- Quick take

- 23 February

- Poland

Polish retail weathered the winter storm

Declines in January construction production and output made some analysts worry that Poland's retail sector had also been hit by the harsh winter weather. However, retail sales proved more resilient than expected, as consumers refreshed their wardrobes and demand for durable goods remained solid

Poland’s retail sales increased by 4.4%YoY in January (ING: 3.1%; consensus: 3.3%) after an increase of 5.3%YoY in December, surprising to the upside.

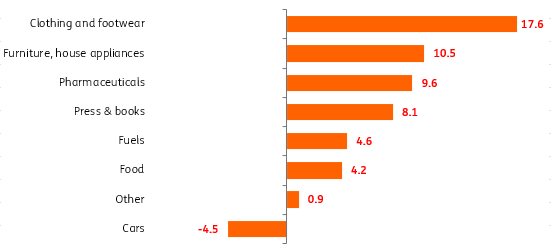

The biggest increase in sales was reported in textiles, clothing and footwear (17.6%YoY).

After several mild winters in recent years, January 2026 caught many Poles by surprise with freezing temperatures and heavy snowfall, prompting them to update their wardrobes with clothing more suitable for colder conditions.

Sales of furniture, electronic equipment and household appliances maintained double-digit growth (10.5%YoY), confirming continued robust demand for durable goods. The decline in car sales (-4.5%YoY) was not a surprise given changes in some legal and administrative regulations. Since the beginning of 2026, businesses have had less generous limits for combustion car depreciation and leasing cost deduction from the tax base. For households, the budget of subsidies for purchases of electric vehicles (“NaszEauto”) was also depleted.

In the case of essentials, we also saw a surprisingly robust sales dynamic. Fuel sales increased by 4.6%YoY, however the pace of growth was slightly lower than in December last year (8.3%YoY), despite the low prices of fuels. Meanwhile, the strong increase in food sales (4.2%YoY vs. 1.9%YoY in December) might have been linked to stockpiling in order to avoid frequent shopping trips, given icy and snow‑covered pavements.

The full set of January data from the real economy points to some slowdown in economic activity at the start of 1Q26, and weather conditions throughout most of February were also difficult. Some of the losses from the first two months may be recovered in March; however, GDP growth in the first quarter is likely to be slower than the 4.0%YoY posted in 4Q25. On the positive side, consumption growth remains sustained.

Our cautious full‑year GDP growth forecast of 3.7% remains unchanged.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more