Reserve Bank of Australia takes another breather

Pausing for a second consecutive meeting, today's rate decision is in line with some better inflation data this month and means the Bank can respond to future data events with less fear of overdoing the tightening

| 4.1% |

Cash rate targetUnchanged |

| Lower than expected | |

Not clear why market was even looking for a hike

It is a genuine mystery to us why there was a small majority of forecasters looking for a hike at today's meeting. We certainly were not. The June inflation data came in better than most of the expectations, including on the core measures. So that alone should have been enough to keep the RBA on hold. And none of the other data since the last meeting have been particularly alarming. Sure, the labour data wasn't exactly soft, but it wasn't super-strong either, and the unemployment rate while still very low, was stable from the previous month.

In the statement in July, Governor Philip Lowe noted that further tightening "will depend upon how the economy and inflation evolve", and in the event, the economy and inflation tended to indicate that they were on the right track. For a central bank that has been keen to give the economy a chance where at all possible, there was simply no good argument for a hike today.

There will be better excuses to hike than existed this month

More hikes are possible - probably one, maybe two

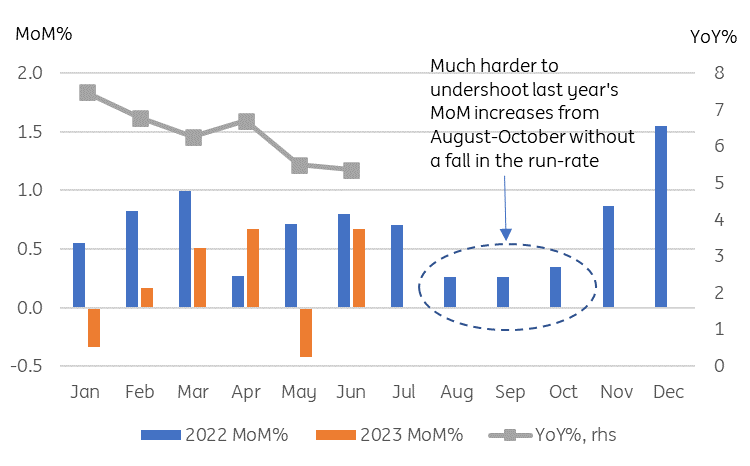

That doesn't mean that there is no chance of any further tightening in this cycle. And while the June inflation figures were lower than expected, the month-on-month increase was not even close to what is required to get inflation back to target. And that will have to change.

Today's statement notes that there is still a chance for some further tightening and that the RBA will "continue to pay close attention to developments in the global economy, trends in household spending, and the outlook for inflation and the labour market" We think that this broad assessment means the RBA can be a bit more choosy when it does decide to tighten again. If it responded to every tiny mishap in the data, then rates would rapidly rise, and by the time the economy did finally show more evidence of turning, the odds are that they would by then have gone too far. This way, they are giving a soft landing the best chance of happening.

Base effects will become far less helpful after the July CPI release later this month, and the July reading of CPI will also incorporate substantial electricity tariff hikes which means that inflation could backtrack higher for July and August readings. That puts a September rate hike firmly into the frame, and possibly leaves the door open for a further hike before the base effects should turn more helpful once more - absent seasonal supply chain shocks, which is harder to take for granted in these climate-changed times.

So we will be looking for one more rate hike to 4.35% at the RBA's next meeting in September. And we will be reserving judgement on another and hopefully final one in October or November, if the macroeconomy remains resilient and if inflation is making insufficient progress lower. The September meeting would be Lowe's last meeting as governor, as the new Governor, Michele Bullock, will take over from 18 September. It would be a nice handover gift if the tightening were largely completed before she takes the helm.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap