- Quick take

- 9 December 2021

- Russia

Russian inflation in November: mounting pressure in durables is the key concern

November CPI data brought both positive and negative news. Stabilization of local food price growth and the one-off nature of the spike in services brought some relief, but mounting upward price pressure in non-food products and high core CPI are causes for concern. The CPI trend is testing the upper border of the Bank of Russia's base case.

| 8.4 |

November CPI, % YoYup from 8.1% in October |

| As expected | |

Russian CPI edging higher, but not everything is gloomy.

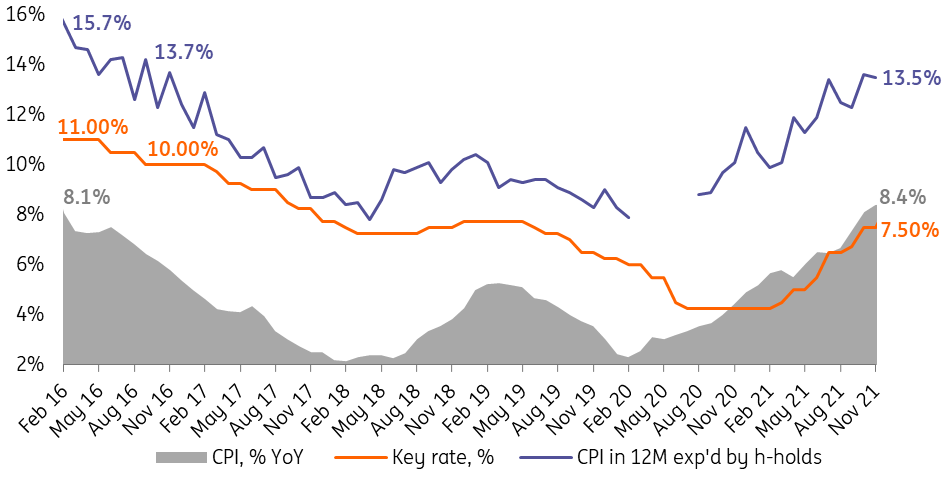

Russian CPI picked up from 8.1% YoY in October to 8.4% YoY in November, broadly in line with what was suggested by the weekly data. According to Bank of Russia data released earlier, higher inflationary pressure is to be seen amid stable, but elevated, houiseholds' inflation expectations (Figure 1). There are several takeaways from the data, both positive and negative.

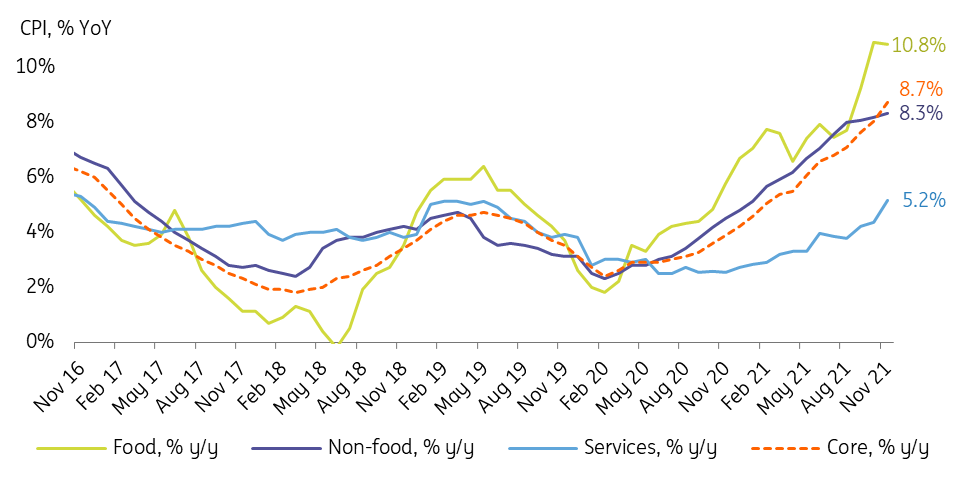

On the plus side, food price growth stabilized at 10.8-10.9% YoY (Figure 2), admittedly an elevated rate. The global context of rather stable key food commodities (Figure 3) and slowing growth in the broad global food basket (Figure 4), combined with the higher base effect in local food prices, allows for optimism in terms of further trends.

Another positive development is that the acceleration in services price growth from 4.4% YoY in October to 5.2% YoY in November seems to be fully attributable to a one-off spike in prices for holiday tours to Turkey registered in the last fuul week of November. The recent weekly data covering the beginning of December points at normalisation of that item, leading to a significant deceleration in the overall weekly price growth from the abnormally high 0.46% WoW to 0.07% WoW.

At the same time, the structure of CPI also points to higher price pressure in the non-food segment. First, non-food CPI growth continues to gradually accelerate - to 8.3% YoY in November - despite a higher base effect. Mounting pressure is seen in a wide range of categories, including faster growth in gasoline prices. This does not fully explain non-food inflation, with the 2% depreciation of the average ruble exchange rate last month also a factor.

The strong pick up in core CPI growth, from 8.0% to 8.7% YoY, is also raising questions, as higher prices for holiday tours to Turkey could have contributed no more than 0.15-0.20 percentage points to the growth rate, according to our estimates.

Figure 1: Headline CPI keeps climbing, while households' expectations are stable, but elevated

Figure 2: Food price growth stabilized, services spiked due to one-offs, but mounting non-food price growth is a concern

Figure 3: Global context favours further easing in local food prices

Figure 4: Broad basket of global food commodities also seems favourable

One-off factors will subside, but demand-side factors are becoming more pronounced

Going forward, the inflationary picture appears mixed. On the plus side, the strong price growth in the food and services segment does not appear sustainable. The new Omicron variant of Covid is indeed a risk factor to the supply side, but given that it is apparently less lethal, and that Russia has pushed up the vaccination rate from 33% in 3Q21 to 47% currently, it should not lead to higher risk of new lockdowns.

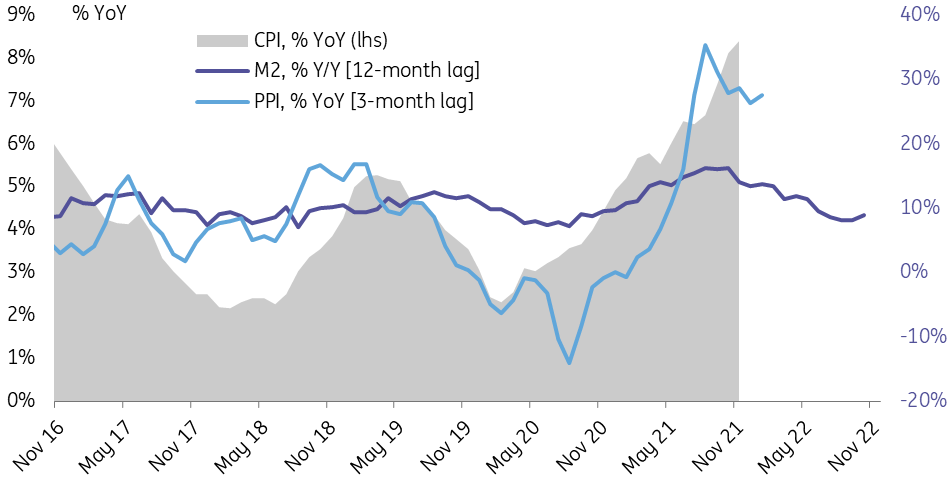

Looking at the standard forward-looking indicators of CPI, such as monetary supplu growth and PPI (Figure 5), consumer inflation appears to be approaching its peaks. However, "boys who cried peak" this year (ourselves included) should keep a number of risks in mind.

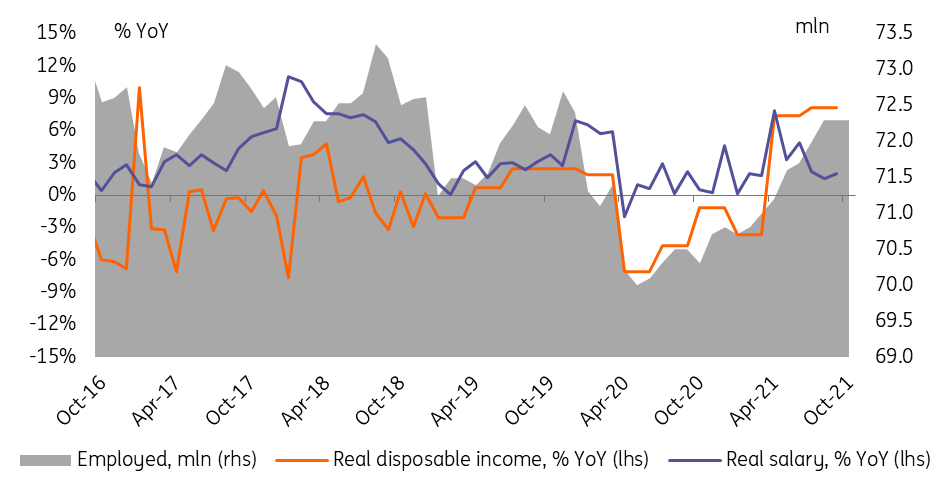

We see two demand-side risk factors that may keep the central bank and the markets on their toes. First, the recent economic data for October confirmed that the labour market in Russia has tightened to pre-Covid levels (Figure 6), both in terms of number of employees and the unemployment rate. Anecdotal evidence suggests growing demand for labour in the construction and services sector, which may lead to inflationary pressures through the wage channel.

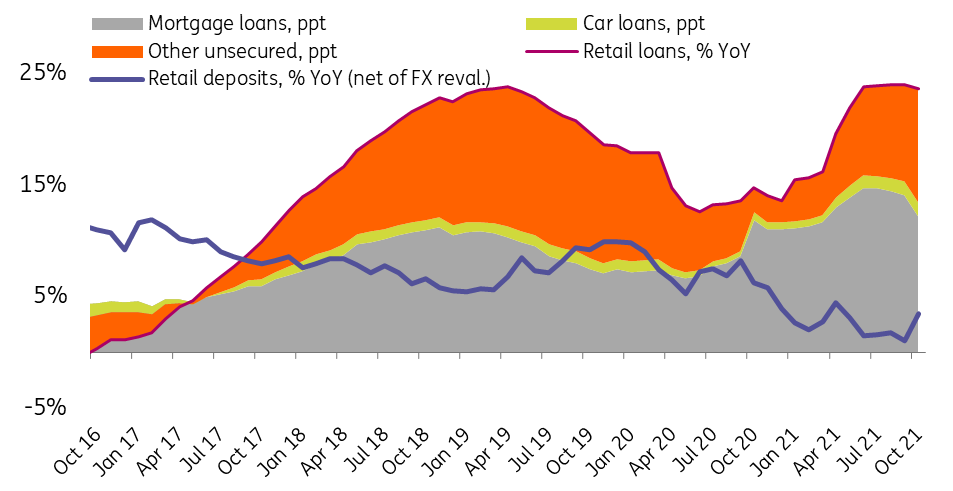

Second, the banking sector data for October (Figure 7) suggests no cooling in retail lending, particularly in the unsecured consumer segment despite the macroprudential tightening, while deposit growth is close to historical lows despite a recent pick-up.

The list of supply-side risks includes uncertainties related to FX rate moves, various Covid scenarios, and global supply chain frictions.

As a result, we see year-end CPI at 8.0-8.5% this year, while the year-end 2022 indicator has a risk of exceeding the CBR's 4.0-4.5% target range.

Figure 5: Forward-looking indicators call for stabilization of CPI...

Figure 6: ...but a tight labour market...

Figure 7: ... and low savings rates are raising the importance of monetary drivers of CPI

CPI trend is testing CBR's base case scenario

In our view, the current inflationary trend is testing the upper border of the Bank of Russia's medium-term forecast. The year-end 2021 forecast of 7.4-7.9% should not be over-emphasized, given its extremely short-term nature, while the longer-term commitment to bring CPI down to 4.0-4.5% by the end of 2022 is more important. Given the elevated inflationary expectations of local households and corporates, the tight labour market and high appetite for borrowing vs. savings, persisting global uncertainties, and the local economic policy priorities reiterated by the president, we believe the Bank of Russia's decision on 17 December should gravitate towards the upper border of the 0-100 bp key rate hike range implied by the CBR's previous communication.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more