- Quick take

Poland: Weaker retail sales on base effects but acceleration ahead

- 19 July 2019

High (negative) base effects mask the boost from generous pre-election social transfers. But retail trade and consumption should accelerate soon as these transfers raise household disposable income growth from an estimated 6% to 9% year-on-year

In June, real retail trade slowed to 3.7% YoY from 5.6% a month earlier. Unlike surprisingly weak industrial output, this outcome was in line with the consensus estimate and our own forecasts. The retail trade structure was also similar to previous months – showing strong growth in electronic equipment and household appliances (8.9% YoY), as well as auto sales (5.1%). Sales in non-specialist stores, pharmaceuticals and cosmetics were also higher, likely reflecting the bonus pension payment (which increased disposable income growth by a third in 2Q19). A negative surprise came from the 'others' category (-3.9% YoY), aggregating luxury goods and building materials.

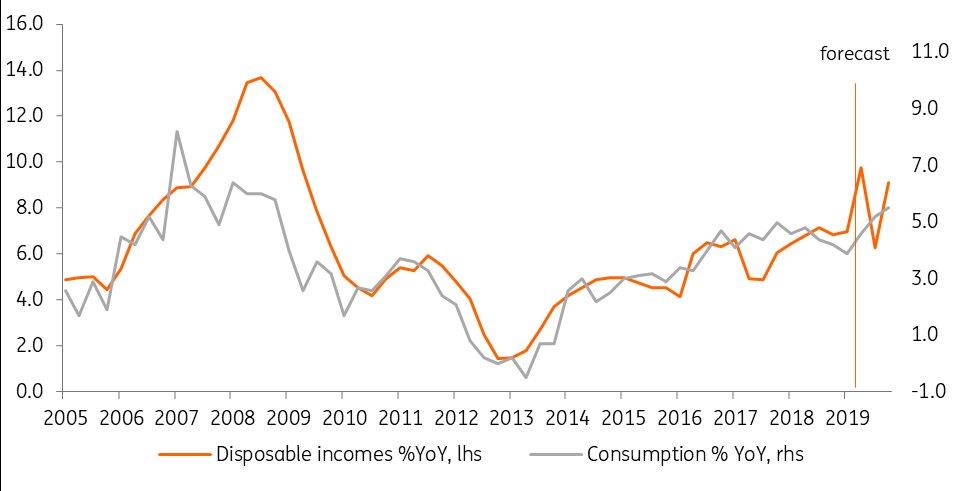

Consumption and disposable incomes

| 3.7% |

Real retail sales (YoY) |

| As expected | |

The slower overall pace of retail sales in June was caused by negative base effects. In the coming months, these effects will reverse and, together with the boost coming from election pledges, should result in higher retail trade (+5% YoY) and consumption.

Moreover, official GUS consumer surveys continue to indicate a high spending propensity for big ticket items like new cars. Disposable incomes should be further increased by another election benefit in the form of an extension to the 500+ child benefit (a bulk payment for July to September in 4Q).

Based on June activity data, we expect 2Q19 GDP growth at 4.6% YoY (prior to yesterday's weak production figure we estimated 5% growth). We also see some downward risk to our 2019 GDP forecast, currently at 4.7%.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more