- Quick take

- 30 October 2019

- Romania

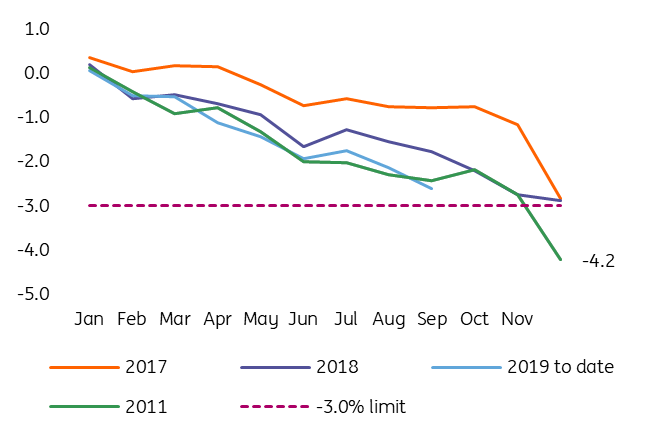

Romania: Budget deficit likely to exceed the 3.0% threshold

At -2.62% of GDP in September, keeping the full-year deficit below 3.0% of GDP in 2019 looks almost an impossible task for any government

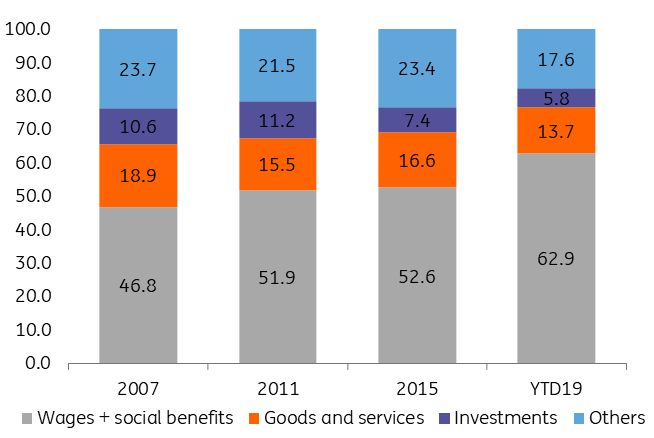

The pace of public finances deterioration seems to have precipitated in the second part of the year, as the budget deficit reached levels unseen since 2010. Moreover, the hard data doesn’t necessarily indicate some newly enacted measures behind the deficit boom (eg, pensions with a 15% hike in September), but rather a continuation of the accentuated revenues/expenses dynamics divergence. While revenues are up by 11.6%, the expenditure side looks increasingly difficult to control: +15.3% on the year, driven by the same ballooning wage bill (+20.1%) and social benefits (+11.1%), despite capital expenditures only at 1.4 percentage points of GDP.

Budget balance as % of GDP

Expenditure composition

The -2.62% budget deficit in September makes the government's full-year target of -2.76% look quite unrealistic. We have been maintaining our forecast for -3.0% of GDP at the year-end for quite a while, based on the government’s strong commitment to this threshold, as exhibited in previous years. This looks less of a case this year, as the current interim government might have less incentive/power to keep the deficit in check, while a new government will not have much time to patch the budget. That said, we are revising our year-end budget deficit forecast to -3.4% of GDP for this year.

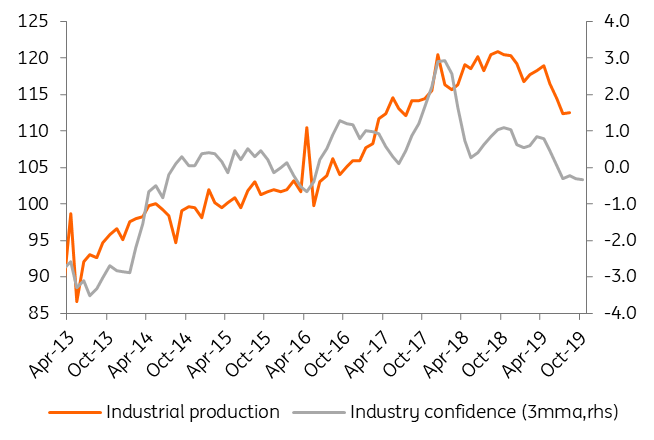

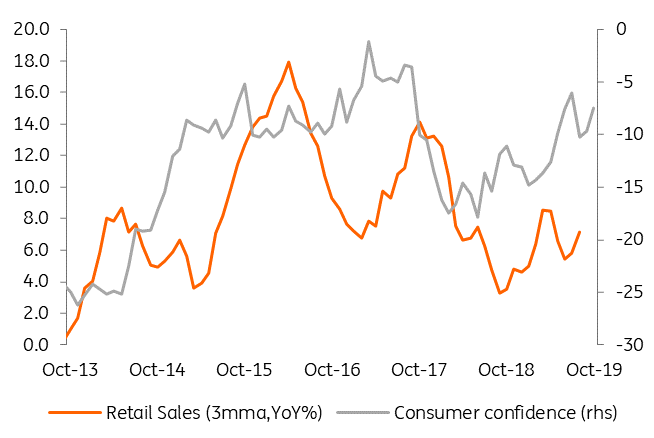

What used to save the day in previous years was strong nominal GDP growth, which managed to offset much of the fiscal slippages and tight spending control in the last part of the year. So far, the economy has been holding up relatively well, but signs of fatigue are showing up lately. The industry is already in contractionary mood, with the latest confidence indicators pointing towards a prolonged weak stance. However, the consumer mood remains optimistic, even close to historical highs, which should keep things moving within the economy. The electoral context is likely to maintain the double-digit wage advances intact at least in the public sector, hence not much could go wrong for the consumers in the short term.

Industry contracting, confidence drops

Consumer confidence keeps things moving

Summing up, the deterioration trend of public finances continues, and we now expect that this year the budget deficit will exceed the 3.0% of GDP threshold. This overlaps an overall slowdown of the economy which, while not alarming, will put some additional pressure on the already strained public finances through the revenue channel. We forecast a -3.7% of GDP budget deficit for the next year, as we believe that the 40% pension hike will only partially be compensated by offsetting measures given the electoral context.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more