- Quick take

Price pressures increase further in Hungary

- 8 October 2021

- Hungary

After a surprise in August, the market adjusted its inflation expectations higher, so the 5.5% year-on-year rate in September was in line with estimates. However, the central bank’s forecast seems to be outdated already, and stronger tightening may be needed

| 5.5% |

Headline inflation (YoY)ING forecast 5.5% / Previous 4.9% |

| As expected | |

Inflation strengthens in every aspect

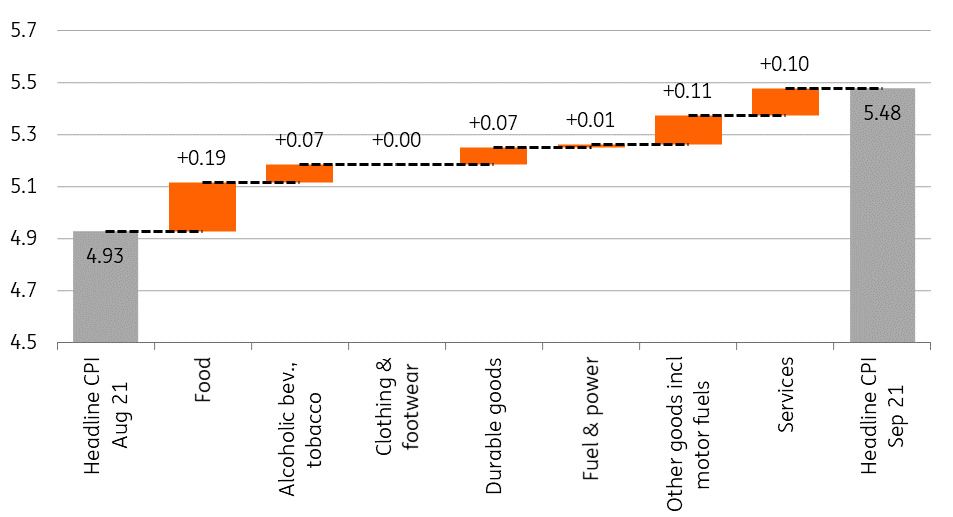

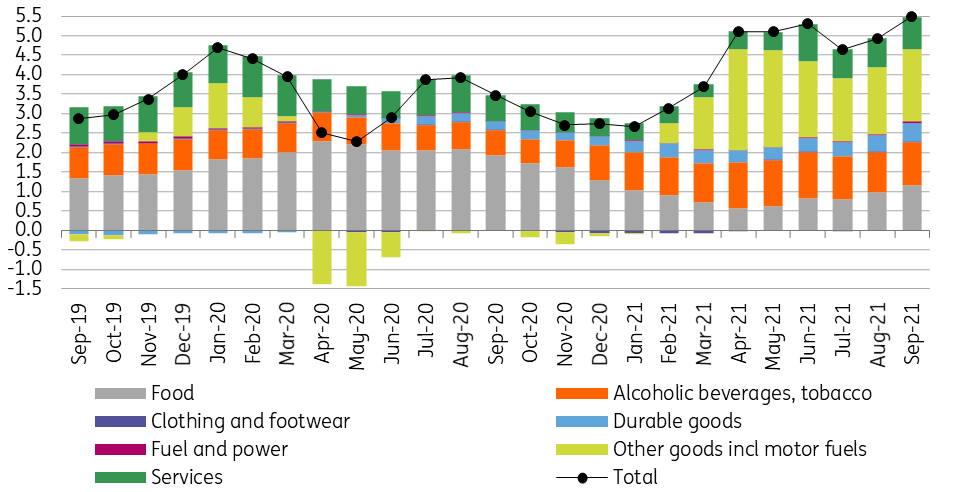

Inflation picked up in August and the acceleration continued in September. This didn't come as a surprise, however, as the market had adjusted inflation expectations upwards following the surprising August data. So the 5.5% YoY headline inflation was in line with the market projection and matched ING’s forecast. The base effect is significant as the month-on-month inflation rate was a moderate 0.2%. The 0.6ppt increase in headline inflation compared to August was broad-based, as all of the major groups showed stagnation or acceleration.

Main drivers of the change in headline CPI (%)

The details

- Inflation in food came in at 4.4% YoY in September, a significant acceleration compared to August. This move was fuelled by seasonal factors such as the increase in the price of vegetables. On the other hand, agricultural commodity price increases are also spilling over into oils and fats (18.6% YoY).

- Prices of durable consumer goods increased further. On a monthly basis the 0.9% rise translated into a 5.1% YoY reading. The last time durables inflation was above 5% was back in 2009. The rise in industrial producer prices and transport costs, as well as the fact that the forint is struggling to strengthen despite the cycle of interest rate hikes, are having an upward impact on imported inflation.

- When it comes to fuel, the base effect didn’t help to alleviate the inflation pressure. Although monthly inflation was only 0.4%, the yearly price change remained elevated at 21.6%. September has traditionally seen some easing in clothing inflation but this year was different, with inflation remaining at 0.5% YoY.

- Inflation in services also picked up, which again goes against seasonal patterns. The 3.2% YoY inflation was fuelled by the repair and maintenance of dwellings (13.5% YoY and the repair and maintenance of vehicles (8.3% YoY). One of the sectors most hit by Covid also saw prices increasing at an elevated level to make up for losses in the past 18 months: cultural, educational and entertainment services prices rose by 3.9% over the year.

The composition of headline inflation (ppt)

Underlying price pressures increases

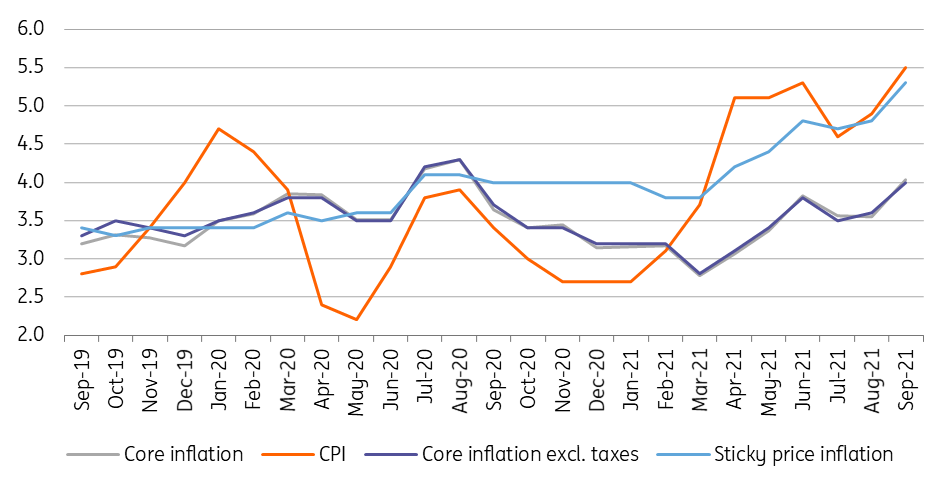

In all, we have broad-based inflation pressure, which is coming both from core and non-core elements. So it hardly comes as a surprise that core inflation rose by 0.4ppt to 4.0% YoY in September. Underlying price pressures have increased further, which is also reflected in the National Bank of Hungary's underlying indicators. Core inflation, excluding indirect tax, sits at 4.0% YoY, while the so-called 'sticky' price inflation moved up to 5.3% YoY, moving close to the all-time high reached in 2004.

Headline and core inflation measures (% YoY)

The chance for stronger rate hikes increases

The September inflation reading was in line with the market consensus, but it is higher than the NBH's forecast published in September (5.5% vs 5.2-5.3%). As a result, we see an increased risk that inflation over 2021-2022 will be higher than outlined in the September Inflation Report. This would also mean further delays in reaching the inflation target without changing the central bank’s underlying rate hike path. According to the latest official communication, the rate hike cycle will continue in the next couple of months with 15bp steps. However, today’s data may force the NBH to change tempo again, this time increasing it. A stronger rate hike might be needed to anchor inflation expectations and to avoid second-round effects. Such a decision could also help the forint, which is still unable to deviate significantly from the 360 level versus the euro.

ING's inflation outlook unchanged

As for ING's inflation forecast, as the incoming data was in line with our expectations, our forecast remains unchanged at 4.7% YoY in 2021 and we see next year’s inflation at 3.7% YoY on average.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more