- Quick take

- 11 April 2024

- Hungary

Services inflation heats up in Hungary

Hungary’s headline inflation in March inched slightly lower, but the rate of monthly repricing accelerated somewhat. Services inflation was the biggest driver, creating an unfavourable turn in the inflation structure

| 3.6% |

Headline inflation (YoY)ING estimate 3.6% / Previous 3.7% |

| As expected | |

Monthly headline inflation rose slightly compared to previous months

Inflation in Hungary continued to fall in March, with the Hungarian Central Statistical Office (HCSO) reporting a higher inflation rate than the market consensus. In contrast, the incoming data matched our own expectations exactly. Compared with February, headline inflation fell by 0.1ppt to 3.6% year-on-year, but at the same time the monthly repricing was 0.8%, indicating a slight acceleration compared to the (already high) repricing seen in the previous two months of this year.

This means that inflationary pressures in the Hungarian economy are generally persistent, as achieving the sustainable 3% inflation target would require monthly inflation rates of around 0.2-0.3%. At the same time, core inflation rose by 0.8% month-on-month, suggesting that price pressures were particularly strong among items included in the core basket – which is clearly an unfavourable turn, as it points to stickier inflation.

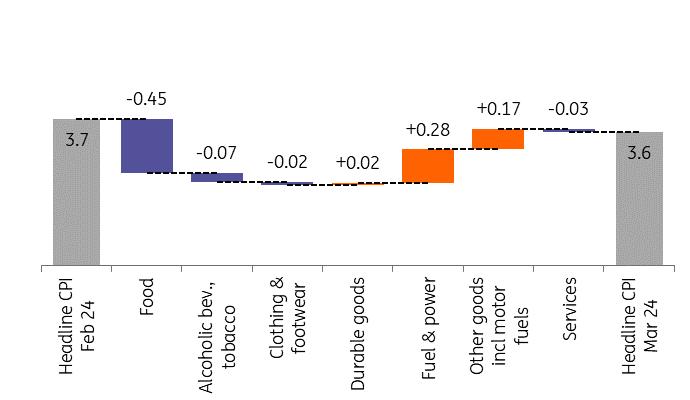

Main drivers of the change in headline CPI (%)

The details

- Food prices rose only by 0.1% MoM, which brings the annual food inflation rate to 0.7%, the lowest level in the post-Covid era. On a monthly basis, prices of unprocessed foods increased, while prices of processed foods decreased, indicating a divergence within the food component.

- Fuel prices increased by 2.1% MoM on the back of higher global oil prices, while household energy prices likewise increased on a monthly basis. The latter might be only a one-off phenomenon coming from the methodology.

- Prices of durable goods remained unchanged in March, despite a weakening of the forint. So, this can likely be explained by the easing of global inflationary pressures combined with weak external demand.

- Services prices rose by 1.8% MoM, which brings the annual services inflation rate to 9.9%. Television subscription and telecom services providers hiked prices in a retrospective manner, hence the large – although expected – monthly increase. In terms of the annual headline inflation rate, the services component explains 72% of total inflation.

The composition of headline inflation (ppt)

Core inflation drops, but the monthly repricing doesn’t paint too rosy a picture

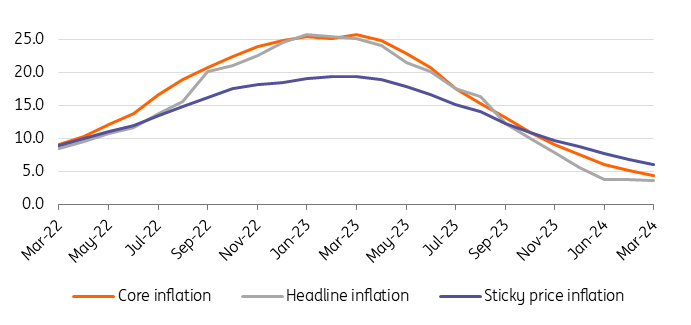

Core inflation decelerated by 0.7ppt to 4.4% YoY in March, while the National Bank of Hungary's measure of inflation for sticky prices also decreased, displaying a reading of 6.1% YoY. This is the result of a 0.8% MoM increase in core inflation, which is the highest monthly repricing seen since April 2023. If we exclude the processed food item, this narrowed core inflation measure came in at 1.1% on a monthly basis, creating headaches from a monetary policy point of view.

Of course, the biggest driver among the core basket was services inflation. This component alone accounted for 0.5ppt of the entire monthly repricing. As we’ve been continuously pointing out, March and April are particularly sensitive months to higher monthly services repricing, which is not a unique phenomenon. What is important, however, is that many services providers hike prices in a retrospective manner, using last year’s average inflation – which was extremely high in Hungary – as an anchor. In this regard, we expect services inflation to remain hot in April as well, on the back of higher repricing from tourism, financial, and telecom services providers.

Headline and underlying inflation measures (% YoY)

We expect two rounds of reflation this year, driven mostly by base effects

Going forward, we expect monthly price adjustments to be slightly weaker than the levels observed over the past three months. This is primarily attributable to seasonal price changes in food and clothing items. We also anticipate a moderation in fuel price increases, mainly due to the recent talks between the government and MOL (the biggest wholesale fuel retailer in Hungary). On the other hand, services price increases are likely to continue, and we therefore expect headline inflation to remain around its current level in April.

However, we still continue to anticipate a two-round reflation process, largely driven by base effects, with the first round likely starting in May and the second commencing in October. Consequently, our December 2024 inflation forecast remains in the range of 5.5-6.0% YoY, currently leaning closer to the upper end of the range.

Nevertheless, it is challenging to make accurate projections for the second half of the year. The Hungarian economy appears weak while labour market tightness has eased, potentially slowing the favourable wage growth process. The cautionary motive of households persists, with the gross savings rate still being at historically elevated levels. In this regard, a significant rebound in consumption is yet to be seen, and all of these factors are therefore likely to provide a headwind to inflation in the coming months.

A new challenge for monetary policymakers

From a monetary policy perspective, the latest inflation figure poses a challenge to policymakers. In our view, rate cuts will undoubtedly continue in the coming months – but the extent of the cuts remains highly uncertain. If market conditions are favourable in the coming weeks, the central bank may even have the opportunity to cut the base rate by 75bp, the same as in March.

However, the structure of inflation (especially the 1.1% MoM core inflation excluding processed food) and developments in the core markets yield environment – with particular attention paid to changes in interest rate expectations regarding the Fed – could prompt the National Bank of Hungary to be more cautious. Nevertheless, we continue to expect the central bank's last rate cut in 2024 to take place in June. This could be followed by a holding period, which would help ensure that monetary policy is tight enough to maintain both price and financial market stability over the longer term in an environment of rising inflation.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more