- Quick take

- 25 October 2018

- Turkey

No surprises from the central bank of Turkey

Turkey's central bank kept the policy rate unchanged at 24% while pointing out the upside risks to the inflation outlook, ongoing strength in external demand and the slowdown in economic activity

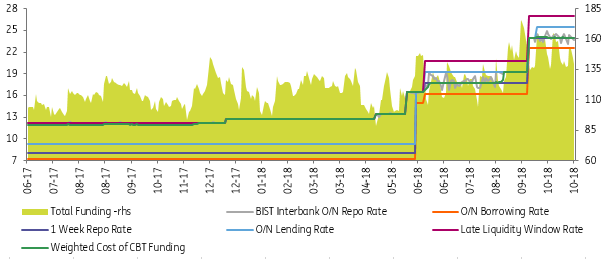

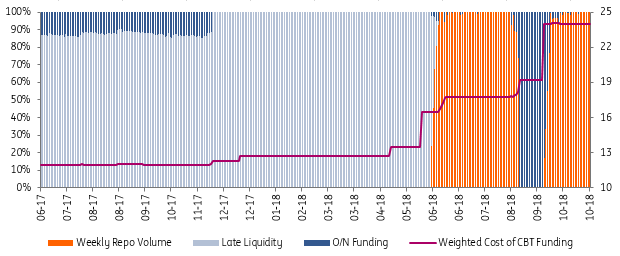

Key central bank of Turkey rates (%)

Policy rate flat at 24%

At today's meeting, the central bank of Turkey kept the policy rate unchanged at 24%, in line with the Bloomberg median consensus and our call. This is following the sharp adjustment last month and with the recent lira strength on the back of Pastor Brunson’s release and subsequent signals from the US on lifting some sanctions.

Markets first reacted negatively, and the lira moved to above 5.70 against the dollar, though later recovered towards 5.62s.

As we wrote before the meeting, the current recovery process of the lira could reduce some repercussions that we have witnessed since the beginning of this year including the declining FX pass through on inflation, given the high correlation between the lira's performance and core inflation. Secondly, the improving financial stability with a better operating environment for Turkish corporates that have a substantial short FX position.

That would be a relief factor for the central bank along with improvements in the geopolitical picture that will likely support the capital flow outlook, despite continuing fundamental macroeconomic challenges, such as inflationary pressures.

Minor changes in the statement

In the statement, the central bank's growth assessment was broadly unchanged, pointing to the “slowdown in economic activity continues”, with an addition in the October statement that it is “partly due to tighter financial conditions”.

But, most importantly, the Bank remained vocal about price stability risks by, once again, reiterating price increases showing “generalised patterns across sub-sectors, reflecting the movements in exchange rates”. They also acknowledged upside risks in the inflation outlook despite “weaker domestic demand conditions will partially mitigate the deterioration”.

Accordingly, it maintained a hawkish bias, keeping the main policy guidance in the statement unchanged. So, while highlighting the determination to tighten further, if needed, the bank will continue to monitor the lagged impact of recent monetary policy decisions and the contribution of fiscal policy to rebalancing process in addition to inflation expectations, pricing behaviour and other factors affecting inflation.

Despite the deteriorating inflation outlook with a surge in forward-looking expectations and fall in the ex-post real rate to the negative territory again, the central bank remained quiet.

This is probably because of rapid improvement in financial stability risks, the ongoing impact of recent financial volatility on the growth outlook, and expectations about the impact of the 10% price cut campaign on the inflation trend.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

In case you missed it: A flurry of central bank meetings

- This bundle contains 11 Articles