- Quick take

- 12 March 2024

- Turkey

Turkey’s current account deficit sees a sharp drop in January

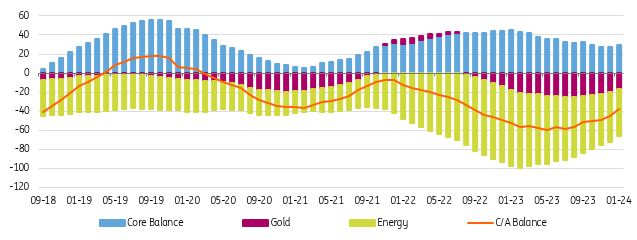

The downward trend in Turkey's current account that began after the peak last July has continued, with a drop seen in the 12-month rolling deficit to US$37.5bn from US$45.4bn a month ago

Current account (12M rolling, US$bn)

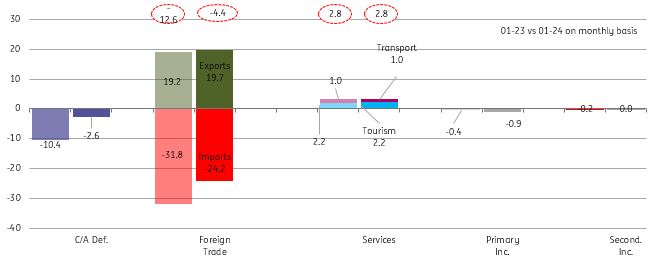

Turkey's current account posted a deficit at US$2.6bn in the first month of this year, better than the market consensus of US$2.8bn. In the breakdown compared with the same month of last year, we see i) a sharp drop in the gold trade deficit from US$4.5bn to US$0.6bn, ii) an improvement in the net energy trade with a fall in deficit to US$5.1bn from US$7.7bn and a turn in the core trade balance to a surplus at US$1.6bn from a slight deficit. While these items turned out to be the major drivers of a recovery in current account balance, flat services income and a drop in primary income limited the extent of the rebound. Accordingly, the 12-month rolling deficit recorded a sharp decline to US$37.5bn (which translates to around 3.4% of GDP) from US$45.4bn a month ago given a large base in January 2023.

Breakdown of current account (monthly, US$bn)

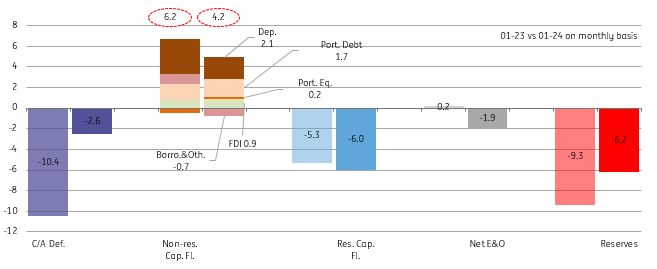

On the capital account, net identified flows turned mildly negative at US$1.8bn. Errors and omissions outflows that have made a return since September were at US$1.8bn in January. With the monthly current account deficit and capital outflows, official reserves recorded the first decline since May 2023 elections at US$6.2bn.

In the breakdown of the monthly data, residents’ movements drove the outflows with i) portfolio investments at US$0.8bn, ii) acquisition of financial assets abroad at US$4.0bn, and iii) trade credits advancing by US$0.8bn.

Non-resident inflows continued, thanks to US$0.5bn in portfolio investments in the bond and equity markets, US$1.4bn issuances abroad by banks and US$2.1bn deposited by foreign entities in the banking system. Net borrowing was slightly positive as corporate debt repayments almost offset borrowing by banks. Accordingly, rollover rates stood at 55% for the former and 255% for the latter in January (vs 93% and 121% respectively on a 12-month rolling basis).

Breakdown of financing (monthly, US$bn)

Overall, the improvement in the current account deficit in January was attributable to the significant drop in foreign trade deficit. Accordingly, the downward trend that started after the peak in the last July continued. The foreign trade deficit dropped by more than 40% to US$7.0bn in February from another large deficit in the same month of the previous year, according to the provisional customs data released by Ministry of Trade. The data implies a continuation of the recovery in February's current account given the large deficit in the same month of last year at US$9.0bn. Additional, the Central Bank of Turkey (CBT) introduced additional macroprudential measures targeting growth in TL commercial loans and general-purpose loans. The positive impact of these decisions on the balancing of demand factors is likely to be observed with a lag, and should support the trend in the current account.

When looking at the capital account, foreign portfolio inflows have stagnated since late December. Given the priority among policymakers of replenishing reserves and higher external financing needs, the capital flow outlook will remain key over the coming period.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more