- Quick take

Turkey: Signals of recovery in industrial production

- 14 March 2019

January IP data recording its first positive reading for six months is another signal of a bottoming out following the sharp adjustment in economic activity in late 2018.

| 1.0% |

IP growth(sequential change in January) |

The December 2018 industrial production (an a seasonal and calendar adjusted basis, SA) index, having been at its lowest since early 2017, recovered by 1% MoM in January. This was its first positive reading for six months. This can be viewed as a signal of gradual direction change after the August volatility that caused a significant adjustment in economic activity. Manufacturing stood out as the major driver of the improvement, contributing +1.0ppt to the headline. The contributions of "electricity, gas, steam and air conditioning supply" and “mining and quarrying” were slightly negative and positive respectively, offsetting each other. "Other transport equipment", dominated by defence industry products, provided a 0.7ppt lift to seasonally adjusted manufacturing performance.

Calendar-adjusted industrial production growth in January, on the other hand, turned out to be -7.3% YoY, slightly better than the market consensus.

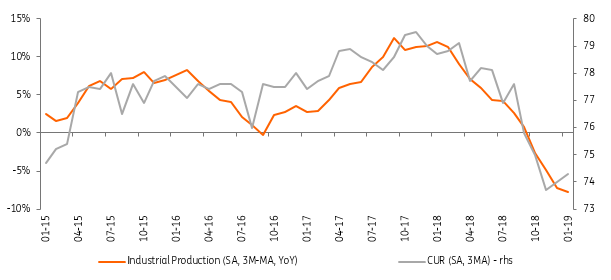

IP vs Capacity Utilization Rate

Across broad economic categories, all the groups that recorded negative growth rates in December turned positive in January. Intermediate goods production was the major driver of the monthly IP growth, at +2.2% MoM (with a 0.7ppt contribution to the headline), followed by energy at +1.4% MoM. Durable consumer goods production, likely reflecting the government’s decision to extend temporary tax cuts (on white goods, furniture and automobile) was also positive, recording 1.1% monthly growth.

Overall, the January IP data recovering from a low base is another signal of bottoming-out. This is evidenced by (1) a slowing credit adjustment, (2) recovering business confidence and sectoral confidence indicators, albeit at a slower pace, (3) recent stability in CUR and improvement in PMI, and (4) momentum loss in the falls in white good and automobile sales. The government has announced a number of stimulus measures in recent months for both households and companies. These include a higher-than-expected minimum wage hike, social security premium support for firms, and SME lending packages at lower interest rates that can be helpful for an economic recovery.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more