- Quick take

Poland: A cautious rate hike as growth outlook dims

- 7 July 2022

- Poland

The MPC raised rates by just 50bp, less than expected (ING and consensus at 75bp). This means there is a risk of the zloty weakening. EUR/PLN nearing the wartime shock peak (5.0/€) is possible, but much depends on tomorrow's conference. A repeat of the very soft rhetoric from June will be negative for the currency

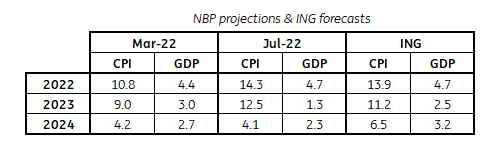

New projections shows high CPI, but technical recession in 2022 and slow recovery

Projections from the National Bank of Poland explain why there was only a 50bp hike. In our view, the Council was sensitive to the weak GDP outlook, despite the high CPI projection for 2022-23. The NBP projection sees GDP slowing sharply from 4.7% year-on-year in 2022 to 1.3-2.3% YoY in '23-24. That means a technical recession in 2022 (bear in mind GDP slowed from 8.8% YoY in 1Q22 below 2% in 4Q22), but also a very slow recovery in the coming quarters.

The NBP inflation projections for 2022-23 are even higher than our above-consensus expectations. They echo our worries about long-term inflation risks i.e. strong second-round effects and high inflation expectations. Actually, the double-digit CPI in the NBP projections for 2023 points to the risk of persistent and self-reinforcing price growth, which may be difficult to stop, while maintaining deeply negative real interest rates. In our view, these forecasts do not provide any room to end the cycle of rate hikes in the coming months. It cannot be ruled out that the NBP's strategy is to extend the time frame for tightening.

We also point out that the sources of the GDP downturn that both we and the NBP see, are external. Also, an economic slowdown will not significantly reduce tensions in the labour market, and the risk of a strong rise in the unemployment rate is low. An overly dovish stance by the MPC could further weaken the PLN and prolong the period of elevated inflation.

Limited changes in statement, but those we see point to weaker GDP outlook with persistent inflation

There are no major changes in the post-meeting statement other than noting the expected slowdown in GDP. The comment saying that relatively favourable economic conditions are likely ahead was removed. The MPC also expressed its preference for a strong zloty, which in their view is consistent with the fundamentals of the Polish economy.

Dovish MPC calls for weaker PLN

The moderate hike of 50bp points to a risk of the PLN weakening. EUR/PLN nearing the wartime shock peak (5.0/€) is possible, but much depends on tomorrow's conference. A repeat of the very soft rhetoric from June will be negative for the currency.

It remains to be seen whether the NBP will pursue the Czech model, i.e. softening of the bias and FX intervention to defend the domestic currency. The Czechs have used 4.5% of reserves (!) to intervene in recent weeks. For now, EUR/PLN defence at 4.80 is strong, but a softer NBP policy bias accompanied by a rising dollar puts the zloty at significant risk.

We still expect a terminal rate at 8.5%, but it may take longer to get there

We still expect the terminal rate at 8.5%, although it may take more time to reach that level. In our view, the projections don't show any room for a rate cut in 2023. The MPC's dovish stance may backfire via a weaker PLN, which should finally trigger further hikes. The NBP may attempt currency intervention but we are concerned about its effectiveness in the long run.

NBP projections and ING forecasts

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more