- Quick take

- 10 October 2018

Romania: CPI surprises as spud prices surge

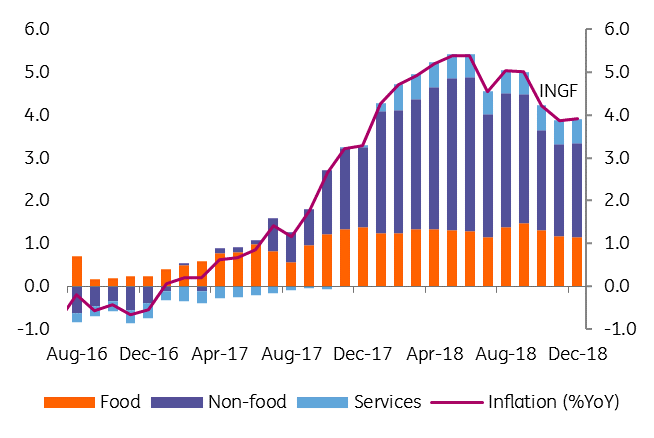

Inflation declined less than 0.1 percentage point to 5.0% year-on-year in September compared to estimates of 4.7%, 4.8% and 4.9% from ING, the market consensus and the Romanian central bank, respectively. Our forecast error came entirely from volatile food prices. Core inflation was flat at 2.8%, in line with our expectations

Large base effect coming in October

CPI surprise: supply side factors

Food CPI inched up by 0.2 percentage points in September to 4.4% year-on-year, with fresh vegetables a strong driver. Actually, almost half of our forecast error for September came from one item in the consumer basket – potatoes - which jumped by 19.2% month-on-month.

Non-food prices fell 0.2ppt to 6.6% YoY, as higher oil prices were more than offset by the statistical base effect, as the first step in an excise duty hike from last year dropped out of the base. The base effect is even larger in October as the second step of this hike and the increase in regulated electricity prices from last year drop out of the base, likely leading to a c.0.8ppt drop in headline inflation.

Services CPI was down 0.1ppt to 2.5%, but this still suggests relatively strong price pressures coming from domestic demand.

| 5.0% |

YoY September CPIOn volatile food items |

| Higher than expected | |

Core inflation tamed, for now

Implications for NBR policy: still waiting for more details

Given the surprise to our forecast, ceteris paribus, our year-end inflation projection is pushed up by 0.3ppt to 3.9% YoY. The surprise for the National Bank of Romania was less significant, but the recent oil price increase might lead it to revise upwards its year-end inflation estimate in the November Inflation Report. Moreover, core inflation declined further, though within the rounding margin, with CORE3 staying flat at 2.8% YoY.

3Q18 high frequency data came in rather mixed: better consumer sentiment, but weaker retail sales, improving manufacturing morale but softer production figures. Flash 3Q18 GDP is due for release after the last NBR meeting for this year. Hence, we expect the central bank to cite supply-side inflationary shocks and the need to assess previous tightening. We think it will keep its policy stance unchanged on 6 November. Macro-prudential measures to limit the leverage for individual borrowers, which are due to be presented by the NBR, are also likely to be cited as an alternative and more efficient policy tightening tool. A possible intensification of the Romanian leu's depreciation might increase the chances for a rate hike, though liquidity management could be enough to fend it off.

We still have pencilled in three NBR rate hikes of 25 basis points each for the NBR next year, with the key rate reaching 3.25%, but we could also see the gap between the key rate and market rates narrowing and a somewhat weaker leu.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more