September rate cut on the cards as Polish inflation falls in July

According to a flash estimate, CPI inflation in Poland declined in July to 10.8% year-on-year (ING forecast: 10.9%, market consensus: 10.9-11%) from June's 11.5%. We are on track to reach single-digit CPI in August and a rate cut by the National Bank of Poland in September

The main driver behind the July CPI decline was food prices, which dropped by 1.2% month-on-month, likely driven by seasonal declines in the prices of vegetables and fruits. They deducted 0.6pp from the yearly CPI. Energy carrier prices were unchanged month-on-month, but their year-on-year slowdown deducted 0.2pp from yearly CPI.

Fuel prices, on the other hand, rose by 0.4% MoM, despite holiday price promotions, adding 0.2pp to yearly CPI.

We estimate that July brought a further sharp decline in core inflation excluding food and energy prices – to around 10.5% YoY from 11.1% in June, which deducted 0.2pp from yearly CPI.

CPI outlook: short-term positive, mid-term mediocre

Inflation is on the path to a single-digit print as early as September. The decline in inflation is largely related to the receding of external shocks. After dynamic disinflation in the second quarter, we expect a slower decline in CPI inflation during the second half of the year. If oil prices remain at current levels (above $80/bbl), we may see fuel prices rise again after the summer holidays.

The medium-term inflation outlook remains uncertain, in part due to likely increases in regulated energy prices beginning in 2024 and continued double-digit wage growth (given a significant minimum wage increase next year).

Monetary policy outlook

Despite some easing in the monetary policy stance in July, the major central banks (such as the US Federal Reserve and the European Central Bank) remain cautious in their assessments of the inflation outlook and see risks of price increases being perpetuated at elevated levels, maintaining a hawkish stance and willingness to tighten monetary policy further. They also point out that the medium-term inflation outlook is not so optimistic, due to overly strong labour markets, demographics, fiscal expansion, and the earlier loosening of the policy mix, among other factors.

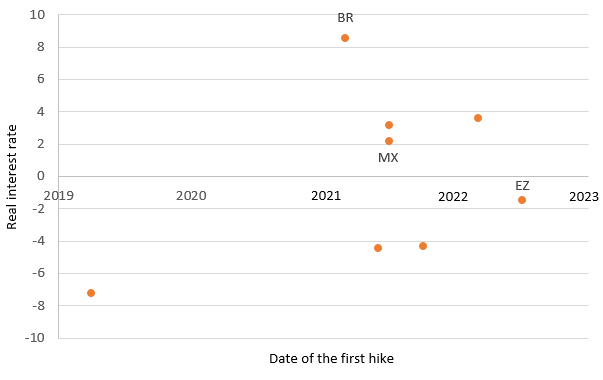

Real interest rates in emerging and core economies

Emerging market central banks are likely to start rate cuts ahead of developed markets'

The situation is slightly different in emerging economies. Some are already cutting interest rates (e.g. Chile, Hungary). The National Bank of Poland (NBP) is focusing on the expected decline in inflation to single-digit levels and says it is ready to cut interest rates after the holidays. This is despite the central bank's projection indicating that the decline in inflation to the target will be a long-term process.

In our view, the NBP should cut rates by 50-75bp in 2023 and begin easing in September. However, monetary easing will prolong the period for inflation to return to target and we see important mid-term risks.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap