- Quick take

- 21 October 2020

- Poland

Polish retail sales rebound is starting to slow

Polish retail sales in September increased by 2.5% vs 0.5% year-on-year in August, close to the market expectations. Construction and assembly production fell by 9.8% YoY after a 12.1% decline in August

| 2.5% |

Growth of retail sales in PolandIn September (YoY) |

| As expected | |

Retail sales

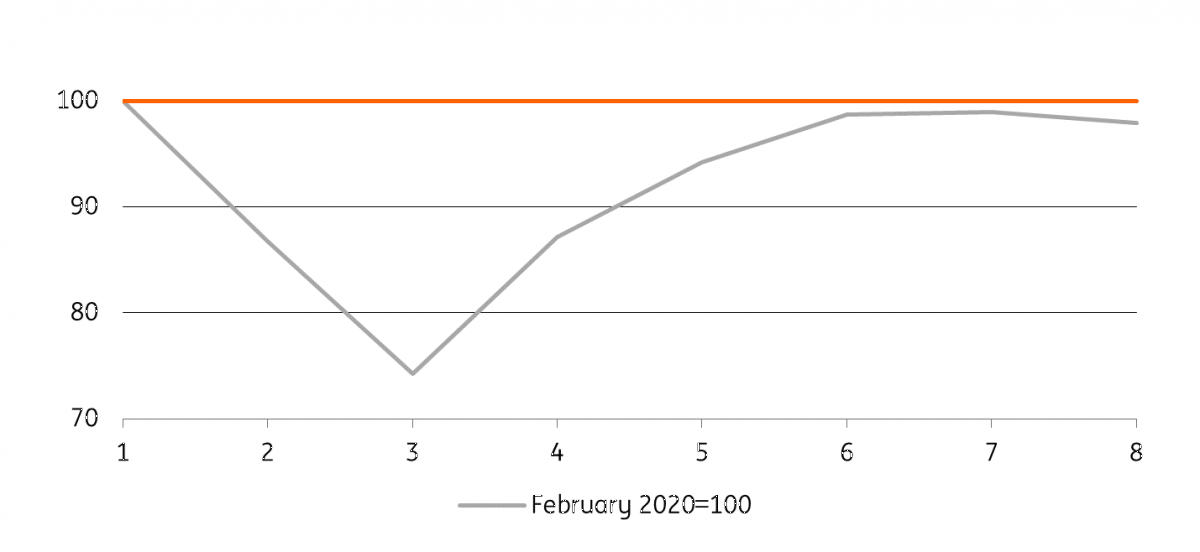

The rebound in Polish retail sales, which started in the second quarter, is slowing down.

Seasonally-adjusted month-on-month growth slowed for a fifth consecutive month, falling 1.0% in September. Retail sales remain 2.0% lower than in February 2020, but the gap has started to increase again.

Retail sales seasonally adjusted

The data shows a rebound in car sales, food and pharmaceuticals in YoY terms compared to August.

Sales of furniture, radio, TV and household appliances retained the highest growth, but somewhat slower compared to the previous month. (8.6% vs. 10.2%). The data indicates that Poles are still adapting their homes to the new reality: since the beginning of the pandemic, homes have had to serve as schools and in some cases, as offices.

In YoY terms, sales of clothing and fuel fell, probably due to the warm September.

First month since April when percentage of online sales increased again

September was the first month since April when the share of online sales increased (to 6.8% compared to 6.1% in August).

In April, online purchases accounted for 11.9% of total sales compared with 5.6% in February, before the outbreak of the pandemic. The highest monthly growth was recorded in press, furniture, radio, TV and household appliances. At the same time, visits to large stores fell. According to the Polish Chamber of Commerce, in September, supermarket sales (20% of sales) fell by 4.2% YoY, while sales in small-format stores (30% of total sales) increased by 5.9% YoY.

| -9.8% |

Growth of construction and assembly production in PolandIn September (YoY) |

| Higher than expected | |

Construction

Data on construction and assembly production was better than expected. In September, output fell by 9.8% after a 12.1% YoY decline in August. The relative recovery is primarily due to smaller decreases in the construction of buildings and civil engineering.

Construction output is still clearly below last year's levels, but is gradually beginning to improve in MoM terms. This is visible in companies engaged in specialised construction activities, which may suggest an acceleration of infrastructure investment in the coming months. This is also indicated by the dynamics of EU funds disbursed in September, which increased by 21% YoY.

Implications for GDP

We already have data on the performance of all major short-term indicators of the economy for 3Q20. The September results were better than expected, as suggested by the soft data, which confirms our expectation that GDP growth in 3Q20 was higher than the consensus (-2.9%). This means that GDP growth in 3Q20 in QoQ terms was about 8%, compared to -8.9% QoQ in 2Q20.

In 3Q20, the first phase of recovery, which resembles the “V” shape, was completed. Most likely, another slowdown awaits in Q4

The economy's performance in October will probably remain relatively good, as shown by a slight deterioration visible in the effective lockdown indexes. However, we believe that with the introduction of further restrictions, the economic situation will deteriorate in the coming months. For the time being, the restrictions only cover hotels, restaurants and sports and recreation facilities. However, the example of other countries shows that when a pandemic gets out of control, the pressure to introduce full lockdowns increases. This creates the risk of economic downturn on both, Polish export markets and domestically.

After updating the GDP forecasts at the beginning of September, we have the second-lowest GDP forecast for 4Q20 (-3.5% YoY and -1.8% QoQ). However, the strong 3Q20 compensates a lot. Assuming there will be no full lockdown again, the 2020 GDP growth rate will be between -2.9% and -3.5% YoY, and the economic situation after the pandemic will resemble a “W” shape.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more