- Quick take

- 3 October 2019

- Russia

Russia: FX interventions not a big deal for RUB in 4Q19

The increase in FX purchases in October is not a big concern for the ruble, which shoud benefit from a sizable seasonal expansion of the current account surplus in 4Q19. Balance of payments data for 3Q19 to be released next week will show how signinficant the main risks - related to non-oil exports, private capital outflow, and portfolio flows to OFZ - are.

| 213bn |

Minfin FX purchases for October in RUBUp from RUB187bn in September |

| As expected | |

CBR/Minfin to increase monthly FX interventions in October, on a spike in the oil price

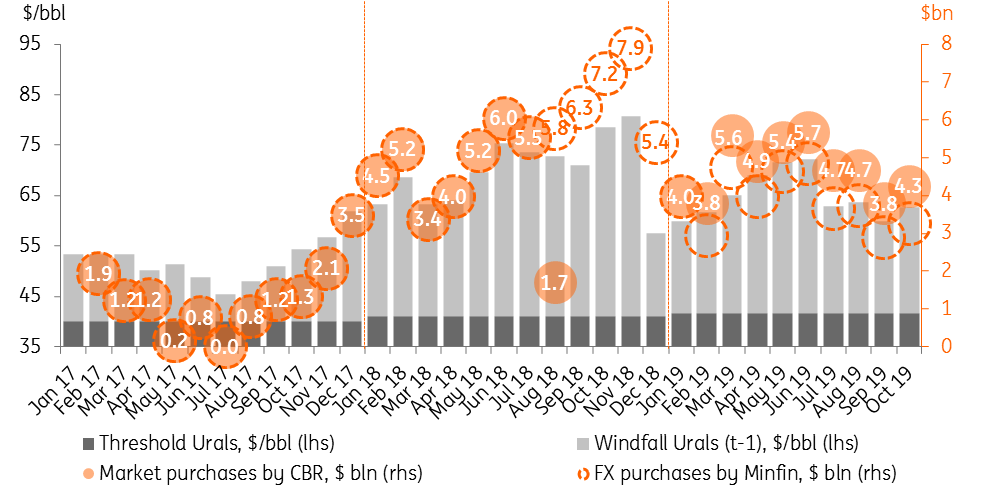

The Russian finance ministry has announced that it will spend RUB213bn (equivalent to USD3.3bn at the current exchange rate) for FX purchases between 7 October and 7 November, close to the RUB220 bn expected by us and the market. The amount comes from the RUB205bn in extra fuel revenues for the budget expected in October and the RUB8bn upward revision in extra fuel revenues for September. Combined with the August-December 2018 backlog, when the central bank put market purchases on hold, the total amount of FX to be purchased on the market will be $4.3bn in October, up from the $3.8bn seen in September.

The increase in FX purchases in October corresponds to a $3/bbl spike in average Urals price in September vs. August, following the drone attack on oil facilities in Saudi Arabia in the middle of September. The effect of this - even on the oil price - seems now to have evaporated.

Monthly FX purchases by Russian Finance Ministry/Central Bank

FX interventions are less of a concern for RUB in 4Q19

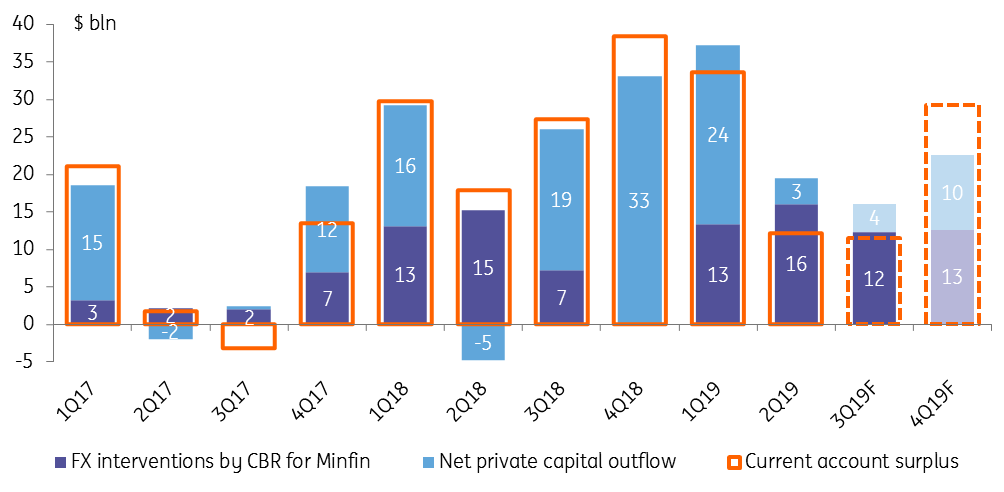

The likely seasonal increase of the current account surplus in 4Q19 suggests that FX purchases will be less of a concern for the rouble in October-December than in previous months. According to our estimates, the current account surplus is set to increase from $12bn in 3Q19 (to be confirmed next week by the Bank of Russia) to $25-30bn in 4Q19, suggesting a drop in sterilization from 100%+ to 40-50%. This is the key reason for why we maintain our expectations of a slight USDRUB appreciation to 64.0 by year-end. However, this constructive view faces a number of risks:

- After contracting in 1H19, Russia's non-fuel exports (40% of total merchendise exports, and including metals, agricultural products, and manufactured goods) might come under additional pressure from the global trade slowdown. According to the recently released numbers, 2Q19 exports dropped almost 5% YoY in real terms, partially on one-off factors, while global concerns remain for the medium term .

- The private capital account remains negative and its predictability remains low. While foreign debt seems to have stabilized and is unlikely to decline by more than $5bn in 4Q19, according to our calculations, accumulation of foreign assets remains an issue. The key focus of the upcoming 3Q19 balance of payments statistics will be net private capital outflow volume and structure.

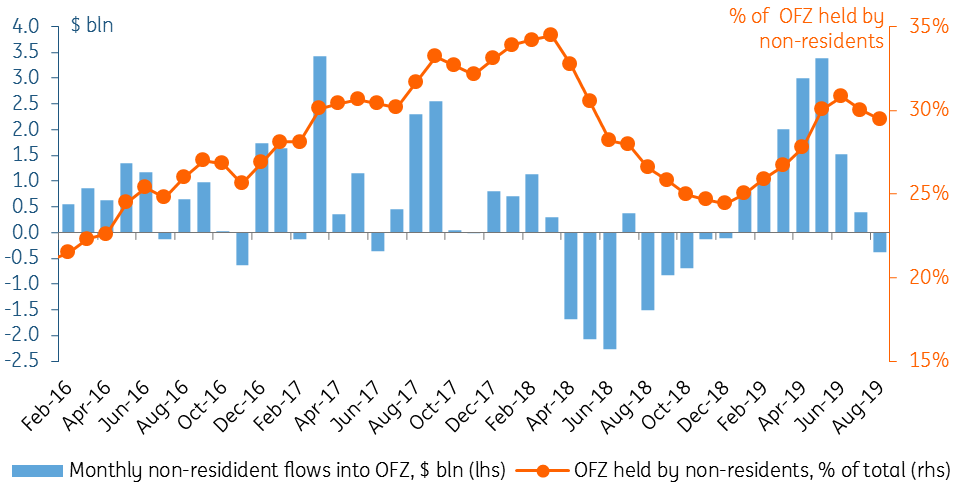

- Non-resident inflows into the local public debt market (OFZ), still the key balancing item for the ruble, have seen uneven performance in recent months and, according to the latest available data, turned negative in August. This was after a recovery in international funds' positioning in Russia to pre-2018 levels, having increased by $12bn over January-July 2019. While Russia remains an attractive borrower, portfolio inflows are subject to constraints linked to the limited amount of Minfin placements relative to 1H19 and to volatility in EM risk appetite.

Quarterly current account surplus vs. FX interventions and private capital outflow

Monthly inflows to / outflows from local state bond market (OFZ) and USDRUB exchange rate

The likely seasonal increase of the current account in 4Q19 lowers the importance of FX purchases for RUB which we continue to see appreciating to 64.0 by year-end, all else equal. In the meantime, non-oil exports, private capital outflows and non-resident participation in OFZ remain factors to watch at the upcoming balance of payments data for 3Q19 to be released next week.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more