- Quick take

- 19 November 2019

Philippines: What’s better than a super budget? Two of them

The Philippine congress passed a bill seeking to extend the validity of the 2019 budget, bringing the prospect of a parallel fiscal push in 2020

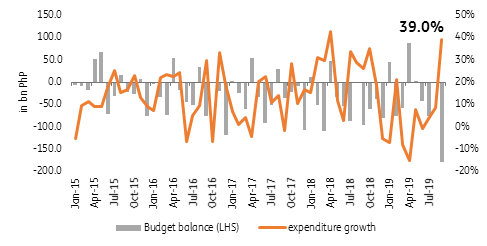

Philippines budget balance and expenditure growth

Fiscal push could last well into 2020

The Philippine congress has approved a bill extending the validity of the 2019 budget (both for operating expenses and for capital outlay) until December 2020. Although the bill will require approval from both the Senate and the President, this development is crucial to ensure that the sustained fiscal push which helped lift 3Q GDP to 6.2% (September surged by 39%) will continue to deliver. Given cash-based budgeting, the government would not be able to carry project funds over to 2020 without this bill being passed into law, making this development worth noting. And although public construction and operating and maintenance costs of the government account for a mere 13% of overall GDP, the recovery in government spending was able to provide a welcome boost to 3Q GDP growth momentum, as capital formation remained in the red.

What's better than a super budget? Two of them

The International Monetary Fund (IMF) upgraded its 2020 forecast to 6.3% (from 6.2%) on expectations the 2020 budget would be approved and as the Bangko Sentral ng Pilipinas (BSP) walks back part of the 2018 rate hike cycle. Most analysts also point to possible clearer skies in 2020 should the budget be passed on time and global headwinds fade. However, should the 2019 budget be extended, we are now faced with the prospect of a double dose of fiscal stimulus (2019 and 2020 operating in parallel) in tandem with BSP’s current easing cycle. From here we can see even faster GDP growth in 2020, base effects withstanding, with robust consumption, rejuvenated investment and the two-headed fiscal budget working together to deliver a solid growth performance next year. Should these factors come together, the prospect of effectively chasing the higher 2020 growth target of 6.5-7.5% will become more tenable, with or without a global slowdown.

Spend spend spend = borrow borrow borrow

The projected increase in spending will ostensibly result in an increase in borrowing from the national government in late 2019 and into 2020. We expect liquidity conditions to tighten considerably in 1Q 2020, just as they did in early 2019, with the national government bond issuances expected to crowd out the rush of private sector capital raising exercises. We forecast that the tighter liquidity conditions could prod the BSP to sustain its easing momentum but tighter liquidity conditions could still very well see bond yields revisit an upward trajectory.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 20 November 2019

- This bundle contains 3 Articles