- Quick take

Norges Bank: Air of caution creeps in as global risks mount

- 15 August 2019

- FX Norway

Intensifying global trade tensions have prompted the Norges Bank to adopt a more cautious stance. A December rate hike still seems more likely than not - domestic growth is being supported by a steep rise in oil investment. But as is the case everywhere, a lot will depend on how the trade war evolves between now and then

Having already hiked interest rates twice this year, the big question going into the latest Norges Bank (NB) meeting was whether policymakers would explicitly hint at a third move in September. Amid rising global uncertainty, the central bank decided to keep its cards close to its chest.

A rate rise at the next meeting still shouldn't be completely ruled out, but if the central bank is to follow through with its plan to tighten policy again this year, we think a December move looks much more likely

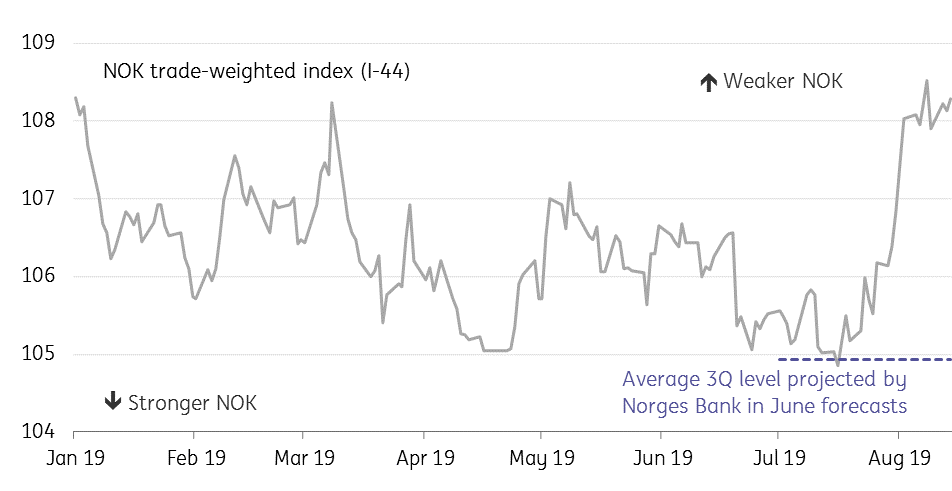

However, the Norges Bank did say that its rate outlook is "little changed" since June. While oil prices have dropped, the Norwegian krone has been significantly weaker than policymakers had factored in their forecasts. While global interest rate expectations have fallen dramatically this year - something that would generally translate into a lower NB interest rate path - most of this move had already occurred before the June meeting. Since then, US and eurozone rates have changed little.

So in the end, the decision to opt against signalling a September rate hike came down to global growth concerns. A rate rise at the next meeting still shouldn't be completely ruled out, but if the central bank is to follow through with its plan to tighten policy again this year, we think a December move looks much more likely. Don't forget that while the global outlook has clouded, the domestic growth outlook continues to receive support from a sharp rise in oil-related investment.

A December rate hike still remains our base case, although ultimately it will all depend on how the global trade war evolves between now and then.

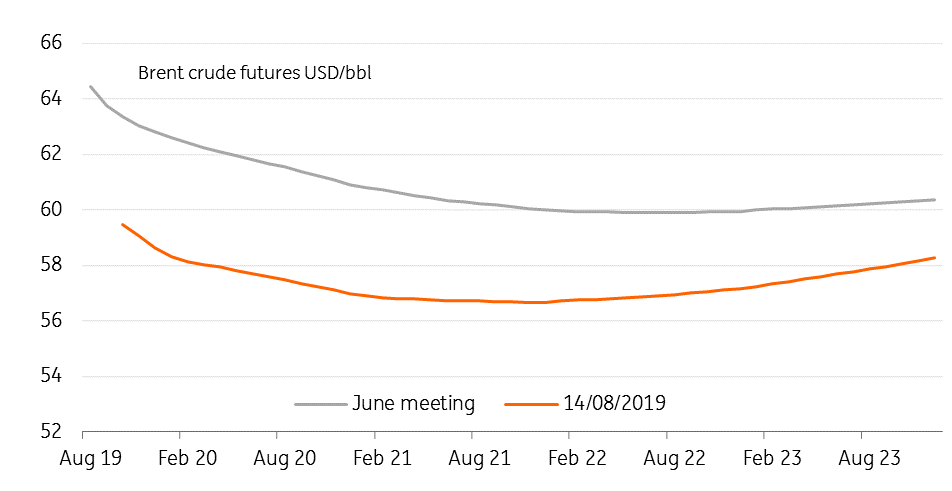

Oil prices have fallen since the June meeting...

... but this has been offset by a weaker NOK

FX implications: More NOK weakness in sight

The krone modestly declined in response to the more cautious statement, which failed to provide guidance on a hike in September. This means that the next move higher, if there is one, would only come in the December meeting. As the December meeting is still quite far away and in the meantime the trade situation may worsen (which could, in turn, reduce the odds of NB moving at the end of the year), the current forward guidance on a rate hike later this year won’t have a supportive effect on NOK.

With no help coming from the central bank for the battered currency (even if it had come, it would have had a short-lived effect on NOK anyway, as the overriding driver of the currency is the trade war situation) the krone will remain driven by trade tensions and its effect on global risk appetite alongside the oil price over the coming weeks/months.

Given the clouded outlook on the former, risks to EUR/NOK are skewed to the upside and the cross is likely to head to/above EUR/NOK 10.10 in coming weeks.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more