Russian consumption improves in February, adding credibility to the hawkish CBR

Russian consumption surprised on the upside in February, responding well to the budget support and gradual improvement on the labour market. This adds credibility to the hawkish stance of the CBR for now. Meanwhile, our longer-term concerns regarding lacklustre production and high dependence of household income on the budget did not evaporate

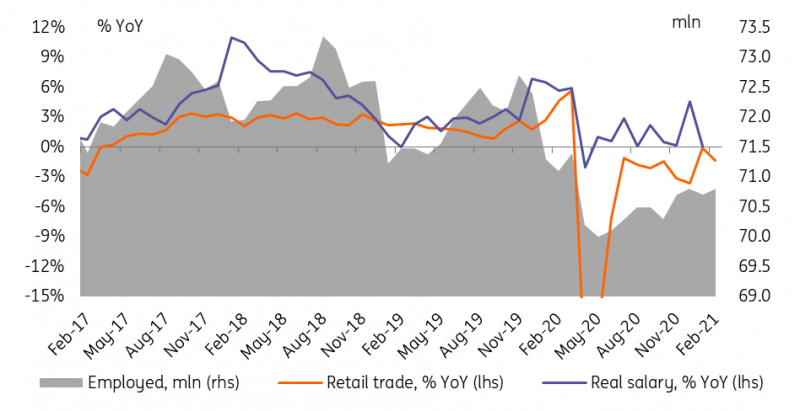

Russian consumption statistics for February 2021 came in weaker than January – largely due to the high base effect of leap February 2020 – but still higher than most of our and consensus expectations. Retail trade dropped 1.3% year-on-year vs. our forecast of -2.5% amid a decline in the unemployment rate by 0.1 percentage point to 5.7%, while real salaries managed to show a 0.1% YoY increase vs. our forecast of -1.2% YoY. Given the lack of banking sector data available for cross-referencing, we have the following preliminary conclusions.

- Improvement (adjusting for the calendar effect) in the retail trade dynamic chimes with the recent statement by the Central Bank of Russia indicating a faster-than-expected recovery of local demand, also supported by the delayed reopening of foreign travel.

- We would also add that this recovery corresponds with the recent pick-up in budget spending, which is now showing a high growth rate of 24% YoY on a 12M trailing basis and is recently focused mainly on non-pension social benefits. We continue to expect that the April revision in the budget draft will result in additional social spending being added.

- Labour market conditions also seem to be gradually improving, though not rapidly. The number of employed has recovered to 70.8 million, which is still 0.6 million below the pre-Covid level. Real salary growth of 0.1%, positive despite the rapid pick-up in CPI to 5.2% YoY in January still suggests that the 4.6% YoY spike last December was a one-off event, most likely related to front-loaded bonus payouts ahead of the increase in taxation for high earners.

- Our longer-term concerns regarding household income growth remain. To remind, the share of household income directly dependent on the budget has increased to the historical high of 36% in 2020, up from 33% in 2019 and 22% in 2006. At the same time, the 2020 enlarged budget spending was at a post 2009 high of 40% of GDP, with household income support measures at a historical high of 22% of GDP. For 2021-23, fiscal consolidation is guided even if the rate of it may be smoother than suggested.

- The producer response to accelerated budget spending seems to be more restrained. To remind, industrial output showed little improvement in February, and neither did the construction sector, which continued to show a flat performance outside the booming housing construction sector. Meanwhile, the recent announcement by the Finance Ministry on the likely investments of RUB1 trillion from the National Wealth Fund in 2021-23 into the local infrastructure projects might add some optimism in the state-driven sectors going forward.

Figure 1: Retail trade is trending up amid gradual improvement in employment and still positive real salaries

Figure 2: Producer side less impressive despite fiscal support

The recovery in household consumption lends credibility to the recent CBR statement, that the recovery in local demand adds to near-term inflationary risks and requires a more hawkish approach. Meanwhile, the lack of a noticeable improvement in the income trend, its high dependence on the fiscal support, as well as the lacklustre performance on the producer side remain challenges to a robust recovery in the overall activity in the longer term.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap