- Quick take

- 5 August 2020

- Romania

At mid-year, Romanian retail sales suggest a flatter V

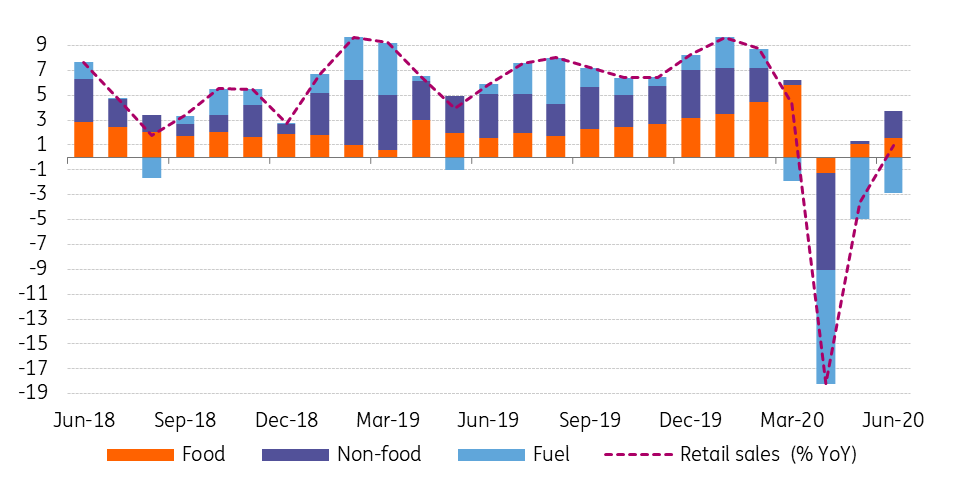

At 1H20, Romanian retail sales are 0.3% above the same period in 2019. The second quarter has nevertheless contracted by 6.9% versus 2Q19. Food and non-food items are back to pre-crisis levels in June but fuel sales remain noticeably below

The worst quarter of the past decade has now passed and the data that describes it is beginning to unveil.

With June retail sales now out, we can say that overall it wasn’t as bad as feared, but not that great either. Compared with the previous quarter retail sales contracted by 13.4%, which will probably act as a drag on second quarter GDP growth.

There are a few reasons for optimism given that growth in June was mainly driven by non-food items, which expanded by 6.4% versus June 2019, although on the quarter non-food still contracted by 9.5%. The last-minute acceleration seen in June was particularly strong in items such as clothing and DIY articles (eg, furniture, electrical equipment, lighting devices, etc), suggesting that consumers are not overly worried about the long term prospects.

Fuel sales, on the other hand, contracted by almost 28% in the second quarter and a recovery to pre-crisis levels seems a longer term process.

Retail sales (YoY%) and contributions

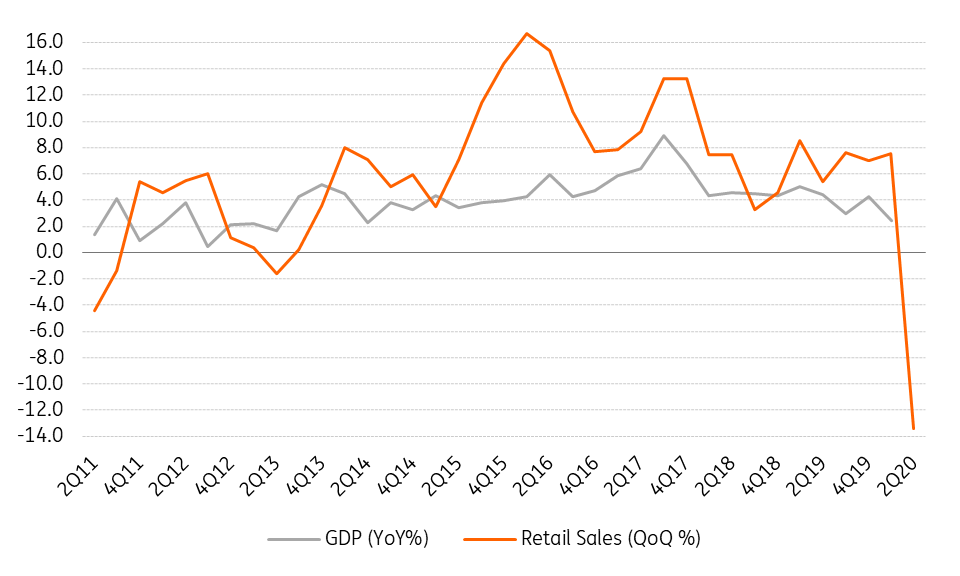

Today’s numbers paint a slightly more optimistic picture of what we can expect from next week’s 2Q20 flash GDP. There is still some important data to be released before that (industrial output, trade balance, current account, etc) that will complete the second quarter puzzle, but so far it looks as though the flash GDP on 14 August has a good chance of being better than our initially pencilled contraction of 18%, at maybe around 14%.

On the negative side, however, we feel that a better-than-expected second quarter will just lead to a flatter 'V'-shaped growth this year, meaning that the subsequent recovery from the third and fourth quarters will be less pronounced. Reasons to believe that come from the pandemic evolution, which has intensified in the third quarter, the electoral context that will dampen sentiment to some extent as it blurs policy visibility, and the general flattening of most confidence surveys in July.

Retail sales and GDP (QoQ%)

Unless we will have a shockingly positive surprise from second quarter GDP numbers, we are still comfortable with our forecast for a 5.5% contraction for the full year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more