- Quick take

- 12 June 2020

Sharp fall in UK GDP unlikely to be regained quickly

Social distancing constraints, consumer and business caution, as well as Brexit, all pose challenges to the UK economic recovery. This is set to keep the pressure on the Bank of England to continue expanding its balance sheet, and we expect a further increase in its quantitative easing programme next week

The UK economy shrank by a little over 20% in April, according to the latest monthly GDP estimates, and this follows an initial 5.8% decline back in March.

Today's data won't necessarily come as much of as a surprise to markets - it shows the damage was a little greater than expected, but the reality is that markets have become fairly desensitised to big numbers over recent weeks. We know too that April was the first month to be fully encompassed by the lockdown. But these figures are nevertheless shocking, and it goes without saying that this kind of fall in activity is virtually unprecedented, either in scale or speed.

The UK economy shrank by a little over 20% in April, according to the latest monthly GDP estimates

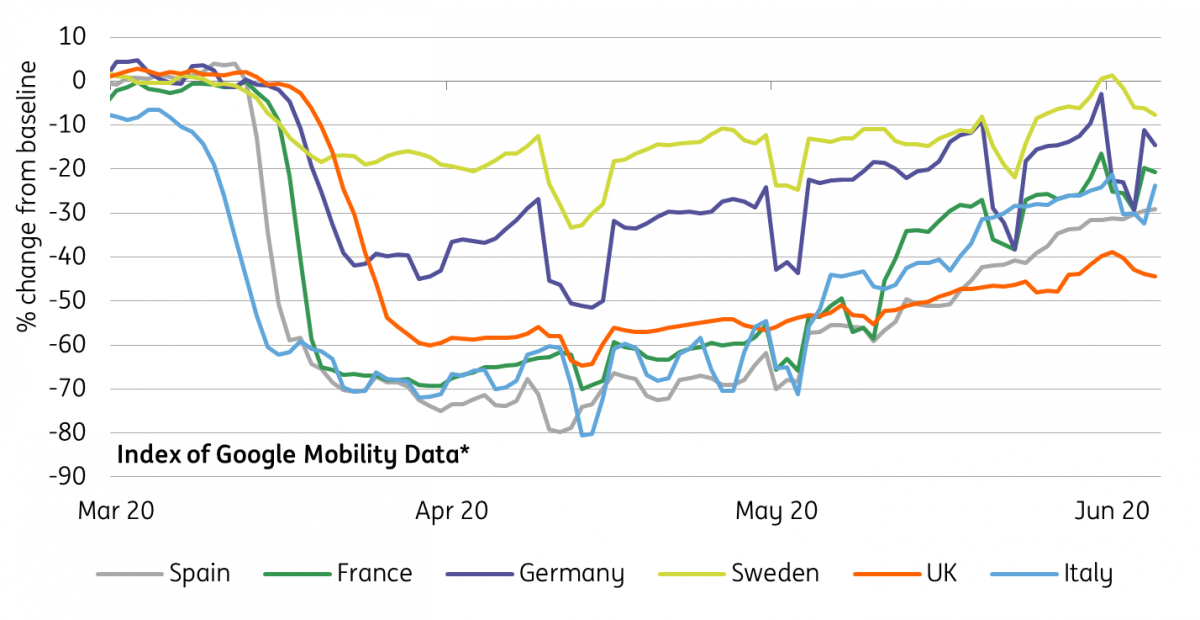

So what next? Well, April was undoubtedly the low point in activity, although it doesn’t appear to have been a substantial rebound so far. Using Google’s Mobility data, which has proven to be a reasonable proxy of output levels so far, overall travel to places of economic relevance only modestly recovered through May - potentially pointing to a small growth rebound somewhere between 3-5% across the month.

Mobility levels are still down quite a bit relative to other parts of Europe, including the likes of France, Spain and Italy. That’s perhaps not surprising given that Britain has so far allowed fewer sectors to reopen, but it does mean when it comes to second-quarter GDP, we’re like to see a sharper overall decline in the UK.

Lockdowns compared: Google's Mobility Index

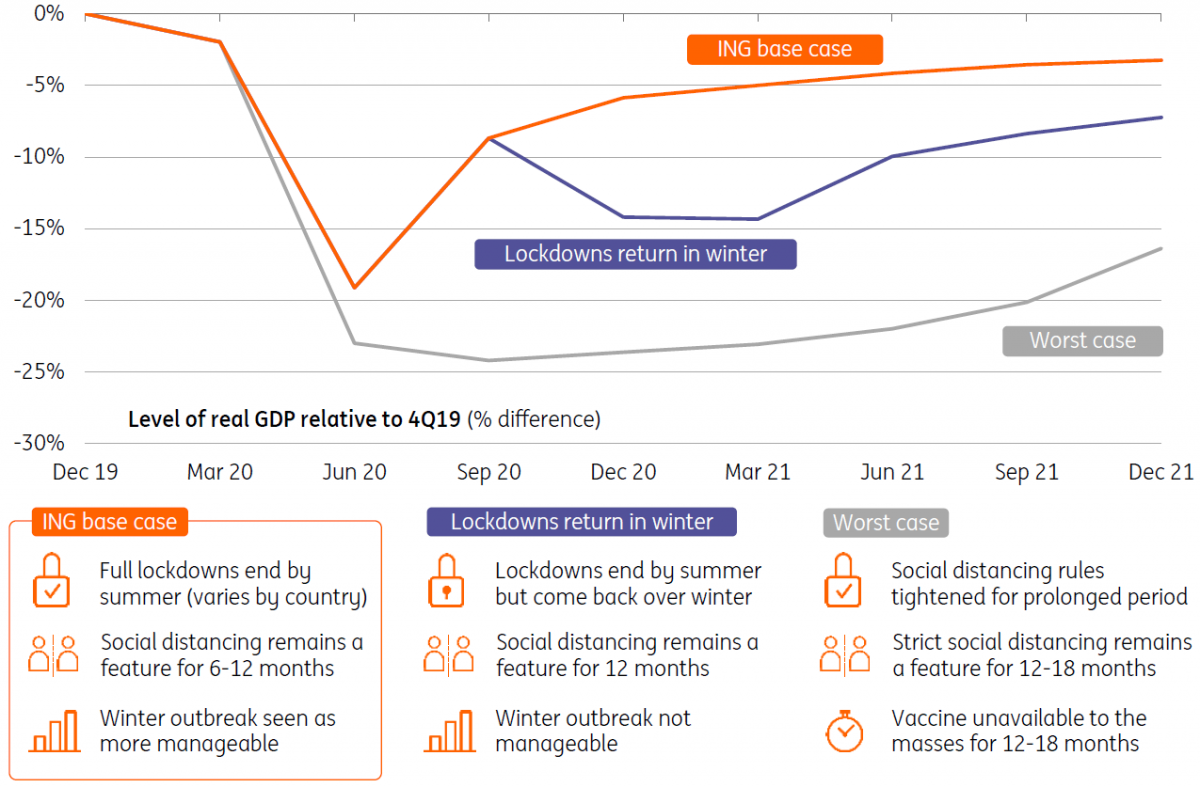

We’ll probably see a more pronounced rebound during the third quarter as a broader range of businesses are expected to reopen. But even then, the economy will remain well below its pre-virus size, and we don’t think it will be until late 2022 or 2023 until it has returned to those levels.

Brexit also looks set to pose a serious challenge later this year, with supply chains likely to see some initial disruption when the transition period ends

A key reason for this is that social distancing constraints are here to stay. While this is essential to help prevent a second wave of the virus - and avoid an economically-damaging return to stricter lockdowns, it nevertheless means many firms will be operating below normal operation levels for the foreseeable future. This could be a particular challenge for parts of the hospitality and retail sectors, where many businesses rely on a high volume, low margin model. At the same time, we suspect consumers and businesses will maintain higher levels of savings/adopt a more cautious approach to spending until the risk of a second wave has gone.

Brexit also looks set to pose a serious challenge later this year, with supply chains likely to see some initial disruption when the transition period ends. Importantly that applies even if there is a free-trade agreement, where the main story remains that the UK economy will be leaving the customs union and single market.

Three potential paths for the UK economy

All-in-all then, there are few bright spots in the UK outlook at the moment, and we currently estimate that 2020 growth will come in just shy of -9%. All of this means the onus on the Bank of England is to continue with its large stimulus package.

Importantly the Bank will soon be nearing the limits of its current £200bn QE package. That suggests an expansion is on the cards at next week’s meeting, and we wouldn’t be surprised to see an expansion in the region of £125-150bn.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more