Mixed conditions in manufacturing soften wage growth in Poland

Some export sectors are growing in Poland while others are stalling. We're seeing mixed signals from industries driven by public investment, and the recovery in manufacturing has also been disrupted by the calendar effects

Mixed signals from the manufacturing sector

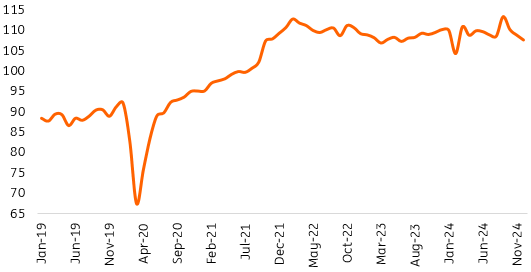

Industrial production in December (+0.2% year-on-year) was weaker than consensus (+1.8% YoY) but in line with our forecast (0.0% YoY). The industrial recovery seen at the beginning of the fourth quarter of last year has stalled. However, the outlook is complicated by the peculiar layout of the December calendar, which may have caused additional downtime.

Stagnation across Europe is a major constraint on Polish exports and production. Between sectors, we're currently seeing mixed signals. Some export sectors (furniture, electrical appliances, and the volatile "other transport equipment" category) recorded declines in production. Others, however, continued to grow (as seen in the fourth quarter of 2024, the manufacture of computers, electronic and optical products, automobiles, and the food sector). There are also mixed signals from industries that could see a recovery in public investment, but this could be due to calendar effects.

Our growth forecast for 2025 (GDP 3.2%) does not look impressive by historical standards, but a regional comparison shows that Poland should again outperform against rest of the CEE region thanks to domestic demand. There are few countries in Europe today that are likely to see strong domestic GDP drivers in 2025.

The recovery of production stalled in December but the calendar effect blurs the picture

Industrial producion, 2021=100

Slower wage growth in December and expected in 2025 should support disinflationary scenario and makes a space for monetary easing despite gradual GDP recovery

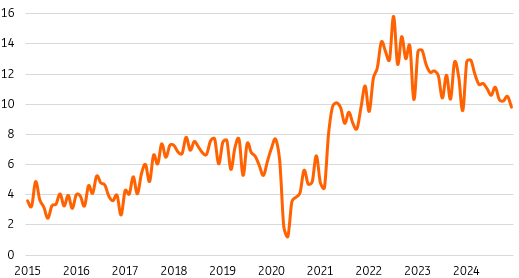

The December labour market report surprised to the downside on both wages and the employment front. Wage growth eased to a single-digit pace and the decline in the number of jobs deepened. The average wage and salary in the enterprise sector increased by 9.8% YoY in December, below our forecast of 11.5% YoY and market expectations at 10.9% YoY. Real wage growth moderated to 4.9% YoY from 5.6% YoY in the previous month. Similarly to previous years, the average wage was boosted by bonus payments in mining, but in December 2024 they turned out less generous than a year earlier.

Calendar effects (a lower number of working days) weighed on manufacturing activity at the end of 2024, which is seen in the employment data. This declined by 0.6% YoY in December (ING and consensus at -0.6%), following a drop of 0.5% YoY in November.

In 2025, average wage growth should slow to single digits from the double-digit average seen in 2024, allowing for gradual disinflation in core inflation. That should make some room for monetary policy easing, especially in the second half of this year.

We forecast that in 2025, this single-digit rate will follow three years of double-digit increases, and we see three main reasons for this.

Firstly, the increase in the minimum wage this year is significantly lower than it has been over the past two years. Secondly, a lower level of inflation means that employees are not putting as much pressure on employers for raises to compensate for the decline in real purchasing power. Thirdly, the deterioration in companies’ financial results and the decline in margins curb the ability of entrepreneurs to raise wages.

Wage growth is one of the drivers of sticky services inflation (up by 6.6% YoY in December) and elevated core inflation in Poland. We forecast that in 2025, wage growth in enterprises should slow to 7.5% (on average), which, combined with the fading base effects on energy prices, should support a decline in CPI inflation to around 3.5% by the end of this year. This outlook suggests some room for monetary policy easing – although the National Bank of Poland indicates that the prospect of interest rate cuts is receding due to upward risks to inflation from administered prices and expansionary fiscal policy.

The wage growth is marginally slowing after CPI shock earlier and general elections in 2023

Nominal wage growth, %YoY

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap