Pipeline pressures support the US soft landing view

After yesterday’s big reaction to the benign CPI data, which saw risk assets rally hard and the dollar come off as interest rate expectations fell sharply, it is the turn of retail sales and producer price inflation today. It once again feeds the soft landing narrative with subdued price pressures and resilience in activity

Last month, US retail sales surprised to the upside, rising 0.7% month-on-month despite credit card transaction numbers looking weak and we get a repeat of that for today’s October report. Headline retail sales fell 0.1% MoM, but this was better than the 0.3% drop expected, while September’s 0.7% initial print has been revised up to 0.9% MoM growth. The details show motor vehicle sales fell 1%, which tallies with the drop in unit sales reported by manufacturers while furniture sales dropped 2% MoM – the fourth consecutive monthly decline, which is consistent with the collapse in housing transactions on the basis that when you move home buyers tend to also buy a few new items. Gasoline station sales fell only 0.3% MoM despite the price of gasoline plunging while department stores and miscellaneous stores had a tough month with sales down more than 1% MoM.

On the positive side it was a good month for health & personal care (+1.1%) while groceries and electronic both rose 0.6% MoM. Clothing was flat on the month and non-store (internet) rose 0.2%. Therefore the control group, which better matches the trends of broader consumer spending via removing volatile items such as autos, gasoline, building materials and eating out, came in at +0.2% MoM as expected. This indicates decent resilience and supports our view that fourth quarter GDP growth may not be as weak as the consensus is currently predicting – consensus is currently predicting 0.7% annualised 4Q GDP growth while we are forecasting 1.5% GDP growth.

WoW change in credit card spending

There will no doubt be some scepticism of the resilience in retail sales given the credit card spending numbers have been so soft over the past couple of months – are we all really returning to cash? But this is the life of an economist at the moment – data inconsistencies everywhere.

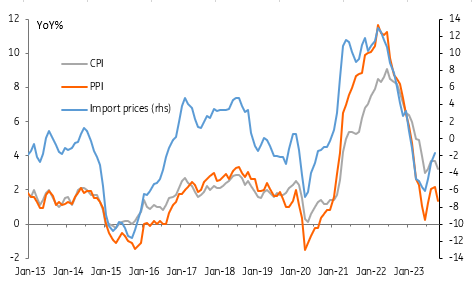

PPI shows weak pipeline price pressures

Meanwhile, pipeline inflation pressures as measured by PPI are very soft with headline producer prices falling 0.5% MoM versus +0.1% consensus while core (ex food & energy) was flat on the month (0.3% consensus). This means that the annual rate of producer price inflation has slowed to 1.3% year-on-year from 2.2% while core is at 2.4% versus 2.7% previously. With wage growth looking more subdued amidst rising productivity growth, it reinforces our view that we will start consistently getting 2% CPI YoY prints at some point in the second quarter of 2024, giving the Federal Reserve the ability to respond to any eventual economic weakness with interest rates cuts.

Import prices, PPI and CPI (YoY%)

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap