- Quick take

- 22 October 2025

- Poland

Strong September boosts Polish GDP growth outlook

Although September retail sales growth fell short of expectations due to weak food sales, the sector still performed strongly thanks to robust durable goods demand. When combined with solid industrial production and construction data, along with anticipated strength in services, this supports our projection of 4%YoY growth for 3Q25

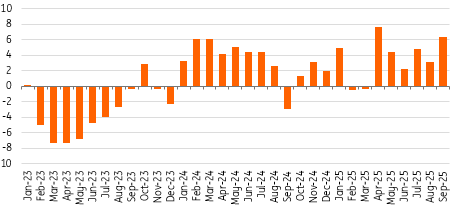

Retail sales of goods rose by 6.4% year-on-year in September (ING: 8.0%; consensus: 6.8%) following a 3.1% YoY increase in August. The strong annual growth was supported by a low base from September last year, when the southern part of the country was dealing with the aftermath of flooding, and retail sales contracted by 5.7% month-on-month. However, the scale of improvement this September was below our expectations. Seasonally adjusted data indicate a 0.6% month-on-month decline in sales.

Low base from last year contributed to high retail sales growth in September 2025

Retail sales (real), %YoY (NSA)

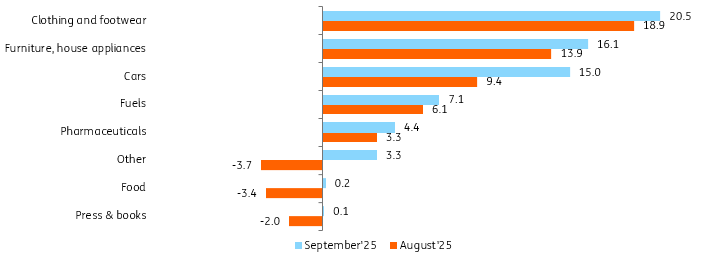

The main source of the lower-than-expected growth in sales was food, which saw an increase of just 0.2% YoY. Double-digit growth was reported in textiles, clothing and footwear (20.5% YoY), furniture, consumer electronics and household appliances (16.6% YoY), as well as cars, motorcycles and parts (15.0% YoY). This reflects not only the low base from last year, but also a continuation of the trend observed in previous months.

The September data set from the real economy – comprising industrial production, construction and assembly output, and retail sales – paints a solid picture of the end of that third quarter. The results were broadly in line with consensus (retail sales) or better (industrial and construction output). We maintain our forecast for GDP growth in 3Q25 at 4.0% YoY, and for the full year, we expect economic growth to be around 3.5%.

The main drivers remain the services sector and rapidly expanding consumption, which is set to grow faster this year than in 2024, despite a slower increase in the real disposable household income. Consumer sentiment is improving, and households appear more willing to spend, no longer accumulating savings to the same extent as in 2024. The strong set of September data calls for the MPC to refrain from easing in November.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more