US Fed indicates March likely too soon for a rate cut

The Federal Reserve has left monetary policy unchanged and while it removed its tightening bias, it doesn’t seem to be in a hurry to cut interest rates. We still think May is the more likely start point for policy easing rather than March, even if the arguments for earlier moves are building

Fed caution argues against a March rate cut

No change from the Federal Reserve on interest rates (target range kept at 5.25-5.50%) and it has removed its tightening bias, as widely expected, but there is a bit of push back on the market pricing that was favouring a March interest rate cut. The Fed say that while employment and inflation goals are “moving into better balance” they don’t think it would be “appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent”.

We suspect that the Fed recognises its credibility was damaged by its "inflation is transitory" assertion in 2021 only to have to rapidly reverse course with significant rate hikes through 2022 and 2023. The last thing the Fed wants to do is get it wrong again at a key turning point, loosen too soon, too quickly and reignite inflation pressures. After all the statement acknowledges the economy has been “expanding at a solid pace”, the unemployment rate is just 3.7% while equity markets remain close to all-time highs.

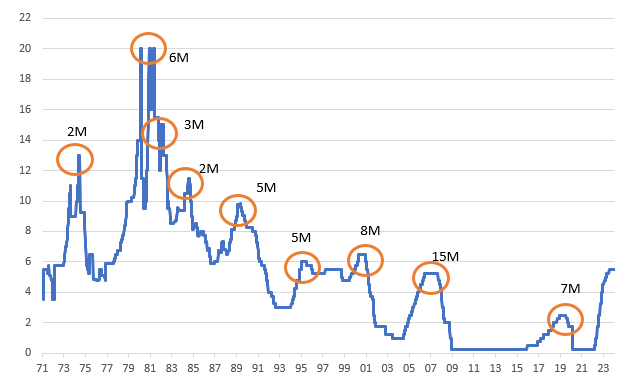

Fed funds target ceiling rate (%) with periods between last hike in a cycle and the first interest rate cut

May remains our call, with 250bp of cuts over the subsequent 12 months

That said, Chair Powell acknowledged monetary policy is well into “restrictive territory” and it will be “appropriate to dial back” on that at some point this year – remember the Fed are currently projecting three 25bp rate cuts. We continue to see some downside risks for growth in the coming quarters as the legacy of tight monetary policy and credit conditions weighs on activity and Covid-era accrued household savings provide less support for spending. Inflation pressures are subsiding with core personal consumer expenditure deflator heading towards 2% and today’s employment cost index offered more evidence that inflation pressures emanating from the jobs market are fading fast.

We remain happy with the view that May will be the start point of rate cuts, assuming today’s regional bank troubles don’t become a systemic issue – Chair Powell appeared relaxed about that. By May we think ongoing subdued core inflation measures will give the Fed the confidence to cut with the policy rate getting down to 4% by the end of this year versus the 4.5% consensus forecast, and 3% by mid-2025. This will merely get us close to neutral territory – the Fed’s view is that 2.5% is likely the long-term average. If the economy does enter a more troubled period and the Fed needs to move into 'stimulative' territory there is scope for much deeper cuts than we are forecasting.

Rates: Market rates should reverse and edge higher again, at least for the coming weeks

We are a bit surprised the market has not moved more on the Fed’s firm preference for a holding pattern on rates. As far as the market discount is concerned, there’s still near a 50% probability attached to a cut in March. This must change. We still think this should be in the 35% area, in terms of probability for a cut for March. And as it moves there, it can pressure the 10yr yield back above 4%, and it should stay above for a bit. The refunding story this morning has a bottom line narrative of heavy supply. There is too much talk there on silver linings. Bottom line it’s heavy. And now we see the Fed is not cutting. At least not yet. As that gets factored in its tough to see market rates ratcheting lower here. The NY Community Bancorp story also looks isolated, so far, and so not systemic. Bottom line we see pressure for yields to edge higher on a multi-week view. Not happening so far, but that’s the view.

This was the FOMC meeting from which some big decisions on quantitative tightening (QT) tapering was mooted to be made. We’ve been of the consistent opinion that the runway the Fed is on in terms of QT is perfectly fine. The Fed can continue to do the $95bn per month for at least the coming 5 months, and after that it could either continue at this pace for another 6 months and then stop, or it could taper if it chooses to. Either way the Fed have time, and that appears to be the way it has approached it at this meeting. It seems the market got too attached to commentary on telegraphing QT intentions from the previous FOMC minutes. This was no more than an early prudent discussion, and not a significant telegraphing event. This Fed is on a holding pattern here too, maintaining the QT at its current pace. We view that as perfectly fine at this juncture.

FX: Just one more reason to hold dollars

Perhaps the only dollar bearish factor in the markets had been the risk that the Fed would turn dovish early and flash a green light to the drop in short-term US interest rates. Other than that, weak growth and disinflation trends in both Europe and Asia, plus simmering geopolitical risks had all favoured the dollar. The Fed’s pushback against ideas of an early cut therefore look just one more reason to hang on to the high yielding dollar. Based on today’s news then we see little reason to change our view that EUR/USD continues to trade near 1.08 for the majority of this quarter, before edging higher through the second quarter when it becomes clear that a Fed rate cut is imminent. Of course US data, particularly price data, will remain a big market driver and markets will now very much focus on the annual CPI benchmark revisions (9 February) and the January CPI data (13 February).

An aside on the US regional banking situation. Focus today on a regional bank saw the EUR/USD three month cross currency basis swap quickly widen 7bp. That is a reminder that the first market move on any news like this is to secure dollar funding (normally dollar positive), with the dollar only selling off when calm is restored (usually by a Fed programme). We will be watching this playbook carefully over coming days and weeks.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article