- Quick take

- 12 October 2018

- Romania

Romania: 3Q data disappoints but outlook brightens

After a sharp slowdown in retail sales, industrial production points to a sequential contraction for the sector in the third quarter

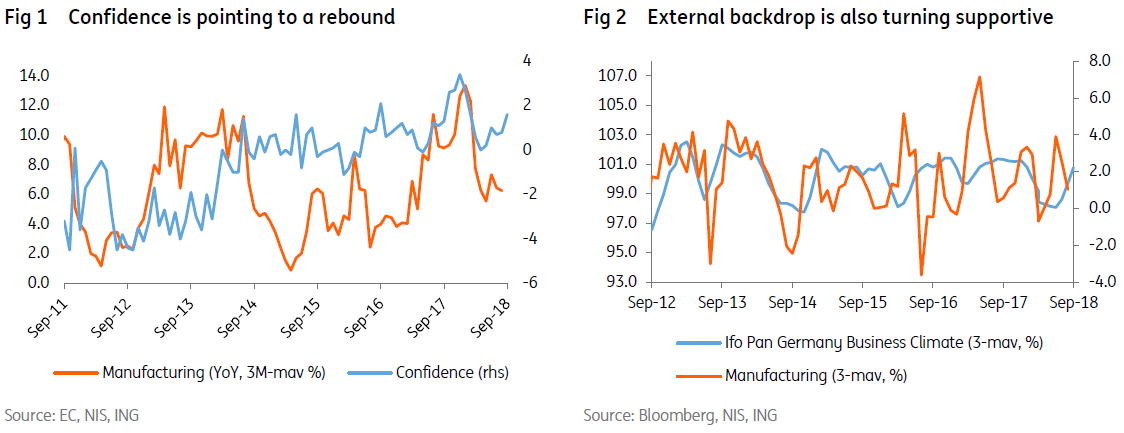

Weak manufacturing, outlook seen improving

Industrial production decelerated to 3.9% year-on-year in August from an upwardly revised 5.4% in July. The slowdown was less pronounced for manufacturing but still fell to 4.5% YoY from 5.1%. Nevertheless, most soft data is pointing to a rebound in manufacturing supported by stronger order books as export demand is improving.

Implications for NBR policy: food for doves

High-frequency data for the third quarter came in mostly on the weaker side. Hence, despite most of the supply shocks mentioned by “some Board members” in the NBR minutes as a risk for “de-anchoring inflation expectations”, we expect it to stay on hold at the 6 November meeting citing stable core inflation, a weaker growth backdrop and the need to assess previous tightening.

Nevertheless, the chances for a hike are on the rise, as the central bank is likely to revise its year-end inflation forecast closer to our 3.9% YoY forecast (details here) from 3.5% due to higher oil and volatile food prices. High FX pass-through makes the NBR sensitive to a weaker Romanian leu as long as inflation is way above its target band. Still, from a net creditor position, the central bank would likely resort to liquidity management to prop-up the leu if needed. In fact, the minutes of the last meeting noted that “the continued relative stability of the EUR/RON exchange rate over the recent months” is “most likely attributable to the considerable differential of interest rates on the local market versus those prevailing in Europe and regionally.” We have the next rate hike pencilled in for 1Q19, as year-end budget spending to reach the budget deficit target is expected to shift the liquidity position of the banking system into a surplus, limiting the NBR's flexibility. This is likely to be followed by two more hikes in 2019 as “most Board members reiterated the importance of an adequate dosage and pace of adjustment of the monetary policy stance”.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more