- Quick take

Romania: Upside surprise from GDP growth, again…

- 14 August 2019

- Romania

Flash estimate 2Q19 GDP posted a 1.0% sequential advance, translating into 4.4% YoY growth. Given the surprise, growth could come 0.5ppt higher. So we'll wait for the breakdown and more detail on external demand before updating our 3.5% growth forecast for 2019

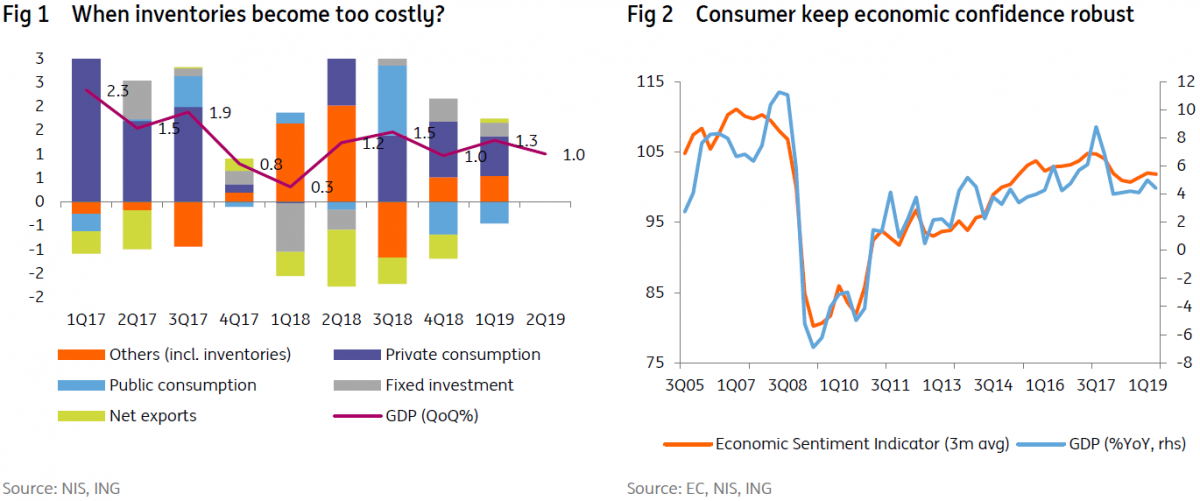

Flash estimate 2Q19 GDP posted a 1.0% sequential advance, a slight deceleration from 1.2% in 1Q19, but above the ING/Bloomberg median estimates of 0.5%/0.6%. This translates into a 4.4% year-on-year GDP expansion.

The breakdown of GDP data is due on 6 September, but from the demand side, we could see, in sequential terms:

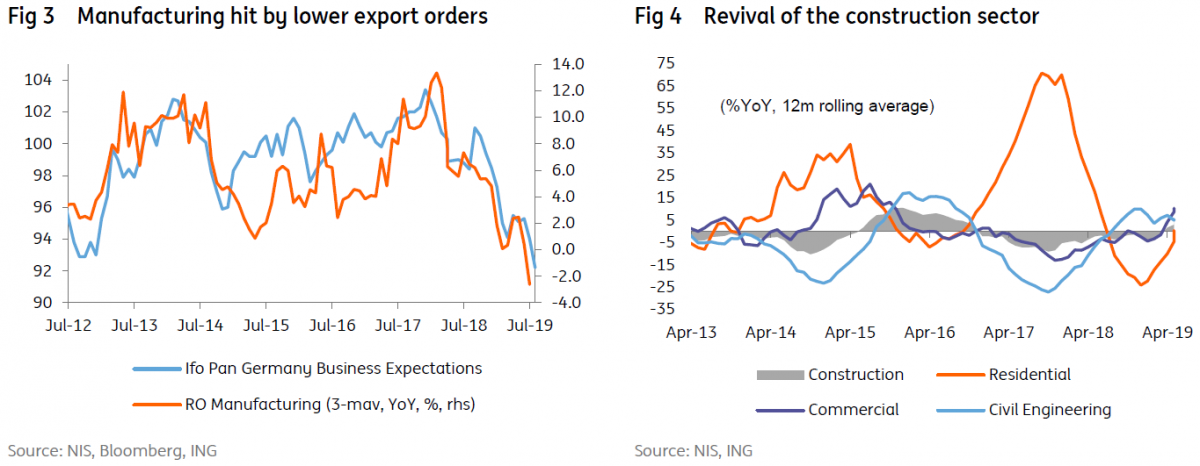

- Private consumption is flat (or slightly positive), as suggested by retail sales data, though consumer confidence reached the highest level since 3Q17. Still, consumption very likely remained the main contributor to growth.

- Investment (driven by construction, though with relatively low weight in GDP) could offer a slightly positive surprise

- Public consumption is likely to add up to growth given the big fiscal impulse (1.4ppt of GDP) in 2Q alone, though usually, its growth multiplier is pretty low

- The narrower negative contribution from net exports

- But again, the big surprise could come from inventories on the back of agriculture crop season

Supply-side, versus the previous quarter, detail GDP data could reveal:

- Contraction for the industry sector. In fact, data shows the industry contracted by -0.5% QoQ. This was driven by contraction in the manufacturing sector of -1.1% QoQ in 2Q19, after posting a -5.3% YoY decline in June

- Data released today showed the construction sector expanded by 15.3% QoQ in the second quarter, a mild slowdown from 18.3% sequential jump in 1Q19. This is mainly driven by sectorial government facilities for the sector enacted at the start of the year

- Moderate expansion in services, but the sector likely remained the main contributor to the sequential growth

- Another strong print from agriculture

Given the upside surprise versus our forecast and past data revisions, all things being equal, GDP growth for the whole year could come 0.5ppt higher, but we are waiting for GDP breakdown and more detail on external demand before updating our 3.5% growth forecast for 2019.

| 4.4% |

2Q19 GDP growthBreakdown due 6 September |

| Higher than expected | |

The lagged effects from eurozone slowdown are already visible in the trade sector. Agriculture and construction are now more like green shoots rather than pillars of growth. With no fiscal headroom and structural reforms, which could unleash some growth potential are not on the agenda in election years. So, the risk is that the economy could slow down more significantly in the quarters ahead.

Even though the reaction to the growth slowdown from major central banks is likely to buy some time for fiscal consolidation and reforms, elections are likely to waste the momentum. At the same time, there is not much room for the central bank to ease policy unless it is accompanied by fiscal consolidation.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more