- Quick take

No move from the Philippines’ central bank despite inflation threatening to breach target

- 24 March 2022

- Philippines

The BSP keeps its policy rates untouched for an 11th straight meeting but could eventually fall behind the curve

| 2.0% |

BSP policy rate11th straight pause |

| As expected | |

Central bank stands pat, again

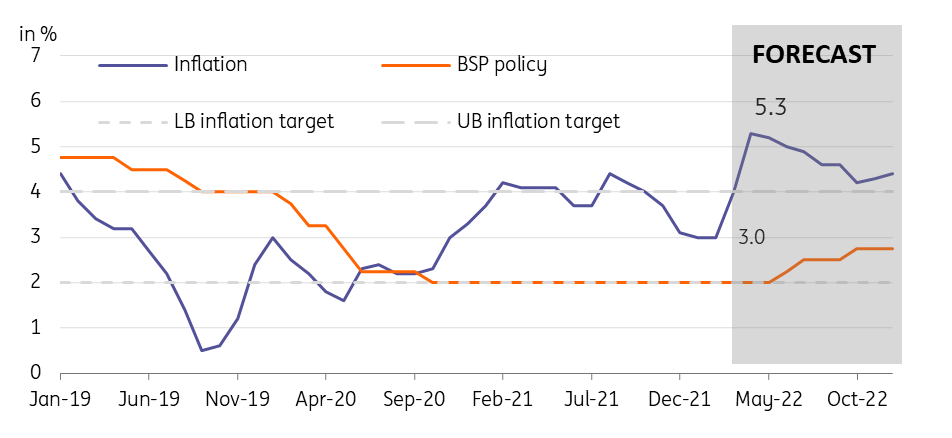

Bangko Sentral ng Pilipinas (BSP) retained its accommodative stance on Thursday. The central bank opted to keep rates untouched yet again citing the need to safeguard the economic recovery even as they described the economy as having “gained stronger traction”. BSP Governor, Diokno, cited the uncertainty of the ongoing war in Ukraine and potential fresh waves of Covid as the main reason for the pause. Inflation forecasts were adjusted higher with the central bank now expecting the headline rate to jump to 4.3% (3.7% previously) in 2022 and 3.6% (3.3% previously) next year.

It's getting hot in here

Given the exposure of the Philippines to the global commodity price surge, we are expecting inflation to quicken rapidly in the coming months. The Philippines is heavily reliant on imported crude and elevated prices for energy have already manifested in the domestic market. Local fuel prices are currently 45% higher than the same period last year, suggesting a stark pickup in transport costs and utilities.

The price of other integral imports such as rough rice, a key staple for the country, is also edging higher. Rough rice in the world market is up 10% and could figure into domestic inflation soon enough. We expect full-year inflation to settle at 4.3% with the headline number cresting 5% as early as May.

It's getting hot in here: Inflation to breach target yet again this year

BSP likely behind the curve

Despite these developments, Governor Diokno has reiterated his preference to maintain an accommodative stance to support the economy. Furthermore, he has given forward guidance suggesting that a rate hike would likely be delayed to the second half of the year. That indicates he needn't move in lockstep with the Fed’s tightening cycle. However, a delay to the second half of the year could translate to BSP falling behind the curve as other global central banks, such as the Fed could have possibly raised rates by as much as 100 bps.

A prolonged pause from the BSP even in the face of surging inflation could result in the de-anchoring of inflation expectations, requiring a more forceful tightening cycle from the bank down the line. Given today’s pause, we continue to price in a depreciation bias for PHP given the widening differential with the Fed and as pricier imports translate to increased dollar demand in the Philippine spot market.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more