- Quick take

- 4 October 2023

- South Korea

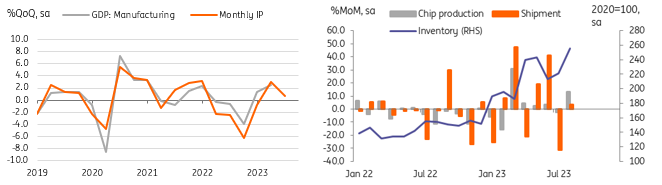

Korea’s industrial production rebounds on strong chip demand

The August IP data showed solid high-end chip demand with both production and related investment rebounding while subdued consumption and investment activity are drags on overall growth. Weak business surveys and high inventory suggest the upbeat surprise in IP may be temporary and the BoK will likely make another hawkish pause at this month's meeting

| 5.5% |

Industrial production%MoM sa |

| Higher than expected | |

High-end chip output boosts manufacturing

Manufacturing IP rose more than expected at 5.5% month-on-month in August (vs -2.0% in July and 0.2% market consensus). The upside surprise mainly came from semiconductor output which jumped 13.4% MoM seasonally-adjusted in August (vs -2.5% in July). We believe that legacy DRAM production continued to decline with the monthly pick-up mainly coming from high-end chip production. As monthly IP data is reported in value terms, the increase in expensive high-end chip production could have been the reason for the overall growth while chip makers are believed to have cut legacy DRAM output. Korean chip makers are expected to increase high-end chip production on growing demand for this special segment. But the high level of inventory is still a concern for the industry cycle. Going forward, we think semiconductor production will continue to rise thanks to strong global demand for AI technology but the legacy DRAM market will likely continue to struggle with low prices and inventory overhang for a considerable time.

GDP is expected to slow but chip production seemingly bottoming out

All industry output rebounded in August but with discouraging details

All industry output rose 2.2% MoM sa in August (vs -0.8% in July) with gains across the economy.

Services continued to rise 0.3% for three months in a row with notable gains in leisure (6.2%) and restaurants (3.6%). This was the first summer holiday season after all Covid measures had been lifted and thus holiday-related activities led the gain. We believe that the longer-than-usual Chuseok holiday will likely continue to support service activities in September and partially in October.

Investment also grew in August with construction and equipment investment up by 4.4% and 3.6%, respectively. For equipment investment, monthly volatile vessel imports (13.1%) were the main reason for the rise thus investment excluding vessels investment continued to decline. Forward-looking machinery orders data contracted, providing a cloudy outlook for investment. Construction rose 4.4% boosted by a one-off plant project completion while residential construction is estimated to decline. With construction orders declining, we think construction will continue to be one of the main drags for the second half of this year and beyond.

Consumption fell -0.3% for the second month presumably because the end of a tax cut programme on car purchases from July negatively affected car sales (-2.4% in August, -12.3% in July). We think the government's shopping voucher programme during the Chuseok holiday is likely to boost consumption temporarily in September.

Overall, the gains recorded across industry in August should add to third-quarter GDP growth but momentum is expected to slow from the peak seen in the second quarter.

Manufacturing PMI rose in August but remains below neutral level

The manufacturing PMI rose to 49.9 in September (vs 48.9 in August) as output and new orders rose, but this has still contracted for 15 consecutive months. Meanwhile, local business surveys from last week deteriorated further as concerns over weak domestic demand and global demand have increased. In addition, inventory levels have remained at an elevated level, which will be a burden for future production. Thus, we believe that the August IP surprise is likely temporary and unlikely to last in the future.

BoK Watch

Consumer price data for September will be released on Thursday, and is expected to accelerate to 3.5% year-on-year (vs 3.4% in August). Together with today's better-than-expected IP outcome, we believe that the Bank of Korea's hawkish pause will continue in October. Beyond October, with dairy products and public transportation fees set to rise from October onwards, inflation will likely remain above the 3% range until the end of this year, and this will be the main concern for the BoK. However, due to clearer signs of slowing domestic growth and increasing financial stress on businesses and households, the central bank will not be able to hike by a further 25bp even if the Federal Reserve delivers a final rate hike later in the year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more