- Quick take

- 20 June 2019

- Russia

Russian household and corporate activity remain sluggish

May data on household income and consumption is slightly better than expected although this could be down to one-off factors. Corporate activity is clearly subdued but may see some support from the scheduled pick up in state spending in the second half of the year

| +1.4% |

Russian May retail trade, YoY+1.7% YoY for 5M19 |

| Better than expected | |

Household income and consumption better than expected, but we're still not too optimistic

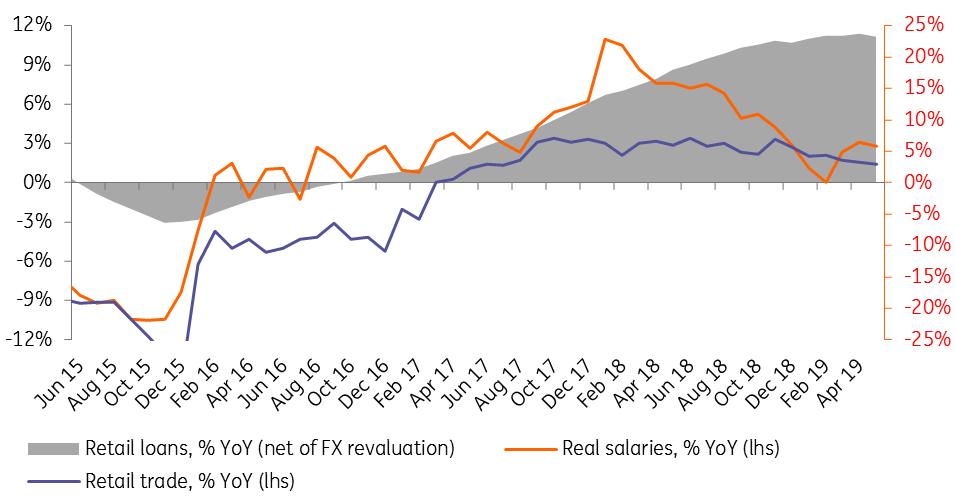

The May Russian retail trade growth of 1.4% YoY and a real salary increase of 2.8% YoY are both better than expected. Combined with an upward revision of April data by 0.4 pp and 1.5 pp respectively it may appear as a positive sign. However, we remain cautious for several reasons:

- The spike in real salaries to 2-3% YoY in April-May vs. 0-2% YoY growth in 1Q19 (amid relatively stable CPI growth at c.5% YoY) seems to be driven by the oil extraction and financial sectors (they account for 4.6% of those employed), which may reflect annual bonus payments or other sector-specific factors;

- For the broader population, retail lending growth seems to be the primary source of financing consumption, however it started decelerating from May, and the publicly expressed concerns with the pace of consumer lending growth by the Bank of Russia (CBR) and the president suggest little room for further support to consumption from lending in the medium-term;

- The structure of retail trade suggests continued deceleration of growth in the sales of non-food items from 2-3% YoY in 1Q19 to 1-2% YoY in April-May, possibly reflecting the continuing effect of a VAT hike amid income growth concerns;

- Today's comments by the president during the annual call-in session with the general public suggests, in our view, that the government is not looking to adress the issue of income and poverty with additional social spending but would rather aim at higher labour efficiency. This message is positive for the macro stability framework, but suggests that any fast and easy support to household income is unlikely.

Overall, with a lack of obvious income drivers, likely deceleration in retail lending and limited scope for deceleration in inflation from the current levels, we continue to expect subdued consumption growth this year.

Key indicators of the Russian consumer trend

Corporate activity weak, but may recover in 2H19 thanks to budget seasonality

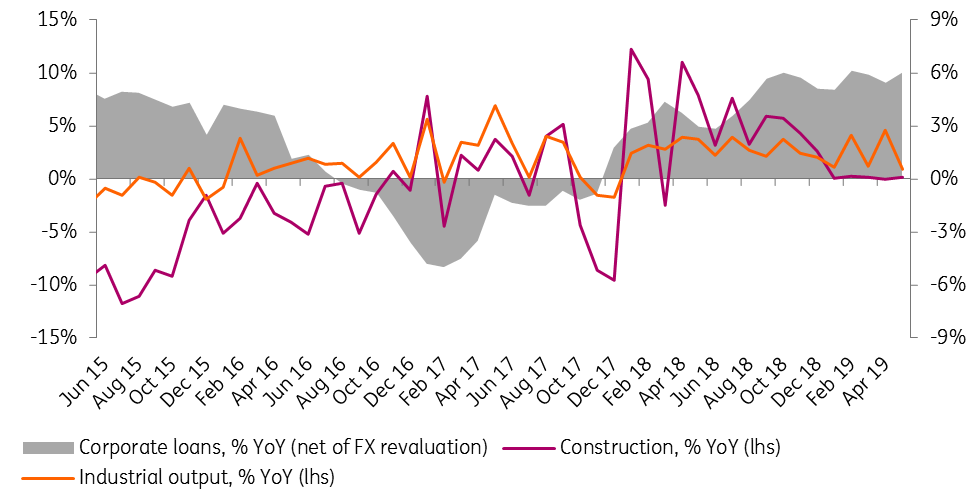

The virtually nonexistent 0.2% YoY growth in construction in May, combined with the 0.9% YoY increase in industrial production (we commented on it earlier this week) and lack of any noticeable acceleration in corporate lending - suggest there's little recovery in the corporate sector from its stasis mode. However, we reiterate there is a hope for some recovery in 1H19, as state spending on direct support to the economy is scheduled to accelerate from -19% YoY in 1Q19 to the drafted +16% YoY for the full year, as the 'National Projects', which are 70% capex, gain traction, and overall budget spending accelerates from 6% YoY in 1Q19 to the 13% YoY drafted for the full-year.

As for the longer-term debate on whether to allow investing part of NWF, the sovereign wealth fund, into the local projects from 2020, the president's position in the debate between Minfin (in favour) and the CBR (concerned) has yet to be clarified. Today's call-in session on the one hand started with highlighting the importance of the National Projects (we believe the idea to invest part of NWF into the local projects is at least partly linked to the search of sources to finance the massive RUB26 trln programme), but on the other hand there were no clear signs that the president is comfortable with sacrificing the conservative approach to the budget policy.

Key indicators of the Russian producer trend

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more