- Quick take

- 13 July 2021

- Russia

Russia: Corporate foreign debt steady, but equity keeps leaking

Russian corporate foreign debt remained relatively flat in 2Q21, suggesting the likely neutrality of the upcoming US$33bn gross redemption in 2H21 for the FX market. But this also means that the entire US$10bn net private capital outflow seen in 2Q21 was related to equity flows, which is not a good sign in terms of the local investment trend

Bank of Russia released its estimate of the foreign debt as of mid-year 2021, providing more details on the overall balance of payments data we covered earlier. The numbers do not contradict our general take, but the surprising part was that foreign debt dynamics did not play much of a part in the capital outflow seen last quarter, suggesting that the structural weakness of the capital account remains unchanged. We have the following observations:

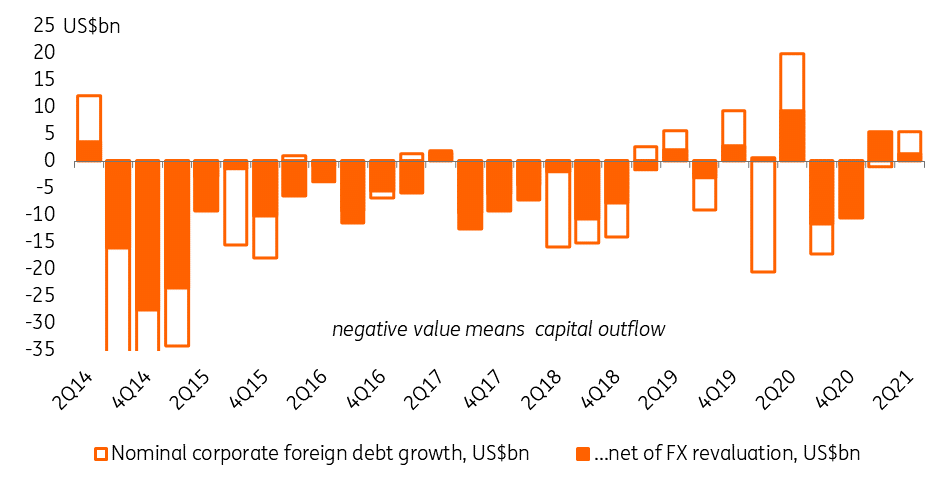

- Nominal foreign debt of banks and non-financial companies (corporate foreign debt) increased by US$6bn to US$394bn in 2Q21 (c.25% of GDP). To remind, up to 45% of the corporate debt is denominated in EUR and RUB, so in order to arrive at the actual quarterly foreign debt dynamic the headline US$-denominated number should be adjusted for the appreciation of those currencies to USD by 3% and 1% respectively during 2Q21. As a result, we estimate that the Russian corporate foreign debt increased by US$1bn in 2Q21, effectively stabilising after showing US$6bn growth in 1Q21 and a US$12bn drop in 2020 (Figure 1).

- On the positive side, the flat foreign debt performance (and small growth in 1H21) after net redemptions in 2020 point at a stabilisation of the corporate sector mood and relatively calm reaction to the increased volatility of the global debt market and to the negative foreign policy newsflow. After the initial sanction-driven shock in 2014, the Russian corporate foreign debt stabilised by 2019, followed by the Covid-related risk-off in 2020, which now seems to be over. This suggests that the upcoming redemption of US$33bn worth of corporate foreign debt scheduled for 2H21 will most likely be refinanced and be neutral for the local FX market.

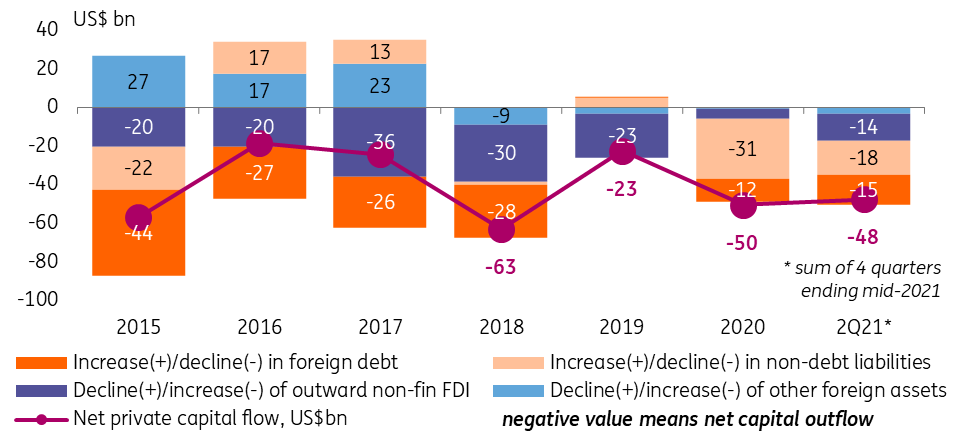

- On the negative side however, the stable foreign debt is failing to prevent net private capital outflows, which totaled US$10bn in 2Q21 and US$48bn over the last 4 quarters, virtually unchanged vs. US$50bn seen in 2020. Looking at the structure of the outflow, it appears that around 80% of it in 2Q21 was assured by the reduction in the non-debt foreign liabilities of the corporate sector, while the remaining 20% were the result of purchases of foreign assets, predominantly by the non-financial corporate sector. This equity-heavy structure suggests an outflow of equity investments, which could be related to activities of offshore shareholders, potentially limiting the local capacity for CAPEX and structural demand for the ruble in the longer term.

- Relative to the crisis in 2020, the structure of the capital outflow managed to become a bit more balanced, as the contribution of foreign debt redemption increased from 24% in 2020 to 32% over the 4 quarters ending in mid-2021. However, that structure still remains equity-heavy (Figure 2), suggesting that the appetite for outward FDI and portfolio investments remains high despite the current efforts to de-offshorize the economy. It also puts additional focus on the nature of the recent acceleration in the local bank lending to non-financial corporates to 7-year high of 13% YoY as of May 2021 (net of FX revaluation) – we suspect the latter is more likely to reflect working capital and other short-term financial needs rather than long-term investments.

Figure 1: Russian companies and banks increased foreign debt by US$1bn in 2Q21 and US$7bn in 1H21 after a US$12bn drop in 2020

Figure 2: In the recent 4 quarters, the role of foreign debt redemption in overall capital outflow has increased but remains small

Foreign debt performance supports our benign RUB view for 2H21, but highlights structural challenges

Stabilisation of the foreign debt despite global market volatility and foreign policy pressures is supportive of our constructive RUB view in 2H21. The latter could also benefit from the conservative monetary and fiscal stance (with a higher-than-expected RUB0.6tr budget surplus reported for 1H21 on strong non-fuel revenue collection). Meanwhile, the equity-heavy structure of the overall capital outflow from Russia is confirming the longer-term structural challenges to the local balance of payments, which needs to be addressed not so much by prudent macro management, but rather through structural incentives to local investment demand.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more