- Quick take

- 6 March 2024

- Poland

Poland keeps rates on hold, CPI projections not that optimistic

The National Bank of Poland kept rates unchanged with the reference rate remaining at 5.75%. The central bank sees upside risks to CPI

The decision

In line with market expectations and our own, the Monetary Policy Council (MPC) left rates unchanged (the reference rate is still 5.75%).

The MPC's post-meeting statement supports our call, i.e., better short-term CPI prospects, as inflation should remain close to the National Bank of Poland's (NBP) target (low demand, local cost pressures and a decrease in inflationary pressures abroad). At the same time, the MPC emphasises the risks to inflation in the medium term: the impact of fiscal and regulatory policy, economic recovery and tight labour market.

We see the elevation of the risks to inflation to "significant uncertainty" in the post-meeting statement as key, whereas a month ago it said "only" uncertainty. This change strongly suggests that tomorrow's press conference should be similar in tone to the one in February and therefore rather hawkish.

The new projection

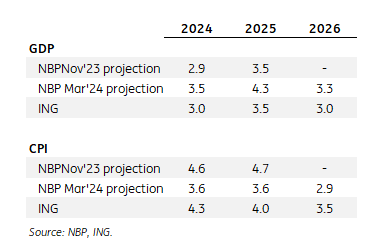

The new projection shows a very optimistic picture of the economy, the so-called 'goldilocks economy'. The inflation path has fallen and GDP has risen, compared to the November projection. CPI reaches the target as early as 2024.

In the case of the CPI projection, the assumption is that the anti-inflation shields (freezing electricity and gas prices plus zero VAT on food) will be maintained until the end of the projection. When adding the assumption of a VAT increase on food starting in April and a gradual normalisation of energy prices in mid-2024 to the projection, CPI would be about 1-1.5 percentage points higher than the NBP projection, which would mean that the average CPI in 2024 would be around 5% year-on-year, higher than the November projection. The March projection would also be higher than ING's inflation forecast. We assume that at the press conference tomorrow Chairman Glapiński will say that this is the most optimistic version, but that risks to CPI are to the upside, and they come from the regulatory policy side.

NBP projections comparision

As for GDP, the upward revision of the forecast in this projection is probably based on the Recovery and Resilience Facility (RRF) effect. If the rules of the programme remain unchanged, all of the RRF money would have to be spent in the next 2.5 years while other countries have had 5-6 years to do so. In our forecasts, we are more cautious on GDP growth, as we have a slightly worse outlook on the condition of the euro area economy. On top of that, we take into account a possible extension of the deadline for the implementation of the RRF, which would make it unnecessary to accumulate spending in 2.5 years, and its effect would be more spread out over time.

The key to assessing the path of inflation from the projection is to know the assumptions behind it, especially regarding electricity and gas prices. We should learn these during tomorrow's press conference by NBP President Glapiński, and more details on this issue will be provided by the presentation of the projection by NBP economists, which will most likely take place on Friday.

Our take

The CPI projection after adding the effect of the VAT increase on food and the gradual unfreezing of electricity bills (we assume an increase in the distribution fee) is higher than our current CPI forecast for 2024 (4.3% YoY).

Therefore, at tomorrow's press conference, the NBP president is likely to take a cautious approach, as suggested by the post-meeting statement of "considerable uncertainty".

He may also reiterate expansionary fiscal policy, as well as a tight labour market and robust wage growth.

We expect the government to take measures to curb the rise in household energy prices, which, in the context of a marked decline in wholesale electricity and gas prices, significantly improves the chances of inflation returning to target in the medium term. Our baseline scenario assumes that NBP rates should remain unchanged until the end of the year, but conditions may emerge in the second half of 2024 for a discussion of a symbolic rate cut. In 2025, we see room for interest rates to fall around 75-100bp.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more