- Quick take

- 14 May 2026

- Poland

Poland’s growth slows but remains resilient against weak eurozone backdrop

The advanced stage of the public investment cycle is helping to shield the Polish economy from external shocks. But the surge in fuel prices threatens to undermine income growth and consumption. Industry is contributing less to GDP growth than in the past and the economy is becoming increasingly reliant on services

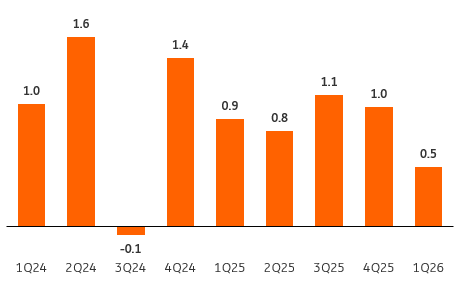

Poland’s GDP growth slowed to 3.4% year-on-year in the first quarter from 4.1% YoY in the fourth quarter of 2025. But the economy continues to expand at a solid pace despite geopolitical tensions, elevated uncertainty and weak economic conditions in the euro area. Seasonally-adjusted data points to growth of 0.5% quarter-on-quarter, following a 1.0% QoQ increase in the previous quarter.

After a difficult start to the year, when harsh weather conditions clearly weighed on economic activity in construction (double-digit declines in output) as well as in industry, March brought a marked rebound. However, this was not sufficient to prevent a slowdown in overall economic growth, especially when compared with the very strong fourth quarter of last year. On the positive side, the economy is maintaining a solid growth rate above 3% despite the unfavourable external environment and the fact that the natural growth engine – industry - is contributing less to economic growth than in the past. Full data, including the composition of GDP, will be released on 1 June.

Against the backdrop of uncertainty related to developments in the Middle East and an intensifying energy crisis, we have already revised down our GDP growth forecast for this year to 3.4% from the 3.7% expected at the beginning of the year. We expect the implementation of projects linked to the National Recovery Plan (NRP), which formally expires at the end of this year, to support the economy in the remainder of the year. Data for 2025 has already shown that public investment is picking up, while the revival of credit in the economy suggests that the public investment cycle is also spilling over into the rest of the economy.

A key risk factor ahead is the potential negative consumer response to higher fuel prices and a possible pullback in spending. The further rise in inflation that we expect, combined with slowing wage growth, would also reduce the pace of real income growth. In this respect, 2026 looks weaker than the previous two years, which were very strong.

The GDP data for early 2026 came in slightly below expectations, and the Monetary Policy Council is likely to maintain a wait-and-see stance in June as it awaits further information to assess the outlook for economic activity and inflation in the coming quarters. We expect the July inflation projection to be an important factor shaping discussions within the Council in the second half of the year. Our baseline scenario assumes that interest rates remain unchanged until the end of 2026. But prolonged gridlock in US–Iran talks and the continued blockade of the Strait of Hormuz increase the risk of higher interest rates.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more