Mixed messaging on US data still argues for a Fed delay until May

The US data continues to refuse to convincingly break one way or another. This will leave members of the Federal Reserve unconvinced there is enough evidence to justify cutting interest rates as soon as March. We favour a May start point, but when the cuts come we believe they will be significant

Some dovish news

In the wake of Jerome Powell’s pushback against the prospect of a March interest rates cut – see our Fed meeting reaction here – the market is now only pricing around 9bp for that meeting, effectively a 37% probability of a cut, having been near enough 100% priced at the start of the year. Today’s data hasn’t shifted that at all, but there are some interesting stories.

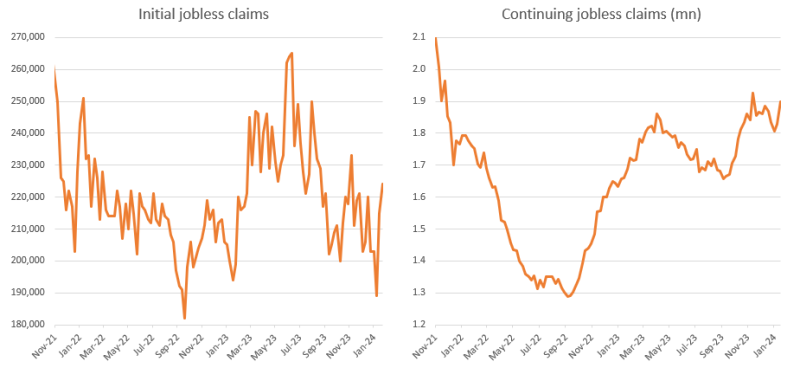

On the dovish side, that could be used to argue for a March cut, we see that fourth quarter productivity was stronger than expected at 3.2% and consequently unit labour cost growth was more benign, growing just 0.5%. This is a nice combination that suggests little inflation emanating from the business sector, which was also evident in yesterday's softer employment cost index. We also note the uptick in jobless claims. Initial claims rose 224k last week from 215k the previous week (consensus 212k) while continuing claims rose to 1898k from 1828k (consensus 1839k). Both are trending higher, but not hugely so – effectively further evidence of a cooling, but not collapsing, jobs market.

Jobless claims numbers are creeping higher again

But also some stronger data

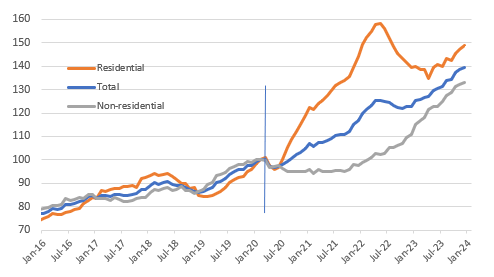

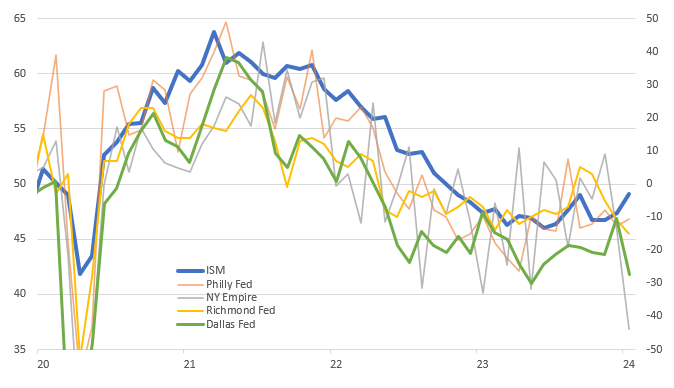

On the more hawkish side that argues for a delay on rate cuts we have a surprisingly strong manufacturing ISM index for January, rising to 49.1 from 47.1. This is still below the breakeven 50 level, as it had been for the previous 14 months, but is a signal that the rate of decline is slowing. Meanwhile construction spending for December rose 0.9% month-on-month after a 0.9% increase in November, which brings the series into line with the strong data seen within last week's fourth-quarter 2023 GDP report. Residential construction jumped 1.4% with the rise in home prices through the second half of last year and lower mortgage rates boosting home builder sentiment while non-residential rose 0.4% MoM. A bit of a slowdown, but it is still up 20.1% year-on-year with the CHIPS act, designed to incentivise domestic investment in chip fabrication, a big support factor in what has been going on.

Nominal construction spending (Feb 2020 = 100)

The ISM is a surprise because all of the regional manufacturing indicators have been so weak and pointed to a deterioration. Now, there isn't a regional survey covering West of the Rockies, but we can use the Chinese PMI as a partial proxy and that too was weak. The details show orders improved from 47 to 52.5, which is the first number in growth territory since May 2022. However, the backlog of orders is very weak at 44.7 and output is little changed, coming in at 50.4. Employment remains in the doldrums at 47.1 suggesting jobs are being shed.

Unfortunately the prices paid component jumped to 52.9 from 45.2, which is the highest since April last year, but for context we had readings of 90+ at the peak of the supply chain strains in 2021, so today's number in no way threatens a resurgence of price pressures in itself.

ISM stronger than regional surveys implied

Fed to wait until May, but will then cut rates significantly

All in, we remain happy with our call that the Fed will wait until May before cutting interest rates. By May we think ongoing subdued core inflation measures will give the Fed the confidence to cut with the policy rate getting down to 4% by the end of this year and 3% by mid-2025. This will merely get us close to neutral territory – the Fed’s view is that 2.5% is likely the long-term average. If the economy enters a more troubled period and the Fed needs to move into 'stimulative' territory there is scope for much deeper cuts than we are forecasting and the market is pricing.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap