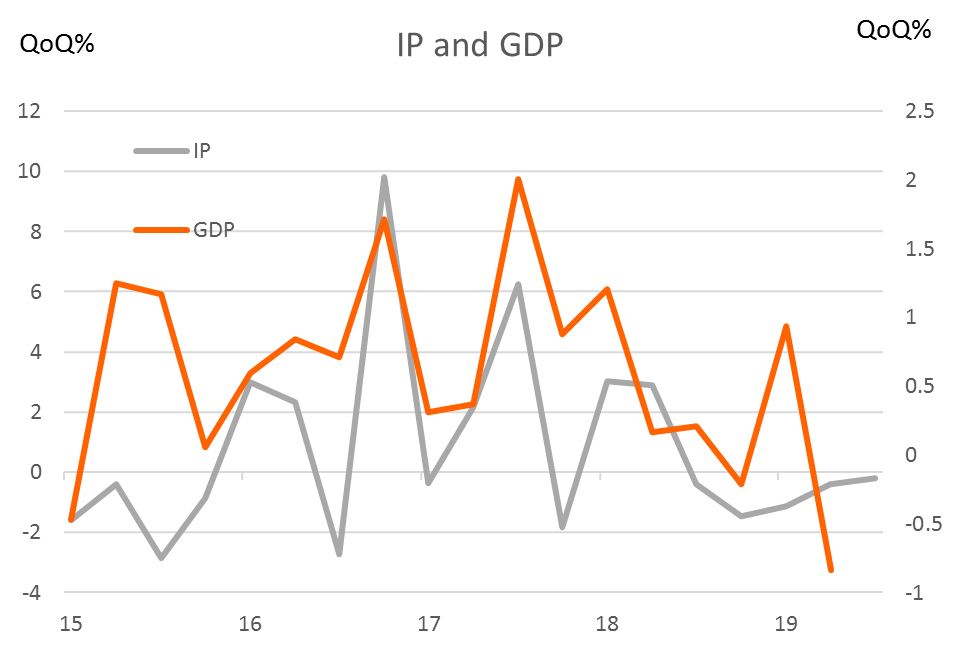

Adding in the latest production figures and a rough guess for September, we can come up with an estimate for industrial production growth for the quarter as a whole. And even with a September bounce, this now looks as if it will be another negative quarter. The overlay of industrial production with GDP is not exact, but it is sufficiently close that a second consecutive negative quarter of GDP is also now looking likely.

That would suggest that GDP is in a technical recession. But even if the data recovers enough to avoid this, the bigger picture is that Singapore activity is still very weak. Narrowly avoiding a recession would be an arbitrary achievement and not one to celebrate.

For 2019, full-year GDP will probably now register only 0.3% growth, even with a bounce in 4Q19 and a negative total is not impossible. We had been looking for growth of 0.7%.

Industrial production and GDP (QoQ%)

MAS needs to ease

The Monetary Authority of Singapore (MAS), which is due to reset the SGD nominal effective exchange rate path and band in October, is, in our opinion, bound to ease from the moderate appreciation it currently has in place. Given how long this policy has been in place while the economy has languished, there is an argument for any policy adjustment to err on the aggressive side. It will be another six months before the MAS is due to make a further adjustment, so underdoing it now will only condemn the economy to a longer period of inappropriately tight policy and slow growth.

There is also a growing argument for some fiscal stimulus. Singapore's financial strength is unparalleled, so the real question is where to aim any stimulus. Given the uncertainty surrounding the global environment and business investment, a more effective stimulus than accelerated depreciation or payrolls tax cuts might be through household tax rebates or cuts in public service charges. But either way, some small temporary stimulus can't do any harm and could help to alleviate some of the strain on the economy whilst conditions remain unfavourable.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 27 September 2019

- This bundle contains 4 Articles