- Quick take

Rates unchanged in New Zealand

- 11 November 2020

- New Zealand

New Zealand's central bank delivers a mixed message while leaving rates unchanged and introducing a new funding-for-lending program

| 0.25% |

Official cash rateUnchanged |

| As expected | |

No change in rates

The Reserve Bank of New Zealand (RBNZ) did not cut rates as we suggested last week might happen, following the recent 3Q20 spike up in the unemployment rate, and the 15bp cut administered by their central bank neighbours in Australia.

But where we go from here is considerably less clear.

On the one hand, you could argue that the new $100bn funding-for-lending (FFL) program will circumvent the issues of housing-market overheating that further rate cuts might deliver. But there are problems with this. Unless the RBNZ can ensure that this lending predominantly supports businesses, it is often easier for cheap funding to simply fuel more mortgage lending, which has been the experience of a lot of other countries that have gone down this FFL route.

Likewise, the RBNZ's quantitative easing measures have also got it to the point where it now owns more than a third (37%) of all the outstanding stock of government bonds, with little further room to move. Such policies also tend to just drive down market and retail rates more generally, so any problems (such as overheating property) associated with easing policy rates further are shared by the current QE scheme.

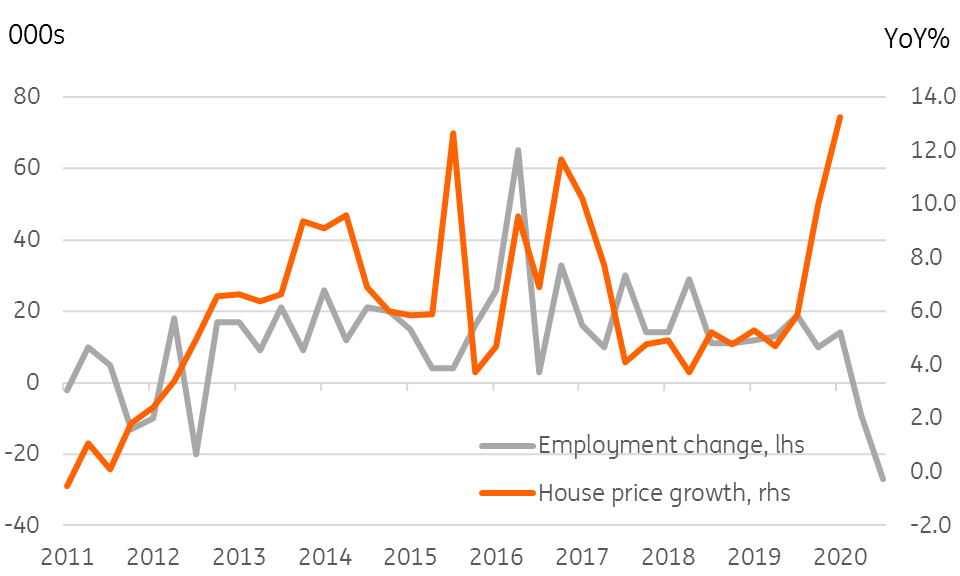

House prices and employment change in New Zealand

Then there is the inconsistency between the RBNZ noting that the economy has actually been stronger than anticipated, but painting a downbeat picture of the quarters ahead, saying they won't be tightening policy any time soon, and noting they are making progress on being able to deliver a negative cash rate. It's very hard to reconcile today's rate pause (if it is just a pause) with the economic realities and keep a credible view open for negative rates in the not too distant future.

One interpretation of all this, and the one we are leaning towards, is that the RBNZ is playing a complicated game of expectations management, though one that trips over some existing economic realities. So the RBNZ is keen to keep expectations alive to the prospects of further easing and to dim the prospects of future tightening in order to keep rate expectations low, and thereby longer-term market rates and yields low.

But this is also pushing the housing market into overheating while the economy as a whole seems to be in decent shape. All things considered, New Zealand probably doesn't need any further monetary stimulus and is running out of effective channels through which to implement this if it doesn't want to create further distortions.

So if that is the case, despite all the talk to the contrary, then the RBNZ is probably done with easing, unless the economy does deliver a double-dip. As the same is almost certainly also true for the RBA, then both the NZDUSD and AUDUSD are likely to be dominated by anticipated USD weakness rather than local monetary policy actions over the coming months. We anticipate the NZD remaining close to 0.68 by the year-end, before rising to 0.70 in 1Q20.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 12 November 2020

- This bundle contains 3 Articles