- Quick take

- 19 February 2021

Poland: Extended lockdown impacts activity in January

After the relatively good industrial results we saw yesterday, retail sales and construction output came in worse than expected in January

| -6.0% |

Retail sales in January (YoY)consensus at -4.5% YoY |

| Worse than expected | |

Retail sales fell by 6.0% year-on-year compared to a 0.8% drop in December and the market consensus at -4.5%. Data on daily activity at retail stores signalled a fall. However, the scale of the decline turned out to be slightly deeper than our estimates.

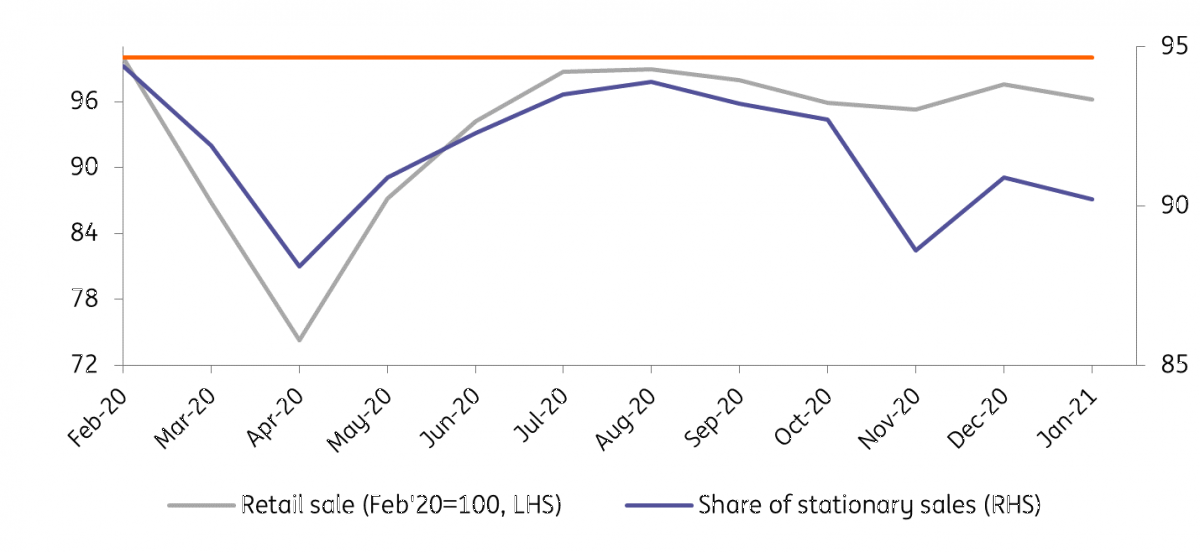

Seasonally-adjusted sales fell 1.4% month-on-month in January. This was due to extended restrictions on shopping malls, as Poles still prefer traditional brick-and-mortar stores. The growing share of online sales does not compensate for the decline in other channels.

Retail sales, the volume against the share of stationary sales

Detailed data shows that sales in most categories slowed in January in year-on-year terms compared to December. Trade restrictions distorted the seasonality of traditional sales, as clothing YoY growth plunged by 30ppt compared to December. Sales of furniture, household appliances and electronics showed positive momentum, accelerating by 7.1% YoY from 3.5% YoY in December.

| -10% |

Construction in January (YoY)consensus at -7.3% YoY |

| Worse than expected | |

Construction output in January declined by 10% YoY and fell short of market expectations (-7.3% YoY). A more severe winter than a year ago brought YoY declines in all areas of construction activity.

After removing the impact of seasonal factors, construction and assembly output continued to grow. In January, it rose by 1.7% MoM after a 1.9% MoM increase in December. This is a bright spot in the negative year-on-year picture.

Today's retail sales, as well as construction & assembly production data are the final piece of the important short-term economic activity puzzle in January. A relatively good outcome for industrial production and a significantly worse, albeit directionally expected, sales result show the critical importance of the course of the pandemic and related restrictions on the aggregate economic outcome.

February may be worse for the economy. Activity indexes based on population mobility and daily indicators for industry show a strong decline in Germany. We must remember that border controls, may further disrupt supply chains. The lockdowns in Europe are prolonged, we have a slow vaccination progress and the risk of a third pandemic wave. This tells us to be cautious in our 1Q21 growth estimates. We have consistently maintained our forecast of a slight quarter-on-quarter contraction of GDP in Poland in 1Q21.

Assuming vaccinations accelerate in the 2Q21 and restrictions are relaxed, growth should rebound, although it may be strongest in 2H21. For now, we maintain our 4.5% GDP growth forecast for 2021.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more