- Quick take

Russian CPI hits the 4% target, may go higher in the near term

- 6 November 2020

- Russia

The increase in CPI in October is not surprising, given the ruble depreciation and low base effect of 4Q19, and should be largely discounted by the central bank. But the mounting pressure from agriculture prices and signs of extended fiscal easing at the regional level are watch factors for 2021, which may minimize the key rate downside

| 4.0% |

October CPI, YoYup from 3.7% YoY in September |

| As expected | |

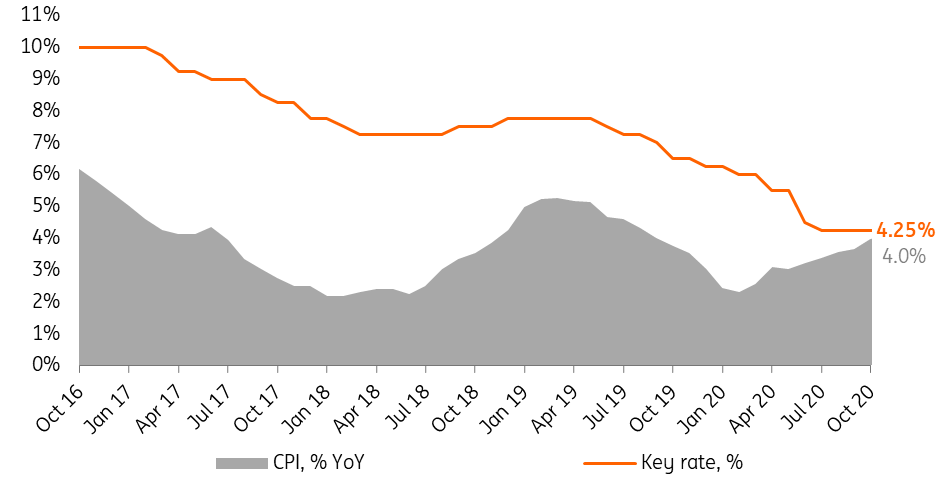

The pick-up in CPI from 3.7% year-on-year in September to 4.0% YoY in October is neither dramatic, nor unexpected. Out of the 0.3 percentage point acceleration 0.2ppt are attributable to the low base effect of 2019, which saw a material deceleration in 2H19 on tight budget policy, stable markets, and delayed tariff indexations. The remainder is the continued effect of RUB depreciation, which totaled 2.4% to USD and 1.6% to EUR in October. Given this, and the renewed weakness in consumption, Bank of Russia treats the current spike in the CPI as temporary, which means that this near-term spike in inflation is unlikely to reverse the generally dovish stance of the Russian central bank. Nevertheless, looking deeper at the structure of CPI, and in the newsflow around the fiscal policy we see factors that could potentially worsen the CPI outlook for 2021 and minimize the downside to the 4.25% key rate.

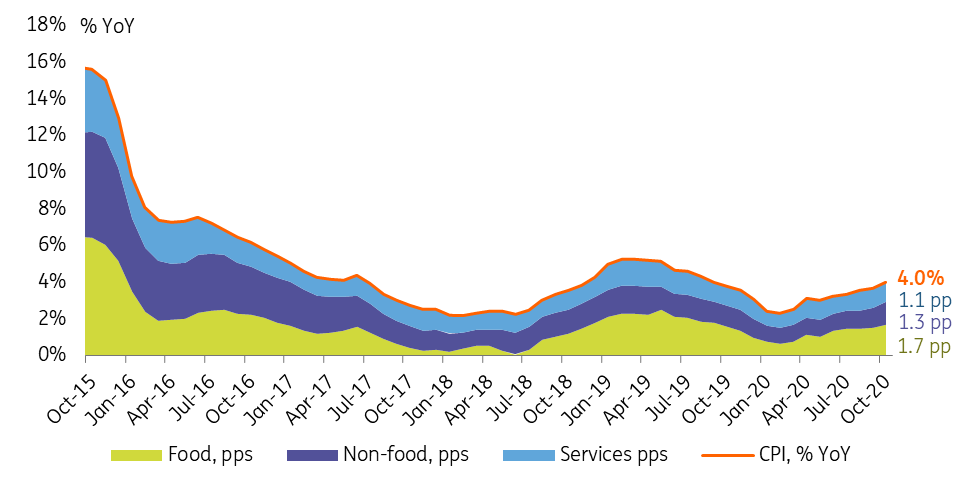

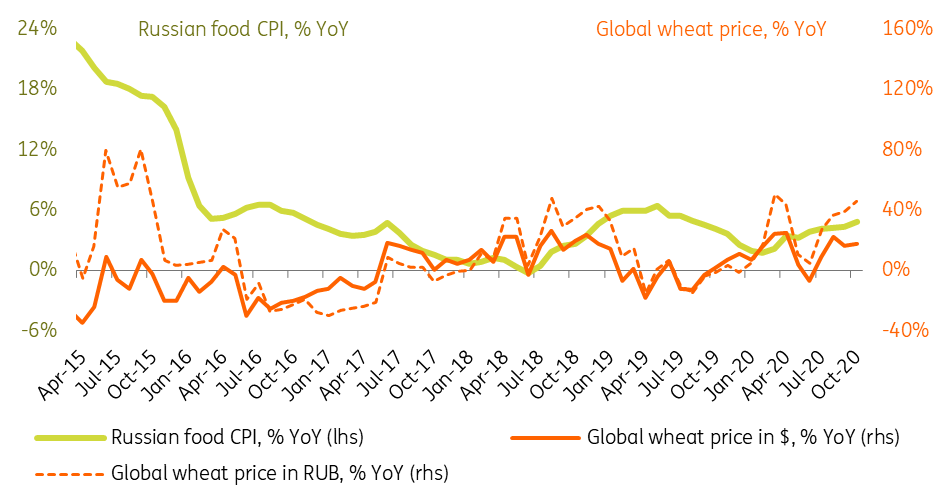

- The acceleration in food CPI from 4.4% in September to 4.8% YoY in October is overall in line with the base effect. However we note excessive growth in prices for sugar, sunflower oil, and other grain-related items. This correlates with the pick-up in the global argiculture commodity prices (amplified for Russia by the ruble depreciation) since mid-year due to climate conditions, disruption in supply chains and strong demand from China. As a rule of thumb, each 10ppt of global wheat price growth in RUB terms translate into a 1.0ppt increase in Russian food CPI and 0.4ppt in overall CPI. As of now, this indicator is up 40-50% YoY. It remains to be seen if the cost-input price pressure could be fully offset by the weakness in consumer demand.

- The non-food CPI is up from 3.8% to 4.2% YoY, exceeding the levels suggested by the base effect, and RUB depreciation is the usual suspect, with most pressure seen in consumer electronics and household chemicals. Also noteworthy, there is a second wave of pharma inflation, coinciding with a material deterioration of reported Covid infections and death rate since October. With further deterioration of the epidemiology context and the increased RUB volatility in the beginning of November, the near-term outlook on non-food CPI is also heading up.

- The basis for the below-target CPI expectations of 3.5-4.0% by the central bank (and our forecast of 3.0-3.5%) is the expected weakness in domestic demand for 2021, and we generally agree with that view. However, it appears that consumption may yet receive an additional boost from the budget policy. While on the federal level the budget is guiding for consolidation, the recent proposals to ease the requirements for the Russian regions to boost debt and plans of the city of Moscow to boost borrowing in 2021, may suggest that the deficit of the regional budgets (normally staying around 2% GDP and fully covered by the federal transfers) may increase to allow broader support to the economy than suggested by the federal budget draft. The regional budgets are in charge of spending on healthcare, education, housing, non-pension social payments, and partial support to the industrial sectors. Also, their revenues depend on the corporate profit tax, personal income tax, and property tax. A softening in the regional budget approach could be a factor limiting the desinflationary effect of demand in 2021. To remind, parliamentary elections are scheduled to take place in September next year. We would not exclude that in this context the consolidated budget balance could temporarily decouple from the the federal trend.

Figure 1: Russian CPI is picking up, mostly on base effect; CBR remains dovish, expecting a reversal in 2021

Figure 2: Food and non-food products are the main contributors to the acceleration

Figure 3: Global grain prices are contributing to the upward pressure in the local food CPI

The recent higher-than-expected ruble volatility, combined with higher global grain prices and stronger-than-expected effect of the second wave of Covid suggests that the year-end CPI could be in the 4.0-4.2% range, higher than our initial 3.7% forecast. On the one hand, given the temporary nature of most of the near-term pro-inflationary factors, this should not trigger an immediate reversal in the dovish stance. On the other hand, a possible easing in the regional budget policy could be a challenge to the disinflationary view for 2021, limiting the scope for further cuts in the key rate. We are now less certain that Bank of Russia will be able to proceed with the key rate cut at its upcoming December meeting.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more