- Quick take

- 19 August 2019

- Russia

Russia: July activity disappoints

July was a weak month in terms of both consumer and producer trends despite the pick-up in budget spending. It remains to be seen whether this weakness continues into 2H19, but it could be an argument for further key rate cuts. The ultimate decision will still depend on whether global markets stabilize until September

| 1.0% YoY |

July retail trade+1.6% YoY for 7M19 |

| Worse than expected | |

Household consumption back under pressure

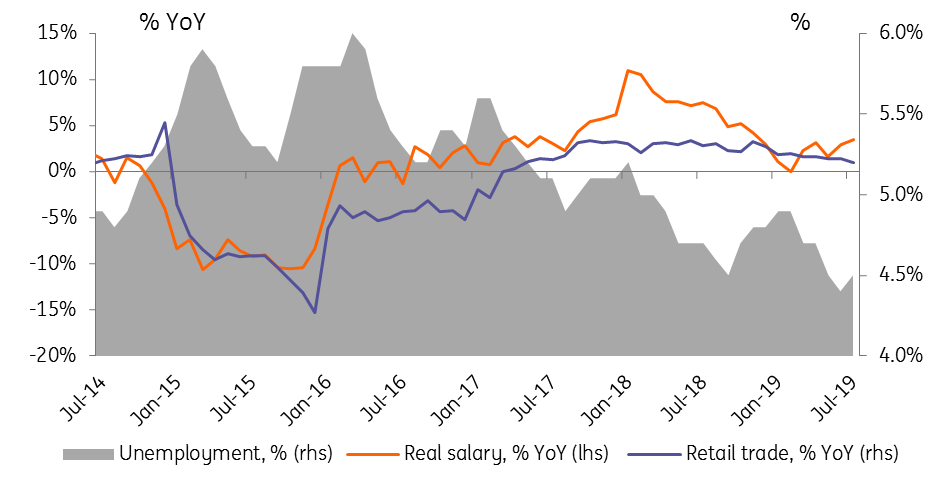

After stabilizing briefly at 1.4% year-on-year in May-June, retail trade growth slid to 1.0% YoY in July, underperforming the consensus forecast and our expectations of 1.6% YoY. The summer months are normally less indicative of the actual strength of consumer activity, as the latter is distorted by the summer vacation period, however the deceleration in the growth of airline passenger turnover from 11.4% YoY in June to 9.9% YoY in July does not allow for dismissing the weak local consumption data on higher spending abroad.

In terms of consumption fundamentals, the picture is also not quite clear.

- First, the acceleration in real salary (two-thirds of overall household income) growth from 2.9% YoY in June to 3.5% YoY in July seems positive, however the sector breakdown for June (the details come with a one month lag) suggests that the strong numbers of the last couple of months may have been propelled by the commodity extraction sector, which accounts for only around 2% of Russia's employees. Moreover, the data may have been distorted by the base effect of 2018 in the oil&gas extraction sector.

- Second, the data on lending for July is (regrettably and quite atypically) not yet available, but given the previous trends and the de-risk measures taken by the Bank of Russia, it would be safe to assume that retail lending growth has probably decelerated, further lowering the support to the consumption growth.

In terms of potential support factors to consumption, one can name the increase of pensions and salaries to the budget sector employees (around 60 million people, or 50% of the adult population), however it will take place only on 1 October, and the scale of indexation will be limited to 4.3% YoY (last year's inflation). Taking into account the increased volatility of the financial markets, which has already translated into ruble weakness, we, therefore, remain cautious on consumption growth for the coming months and reiterate our call that it will not be a major support factor to GDP growth this year.

Key indicators of the Russian consumer trend

Corporate activity remains weak... so far

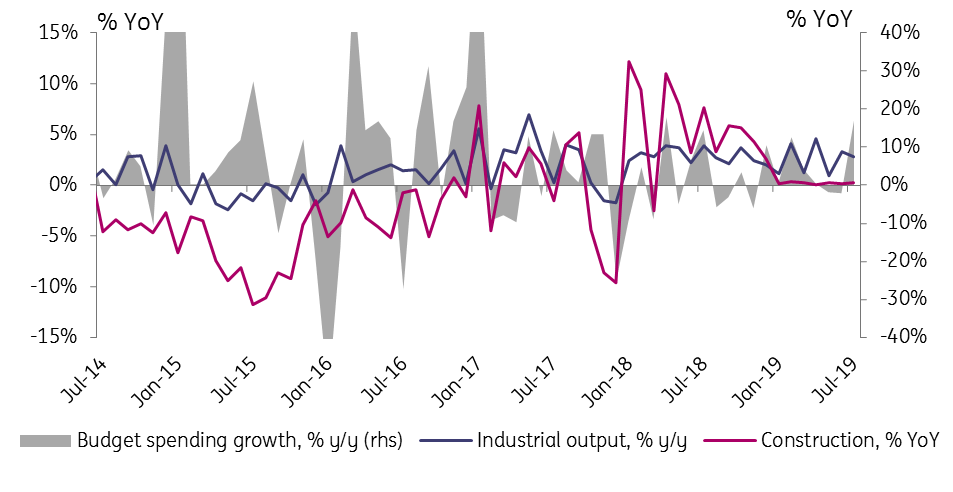

Corporate activity indicators for Russia generally disappointed, as the earlier reported industrial output data (+2.8% YoY for July, below expectations) was joined by the persistently negligible 0.2% YoY growth in construction. This suggests that the acceleration in budget spending from 2% YoY in 1H19 to 17% YoY in July has not yet translated into higher overall output.

The weakness in the key sectors in July apparently did not prevent an acceleration in the overall GDP growth rate from 0.8% YoY in June to 1.7% YoY in July, propelled by the higher output in the agricultural sector (that has experienced a climate-related shift in seasonality this year), and the non-key sectors, which may prove temporary.

As a result, the key hopes for the acceleration in GDP growth for 2H19 are related to the activisation of the National Projects driving the infrastructure-driven growth. Fixed investment growth has remained at a very modest 0.5-0.6% YoY in 1H19, but may accelerate towards the year-end.

Key indicators of the Russian producer trend

We believe the weakness in the consumer and producer activity in July may put the budget policy in focus - by reigniting the calls to accelerate state spending in 2019 and expanding the list of prospective local projects for investments from the National Wealth Fund starting in 2020. As a side note, the Bank of Russia (CBR) may also face calls from the real sector to ease the approach to monetary policy, however, we doubt that activity will play a major role in the decision making in this area.

In terms of the upcoming 6 September CBR meeting, we believe there is still the possibility of a key rate cut, as the current CPI trend points at further deceleration. However, we acknowledge that the recent deterioration of the mood on the global markets, which has already contributed to the RUB weakness in August, increases the chances that the CBR will opt for a halt in the rate-cut cycle. We would indicate RUB68-70/US$ as a 'threshold range' for the CBR's key rate decision, as those FX levels are very close to this year's lows, and reaching those might negatively affect inflationary expectations. In any case, given the increased market volatility, any clarity on the upcoming decision is unlikely to follow until the very end of August.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more