- Quick take

- 25 February 2019

- Romania

Romania: Lending off to a good start in 2019

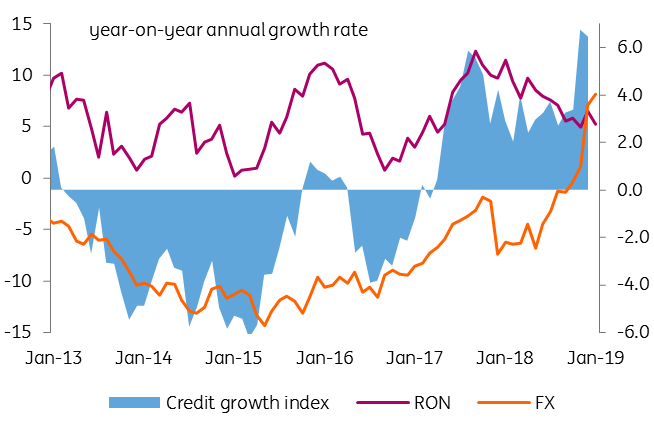

Adjusted for FX effect, credit growth expanded 8.1% year-on-year in January 2019, thus keeping alive hopes that the economic slowdown will not turn into a hard landing

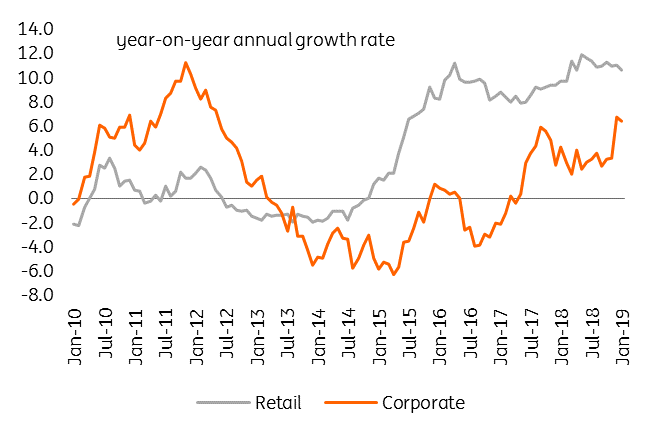

Retail credit still strong

Despite the recently enacted macroprudential measures aimed at capping the debt service for retail borrowers, the retail lending dynamics remained robust in January. Consumer loans growth in local currency accelerated for the eleventh consecutive month to 20.4% year-on-year while RON mortgage loans continue their mild descent in the growth rate to 32.7% in January. It is actually the twelfth consecutive month of deceleration in the mortgage growth rate but the dynamics still looks reasonable given the context of slower growth.

Credit growth index (adjusted for FX effect)

FX lending becoming attractive again for corporates

After a 2018 with ultra-low volatility for the exchange rate and increase in borrowing costs in local currency over the last two years, corporates attention gradually turned towards hard currency. December 2018 marked the first month since 2011 when FX lending to non-financial institutions dynamic has been superior to the RON one. January 2019 came to confirm the trend, as loans in hard currency expanded by 8.2% year-on-year, while the local currency ones slowed to 5.2%, from 6.5% in December 2018.

Corporate lending dynamics

Highly uncertain outlook

Given the rather accelerated slowdown of the Romanian economy, from 6.9% in 2017 to 4.1% in 2018 and to 2.7% in 2019 (ING forecast), the resilience of lending activity provides a much-needed ray of hope that the slowdown will not eventually turn into a contraction. Still, the revival in bank lending might be derailed by the bank levy as banks are likely to try to optimise their asset base and pass-through part of the additional cost.

The NBR has requested the elimination of the link between the bank tax and the interbank ROBOR index while also suggesting to exempt from the tax base the minimum reserve requirements, government bond holdings and loan portfolio originated under the state guaranteed mortgage program. Discussions with the government to amend the bank levy bill however ended in an apparent deadlock. Eventually, the parliament could amend the bill, but this might take quite some time. In the meantime, the government emergency decree remains the enforceable legislation.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more