- Quick take

Poland’s central bank to hike rates by 50bp

- 4 January 2022

- Poland

We expect the National Bank of Poland to hike rates by another 50 basis points on 4 January. The data released since the December hikes calls for CPI upside pressure in the short- and long- term. Recent statements by central bank hawks call for a 50bp hike, and no more. We upgrade the terminal rate to 4.5%

We consider recent statements by Monetary Policy Council hawks Eugeniusz Gatnar and Łukasz Hardt as the important guidance for the January meeting. Both suggested a 50 basis point hike, indicating that a larger move is unlikely. Also, Governor Adam Glapinski said after the December decision that the following moves should be comparable in magnitude to the one in December (50bp). This is also reinforced by uncertainty on the economic impact caused by Omicron, which should affect economic activity, but only in 1Q22. Given a relatively low vaccination rate (55.3% vs EU average at 70.3% of fully vaccinated) Poland seems vulnerable to the more contagious Covid variant. Moreover, due to the January MPC meeting being moved earlier (4 January), the MPC will not see the December CPI print beforehand.

We estimate 4Q21 GDP to grow by about 7% year-on-year

The data released since the December meeting add to CPI upside pressure in the short- and long-term. The November activity data surprised on the upside and we also see strong production and exports (less so retail sales) in December. So overall, 4Q21 GDP should be very strong despite the simultaneous peak of new cases in the fourth wave of the pandemic – we estimate 4Q21 GDP to grow by about 7% year-on-year vs 6.5% YoY we and the NBP expected before. The main consequence of the resilient 4Q21 GDP is that companies can easily pass rising costs on to retail prices.

And there is so much to do here. The hikes of regulated prices (for households) released in December surprised on the upside, especially the new tariff for gas (54%), while electricity price hikes were in line with our expectations (24%). The anti-inflation shields, introduced by the government, should constrain the CPI spike in January (effectively splitting gas and electricity prices hikes between January and April or the following months given the likely extension of government anti-inflation measures). But still, the average CPI should be higher in both 2022-23 than we expected before. Gas and electricity prices for business are not regulated, but still companies expect new prices to be introduced in January and these can be easily passed on.

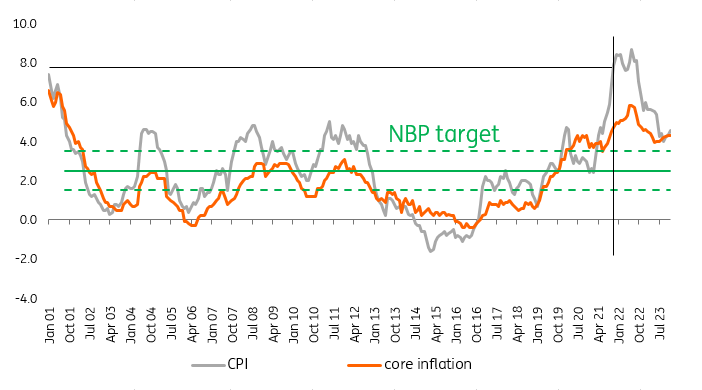

The wage-price spiral should translate into very high core inflation, rising from c.4.1% YoY in 2021 to c.5.1% YoY in 2022. We expect double-digit wage growth in 2022-23. The labour market is already very tight, while regulatory and fiscal measures will only add to wage pressures (eg, another strong rise in the minimum wage, increased effective tax rates for high-earners under the Polish Deal). This setup makes Poland one of the prime candidates for second-round effects to take place.

We see 2022 CPI at 7.7% YoY

Given all the above factors, we see 2022 CPI at 7.7% YoY (vs 6.7% YoY seen before), up from 5.1% in 2021. In 2023, CPI should gradually subside on base effects to around 5% YoY, but also here, we see a higher CPI trajectory than expected before (previous ING forecast for 2023 at 4.2% YoY, November NBP projection for 2023 at 3.6% YoY). Inflation should remain above the NBP's upper target band (3.5% YoY) much longer than the NBP expected when the projection was released in November.

Given the robust GDP performance in 4Q21, but more importantly, the extended period of CPI staying above the upper bound and the risk of long lasting second-round effects (coming from the current second wave of supply shocks and expected wage prices spiral we see in 2022) we upgrade our forecast for the terminal rate to 4% at the end of 2022 and 4.5% at the end of 2023.

The January MPC meeting will be the last one for two MPC members appointed by the Senate. At the end of January, two out of three Senate members should leave, ie, Eugeniusz Gatnar (hawk) and Jerzy Kropiwnicki (swing voter). They will be replaced with new candidates, ie, Ludwik Kotecki and Przemyslaw Litwiniuk, who will be appointed on 12 January. We believe the new MPC members should show a similar bias to those who are leaving their posts (Ludwik Kotecki said the NBP should follow the Czech central bank). The third candidate from the Senate, Joanna Tyrowicz, should replace the outgoing Rafal Sura by November 2022 at the latest. She should hold a more hawkish bias than Sura.

CPI inflation should stay above the upper bound till end of 2023

CPI and core inflation (%YoY)

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more