- Quick take

- 13 February

- Poland

Poland’s current account deficit expands, but external balance remains healthy

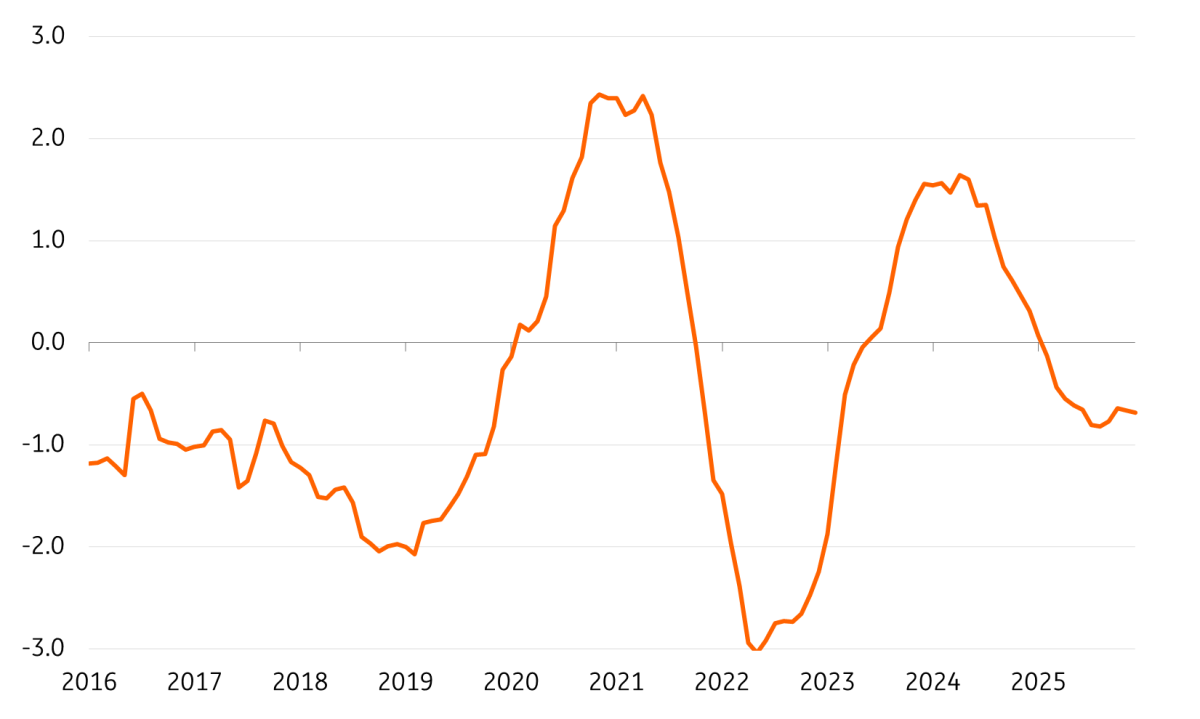

Poland’s current account deficit for December widened more than forecasted by market consensus but slightly less than we had projected. We estimate that the 2025 deficit amounted to 0.7% of GDP, switching from a tiny surplus of 0.3% of GDP in 2024. Poland’s external balance is still in a good place, in our view

The December current account recorded a balance of -€1,698m (we forecasted -€1,978m, consensus -€1,252m), following -€499m in November. We estimate that in 2025 the deficit amounted to 0.7% of GDP (similar to the figure after November), compared to a surplus of 0.3% of GDP in 2024. The scale of the external imbalance remains low and Poland’s external balance has returned to levels seen around ten years ago. This year, we expect a deficit of 0.9% of GDP, with the Polish economy remaining well-balanced externally.

The December current account deficit was the result of a goods trade deficit of €2.3bn (after a deficit of €1.1bn a month earlier) and a primary income account deficit of €3.1bn, as well as the traditionally high surplus in services trade of €3.3bn as well as a surprising surplus of €0.4bn in secondary income. The increase in the latter category probably stemmed from rising EU subsidy payments from the National Recovery Plan to final beneficiaries (these are recorded in transfers after disbursement of funds to final recipients).

The goods trade deficit was due to a 9.7% year-on-year rise in exports in euro terms and a 10.1% YoY increase in imports, marking the highest turnover in three years. It represented a solid acceleration in exports from 2.7% and in imports from 3.1% in November, accordingly. On a 12-month rolling basis, the merchandise trade balance in December remained at the same level as in November, i.e., -1.4% of GDP.

Commentary from National Bank of Poland (NBP) analysts, referring to the changes in the value of trade aggregates in PLN, indicates an acceleration in the dynamics of goods trade, partly supported by a greater number of working days compared to the previous year. On the export side, the strongest growth was observed in agricultural products and other consumer goods (clothing, video game consoles, footwear, and computers), suggesting a significant role for re-exports. Consistent with December data on industrial production, there was strong growth in the export of intermediate goods and parts for transport equipment, including aircraft engines. In the export of durable consumer goods, stagnation trends persisted, related to strong competitive pressure from China in this segment.

On the import side, growth was recorded in most major categories. The strongest was in imports of investment goods, primarily computers and intermediate goods, including semi-finished products made from iron and steel. Lower oil prices led to a decrease in the value of fuel imports.

Recognising the small current account deficit as a long-term equilibrium level, we expect the deficit to remain at 0.9% of GDP this year. We forecast a slight acceleration in GDP growth to at least 3.7% in 2026 from 3.6% in 2025 and assume a greater contribution of investment to GDP growth than in 2025, while net exports contribution is to remain slightly negative. In 2026, we expect higher growth in industrial production and exports than last year, thanks to the gradual recovery of external demand in the euro area. Data for the final months of 2025 suggest a recovery in Germany, particularly visible in industrial orders, but for the whole of this year, we expect Germany’s GDP to grow by 0.9%, after stagnation of 0.2% in 2025 and declines in real GDP in the previous two years.

From a macroeconomic perspective, the Polish economy remains solidly externally balanced, and the balance of payments data have little impact on short-term movements of the Polish zloty, which since the beginning of the new year has been trading below 4.23/€, and even tested the 4.20/€ level. For the FX market, decisions by global central banks are key, particularly fluctuations in market expectations regarding the scale of Fed rate cuts this year and decisions and communications from the Monetary Policy Council, which this year is expected to continue to cut NBP rates.

Poland’s current account balance in 2016-25 (% of GDP)

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more