- Quick take

- 25 April 2017

Our guide to May’s US jobs data

Why today's jobs numbers won't give the Fed too much to get excited about

Authors

Jobs growth: Weak

An unusually warm February was only partly to blame for last month’s surprise 98k figure. There was broad-based weakness, notably in services, which we would expect to at least partially correct this month. But in any case, the Fed seems happy with slower jobs growth as the economy nears full employment.

| 150k |

Change in Non-farm Payrolls (000s)(Consensus: 190k) |

Wage growth: Weak

At complete odds with payrolls, the household survey shows that almost one million jobs have been added in the past two months. This survey does tend to swing around, and we suspect we’ll see some correction. The unemployment rate could tick up, but anything sub-5% is considered close to full employment.

| 2.6% |

Average hourly earnings growth (YoY%)(Consensus: 2.7%) |

Unemployment rate: Higher

There’s little doubt that tight jobs market conditions are driving up pay. But for the Fed to take the pace of rate hikes up a notch, we need to see wage growth go above 3%, and that’s not likely until much later this year. This, and sub-2% core PCE, are two key reasons why we think a June rate hike is still a 50:50 call.

| 4.6% |

Unemployment rate(Consensus: 4.6%) |

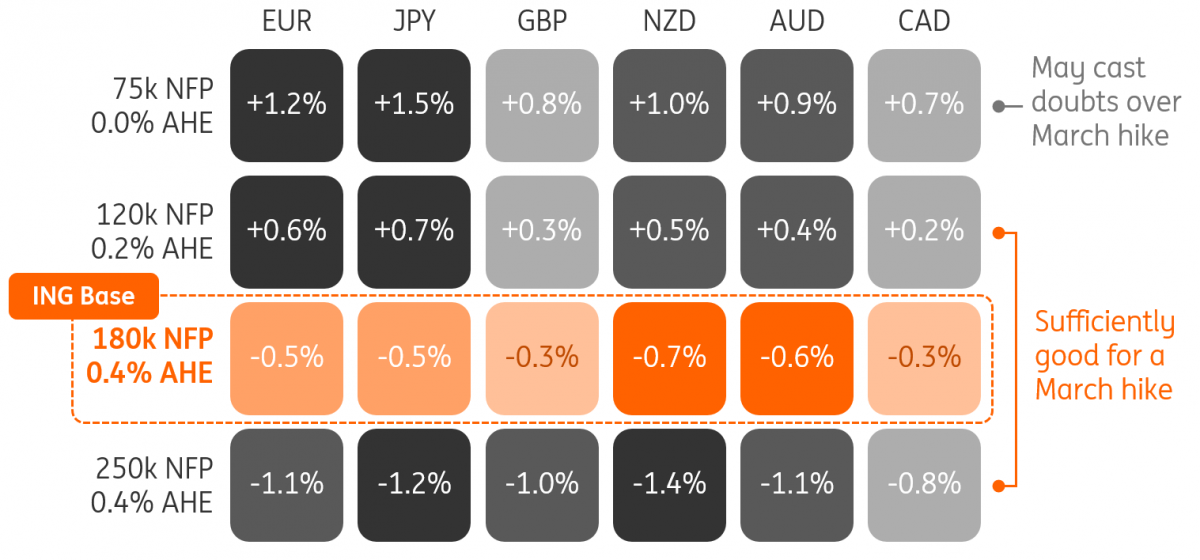

FX Playbook: How markets could react

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more