Russian consumption: recovery stalls on reopening of foreign tourism

Retail trade dropped 2.7% YoY in August, underperforming the July result and consensus expectations. We are not disappointed as it may reflect the reopening of outward tourism to some popular locations. Above-expected salaries, continued social support and positive lending dynamics should be supportive of consumption in 4Q20

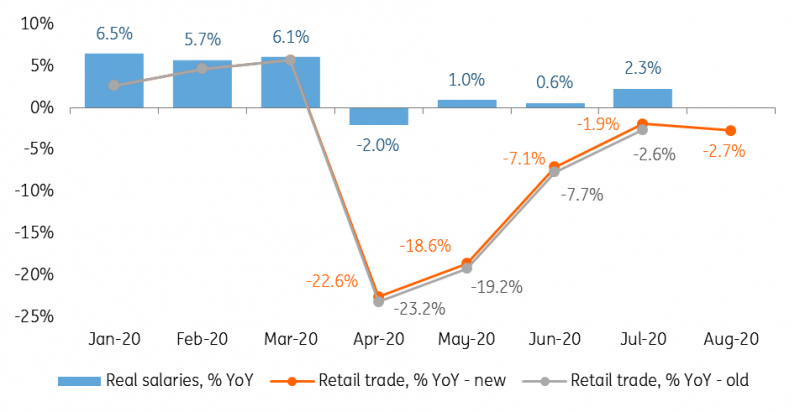

Russian retail trade posted a 2.7% year-on-year drop in August, underperforming the consensus forecast of -1.7% YoY, but very close to our expectations of -2.5% YoY. While indeed the period of fast recovery in consumption seems to be over, we see several reasons not to be disappointed in the released numbers:

- After months of lockdown, several foreign tourist destinations, including Turkey, have been made available for Russians since the middle of August. Spending on foreign travel (imports of services) could have reached US$1-2bn last month. Without the reopening, the local retail trade growth in August could have been 2-4 percentage points higher. Or, to be more precise, the lack of foreign travel could have propelled the April-July retail trade growth numbers by up to 8ppt YoY. Unless there is a second wave of strict lockdowns, the local consumption numbers are likely to remain under pressure of normalisation in foreign travel.

- Salary growth numbers for July (this data comes with additional lag) significantly outperformed expectations, posting a 2.3% YoY jump in real terms after a 0.6% YoY increase in June. Though this data is more relevant to the larger businesses and state sector, and the situation in the SME sector could be different, other sources of income were likely supportive as well: the budget fulfillment data for 8M20 point at continued acceleration of spending on pensions and social security. The unemployment level increased modestly by 0.1ppt to 6.3%.

- While there is no banking sector data available (it is scheduled to be released later on Monday), Governor Nabiullina indicated in broad terms that lending growth both in retail and corporate sectors continued in August, which should also be supportive of consumption. The upcoming banking sector data may also bring additional colour on the household savings (previously it showed continued accumulation despite some outflow into cash and into higher yielding financial instruments).

- The earlier estimates for retail trade for April-July have been improved by 0.6-0.7ppt YoY, including from -2.6% YoY to -1.9% YoY in July, suggesting that the drop in smaller businesses was not as deep as expected.

- Structurally, the deterioration of retail trade dynamics in August is seen only in the food segment (from -2.0% YoY in July to -4.1% YoY in August) amid the improving performance in durables (from -1.7% YoY to -1.2% YoY). This also speaks against a material deterioration in households' purchasing power.

Figure 1: Real salary growth positive, retail trade trajectory revised slightly upwards

With a -5.1% YoY drop in 8M20, retail trade is on track to meet our full-year target of -4.0%. While the period of fast recovery in the consumption trend is over, it will remain supported by a relatively defensive position of the large corporates, continued social spending and subsidized lending. Our understanding of the current consumption trend does not go against the slightly less dovish CBR stance at the recent monetary policy meeting.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap