- Quick take

- 3 June 2021

- Russia

Russia to catch up on FX purchases, increasing ruble’s sensitivity to trade and capital flows

Russia will prop up FX purchases by US$1.3bn to US$3.0bn in June, slightly higher than expected, reflecting strong oil prices and volumes in May. This puts more focus on the current account, with strong exports and low outward tourism fighting against dividends and higher imports. Capital outflow, which has so far remained strong, is also a watch factor

| 221 |

June FX purchases, RUBbnup from May's RUB124bn |

| Higher than expected | |

Russian FX purchases above expectations in June

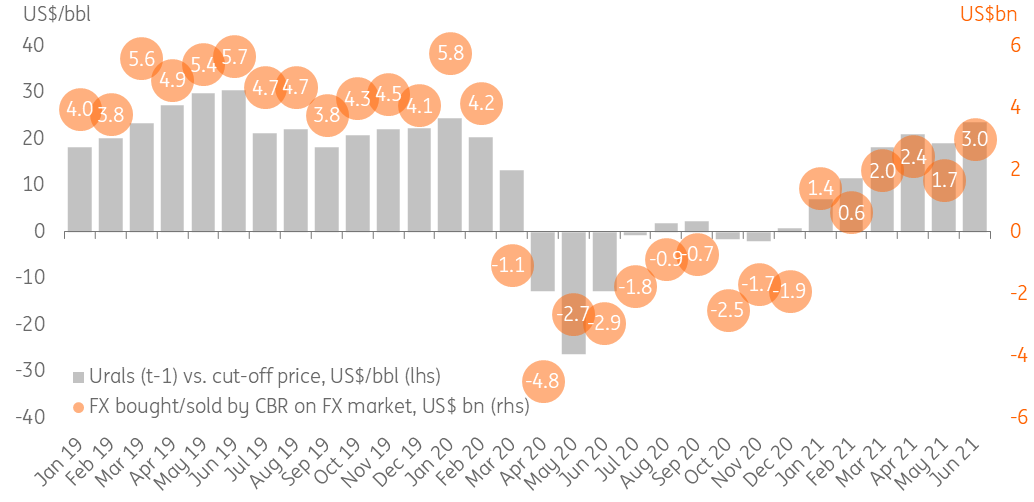

The Russian Finance Ministry announced an increase in monthly FX purchases from US$1.7bn in May to US$3.0bn in June (Figure 1). Our expectations, which were in the middle of consensus, suggested a more moderate increase to US$2.6bn.

In our view, the higher-than-expected increase in the FX purchases suggests that in addition to the US$5/bbl increase in the average monthly Urals price in May, the Russian trade balance and budget may have also benefited from increased volumes of oil production and exports. Given the stronger-than-expected oil price environment and signs of faster economic recovery, our budget balance expectations for 2021 (deficit of 1.2% of GDP) now has room for improvement.

The implications for the exchange rate, however, are not as straightforward, as the ruble is currently at the cross-roads of counterbalancing factors.

- On the positive side, we have strong oil prices and prospects of further growth in volumes (supportive of exports), extended ban on outward tourism to Turkey and Egypt – popular destinations (reducing imports of services) – a hawkish Central Bank of Russia, benign global mood, and easing in the foreign policy tensions ahead of US-Russia summit on 16 June (assuring the return of portfolio investments into OFZ in the amount of US$0.7bn in May), as well as the still glowing prospect of a reduction in the annual FX purchases in case of local investment out of the National Wealth Fund in the amount of US$4-5bn per year. The latter is not to be confused with the recent news on de-dollarization of the NWF, which in our view will be neutral to the market.

- On the negative side, the current account, which has so far has been strong on both oil and non-oil factors, is now about to come under pressure due to fast growth in merchandise imports (non-CIS imports were up 49% year-on-year in April, challenging our 18% YoY expectations for 2Q21) along with an economic recovery, and of seasonal dividend payments (we expect around US$7bn to be paid in favour of foreign shareholders from end-May till early August this year). Also, the net private capital outflow has remained sizeable so far (US$18.7bn over 4M21), suggesting continued obstacles to ruble appreciation. Finally, the uncertainties regarding the Fed stance at the upcoming months are also creating additional external risk factors for the EM space in the medium term.

Figure 1: FX purchases to catch up with oil price, putting the spotlight on other balance of payment items

We remain cautious on the ruble for the medium term

A strong oil price environment, easing in the foreign policy tensions, continued foreign travel restrictions and benign global EM-risk mood create favourable conditions for the ruble in the near-term, regardless of the higher-than-expected FX purchases in June. Meanwhile, the dividend season, galloping imports and persistently high private capital outflow could serve as obstacles to ruble appreciation this summer. We continue to see USDRUB 72-73 levels as attractive for building up FX positions.

The May balance of payments, to be released on 9 June, will be the next important data point to test this view. We expect a narrowing of the current account surplus amid persistent private capital outflow.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more