Reserve Bank of Australia drops its tightening bias

The Reserve Bank of Australia (RBA) is still not ruling out hikes, but it has moved to a more neutral setting as far as its guidance is concerned

What has changed?

The RBA met today to discuss policy, but there was no expectation of any rate change today, and the entire focus of the market was on the RBA's statement and guidance.

The sum-total of what markets are reacting to today amounts to eleven words, these are "...and a further increase in interest rates cannot be ruled out". These eleven words were in the February RBA statement. but were replaced in the March statement by "...and the Board is not ruling anything in or out".

In central-bank-speak, this means that the RBA is signalling that it has a neutral outlook on rates, whereas before, it had a tightening bias.

This isn't much of a change and such a tweak to the statement looked quite likely following the recent run of data, which has included confirmation that the economy is slowing according to recent GDP data, as well as some softer labour market data. The inflation outlook has also improved considerably, with the big drop in inflation in December not reversing as was widely expected in January, though the February data point looks likely to show some back-slippage, which is maybe why the RBA is keeping its options open for now, rather than moving straight to an outright easing bias.

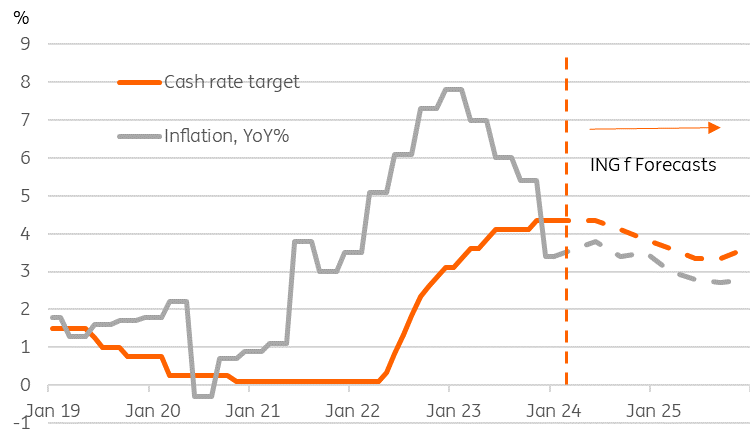

Cash rates and inflation forecasts

Markets have moved a bit but this was not totally unexpected

The impulse response to this development was for the AUD to weaken slightly, though it remains above 65 cents against the USD, and the market moves have, so far, been quite modest.

Cash rate futures are now more fully pricing in two cuts before the end of this year, whereas before, the second cut was only about 61% priced in. Markets are still not totally convinced about the second cut though.

Australian government bond yields have declined along the curve. 2Y yields are down about 6 basis points, while the 10Y bond yield has declined by about 5bp relative to its pre-RBA decision yield and is now down to 4.08%

Two cuts this year seems a reasonable guess

Although the near-term inflation path still presents a slight risk to the rate outlook, we think that inflation will have fallen sufficiently far by the third quarter of this year to enable the RBA to cut the cash rate target by 25bp. We also think that by the year-end, slowing growth and further inflation declines will be enough to deliver a second rate cut. Where this leaves bond yields and the AUD will probably be more influenced by the US and Fed rate policy than local developments, and there are still huge question marks hanging over that.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap