- Quick take

- 21 March 2023

- Poland

Weak Polish retail sales add to gloomy outlook

Poland’s retail sales nosedived in February as elevated inflation took its toll on consumers' real disposable income, dampening household consumption. Along with poor industrial output figures, we expect a weak first quarter with downside risks to our -1% year-on-year GDP forecast

In February, retail sales of goods fell by 5.0% year-on-year (ING and the market consensus pointed to a 1.4% YoY decline) after an increase of just 0.1% YoY in January (data revised). The seasonally-adjusted data point to a drop in sales of 4.1% vs. January.

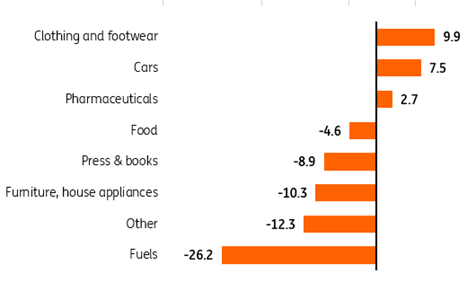

Retail sales data clearly show that elevated inflation is putting downward pressure on households' real disposable incomes and purchasing power. Most of the weak sales of durable goods last year were alongside rising purchases of necessities (food, pharmaceuticals, clothing and footwear). Consumers seem to be trimming their purchases of essential goods.

Purchases of food fell for the second month in a row (down by 4.6% YoY in February). At the same time, a sharp annual decline in fuel sales (-26.2%) can be attributed to a high reference base. In February 2022, customers rushed to gas stations after Russia invaded Ukraine (sales of fuels soared by 23.1% month-on-month).

The short-term prospects for retail sales are negative. In March 2022, sales of clothing and footwear, food and pharmaceuticals soared as the first wave of refugees from Ukraine reached Poland. Therefore we should brace for an even deeper annual decline in retail sales in March 2023.

Retail sales, month-on-month change

Rates to remain unchanged in 2023

The fourth quarter of 2022 was poor for household consumption and monthly data on sales of goods suggest that the first quarter of this year may be even worse. Along with data from the industrial sector released yesterday, figures from retail paint a gloomy picture of the first quarter. A decline in annual GDP was broadly expected, but risks to our -1%YoY forecasts are clearly to the downside now. On a positive note, construction data suggest that investment activity was still solid. The Monetary Policy Council is between a rock and a hard place as elevated inflation (especially core inflation) leaves no room for the National Bank of Poland to cut rates any time soon. We expect the main policy rate to remain unchanged until at least the end of 2023 and see no ground for debate on rate cuts due to uncertainty regarding the sustainable return of CPI inflation to the bank's target.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more