- Quick take

- 3 March 2021

- FX Russia

Russia: higher oil does not mean better outlook for ruble

The $9/bbl upgrade in ING’s 2021 oil price forecast boosts Russia's annual exports by $25 billion. But it will be sterilised by an additional $15bn of FX purchases and elevated capital outflows on local and foreign challenges. We see no reason to improve our USD/RUB forecasts of 72-73 for 1H21, though stronger financial stability is somewhat reassuring

Higher oil price benefits the budget, not the FX market

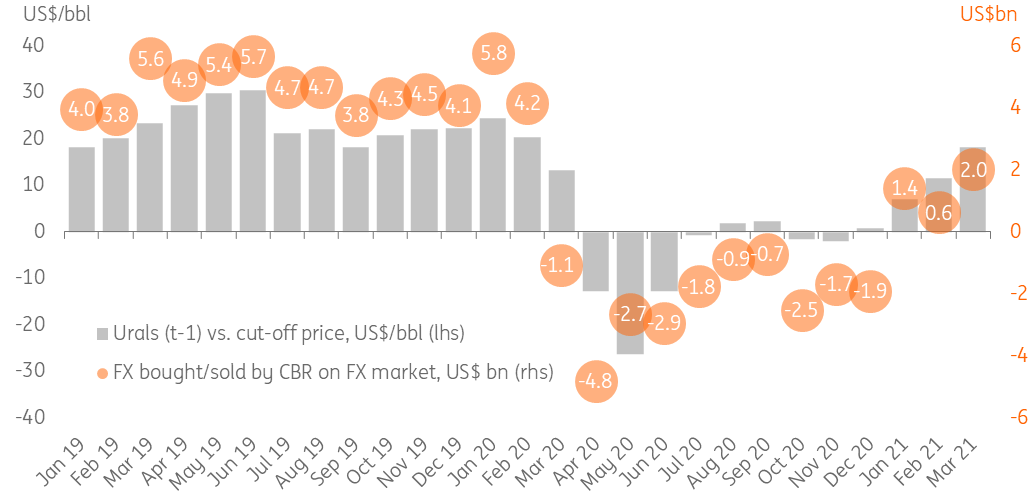

The Russian Finance Ministry announced an increase in monthly FX purchases from $0.6bn in February to $2.0 bn in March (Figure 1), which is higher than the $1.6bn Reuters consensus and slightly higher than our expectations. The hike in the fiscal-rule FX purchases, which will be conducted by the CBR on the market, reflects a material $7/bbl increase in the average monthly oil price in February and the upward revision to the last month's oil revenues of the budget. We positively take the fact that the budget is almost fully benefiting from the high oil price environment despite the earlier warnings of reduced oil exports in February. At the same time, the March FX intervention announcement is generally in line with our take on the relative neutrality of oil prices for the ruble's performance. Year-to-date, the ruble is up just 1% against the US dollar despite a 21% increase in the oil price.

Following the robust performance of the commodity markets, ING has upgraded its oil price forecasts for 2021 by around $9/bbl, which corresponds to our Urals price assumption of $63/bbl vs. the previous call of $54/bbl. According to our calculations, that means a material $25bn increase in the annual current account forecast to $70bn for 2021. Meanwhile, the budget will be the key beneficiary of this increase, as more than half of the extra current account ($15 bn) will be sterilised by the FX purchases under the fiscal rule, as we now see annual FX interventions at $25bn this year vs. previous expectations of $10bn. The remaining $10bn of extra current account is subject to risks of elevated private capital outflows, as suggested by the disappointing January data.

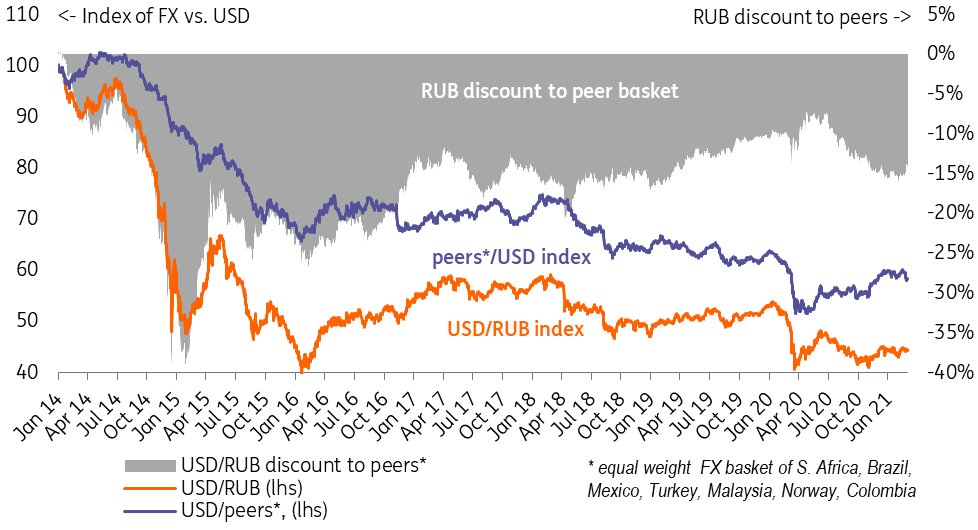

While failing to have a direct positive effect on the ruble, it may help to insulate it from additional external volatility through reinforced macro stability perceptions. The total foreign debt of 32% of GDP, public debt of under 20% of GDP, liquid FX savings in the sovereign fund at 8% of GDP, expected current account surplus of 4.5% of GDP combined with FX underperformance in 2H20 (Figure 2) should make the ruble less vulnerable to global volatility associated with the US Treasury sell-off than most of its emerging market peers. At the same time, higher oil prices are unlikely to insulate the ruble from the pre-existing Russia-specific challenges, including foreign policy uncertainty (the recent US sanctions were a relief but the risk of further tightening has not been removed) and private capital outflows stemming from low local confidence.

Figure 1: At current oil prices, monthly FX purchases have reached $2bn

Maintaining a cautiously constructive view on the ruble, but risks of volatility are high

The high oil price environment is unable to directly translate into a stronger ruble, but it helps to boost Russia's macro stability advantage relative to its EM peers, potentially limiting the negative impact of the recent volatility on the global bond markets. We therefore maintain our cautiously constructive expectations of USD/RUB 73.0 by the end of 1Q21 and 72.0 by mid-year. Meanwhile, Russia-specific challenges to the capital account, including persistent foreign policy uncertainty and low local confidence, remain a risk factor, potentially challenging the year-end target of 73 and causing the ruble to trade in a wide range throughout the year. The February balance of payments data, to be released on 10 March, will be the next important data point in assessing the prospects of capital outflows.

Ruble has been underperforming peers in 2H20 on elevated country-specific risk perception, stabilized year-to-date

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more